April-May 2020 Edition of Corona Crash or Everything Bubble Pop?

I created this series to serve as a set of living artifacts. This is the 2nd post in the series. I’m striving to capture major current events and financial market action from the lens of a retail investor in the US. It’s essential to understand how one feels and behaves during times of economic uncertainty and market volatility. What better way to do that then keeping a log here to reference in the future? This is not investment advice!!!

2018-2019

2020

February-March

April

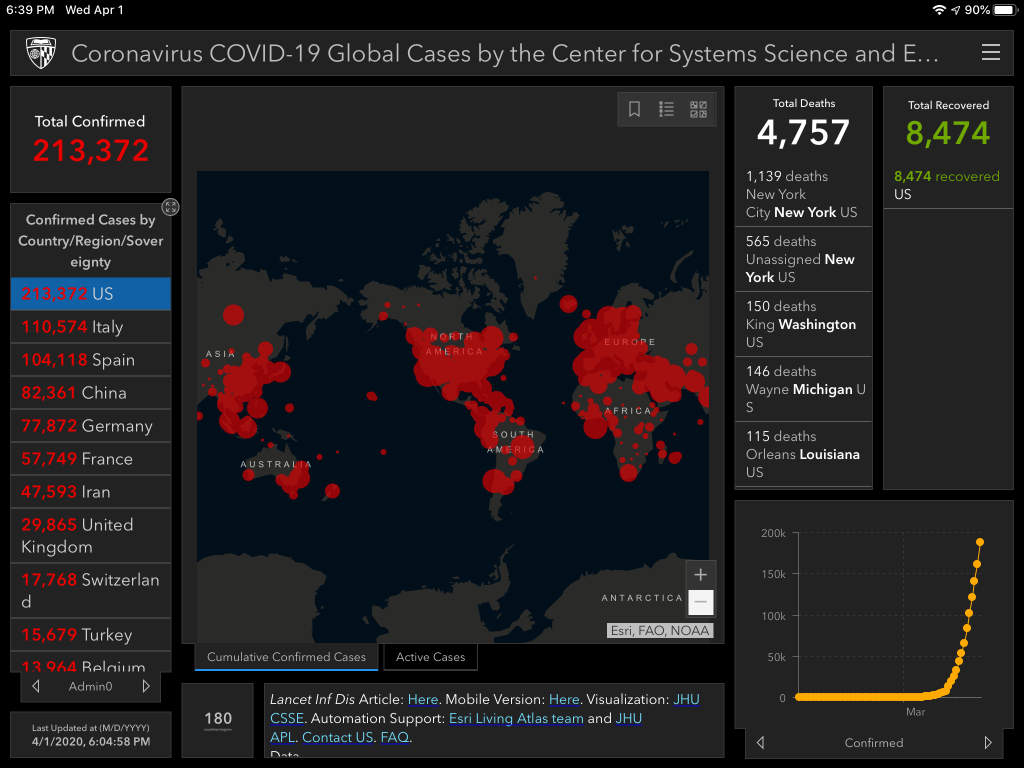

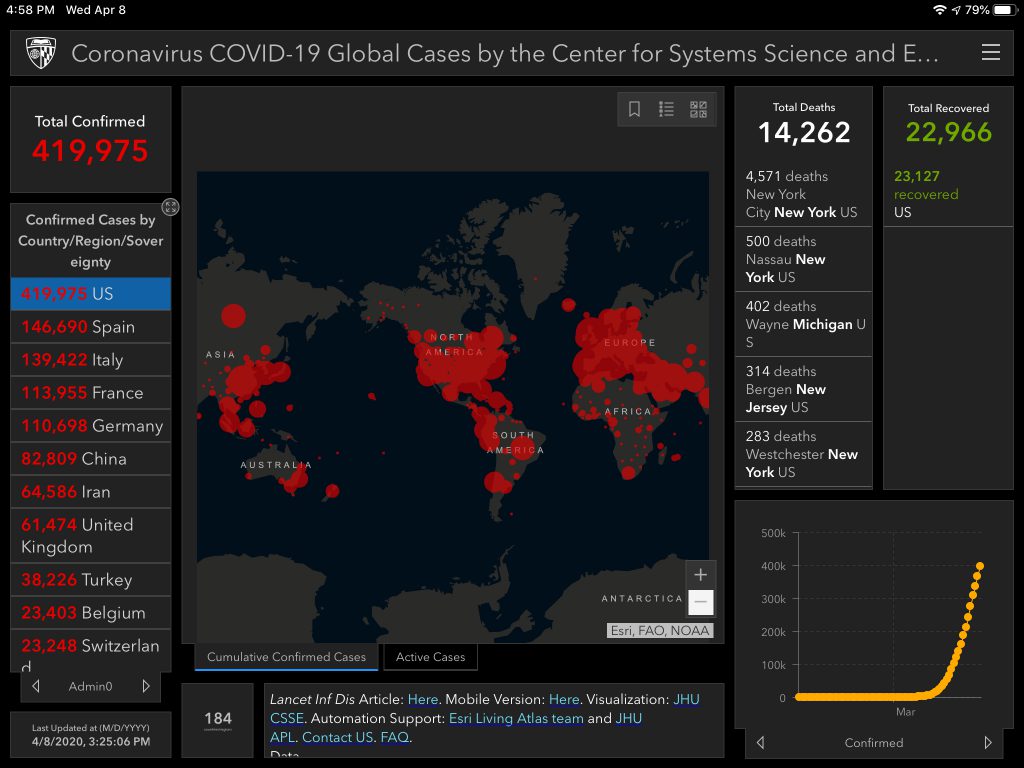

April 1

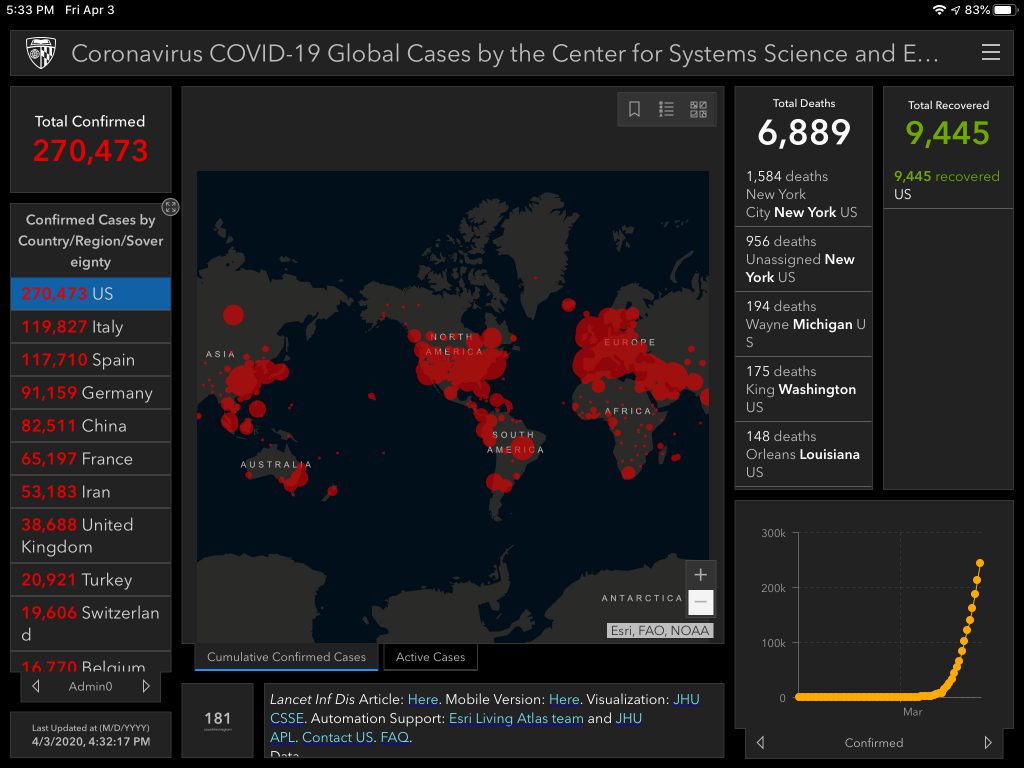

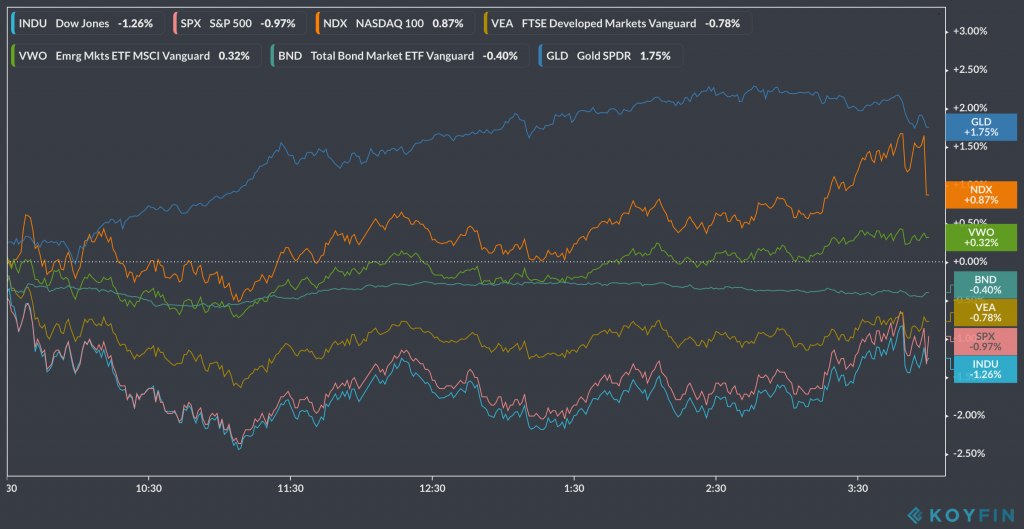

Day 1 of Q2. S&P 500, Dow, and Nasdaq all down ~4.4%. And I have to say… it feels right. Not alarming. Just, right. Green days aren’t comforting to me. They make me question if I’m missing something big. They make me question if I’m greedy waiting for the next leg down, and if it’ll ever come. So being down over 4% today feels right. Things aren’t good and won’t be anytime soon. Thus the stock market reflecting that is rational. Rationality is comforting.

Howard Marks & Oaktree published a memo named Which Way Now? As usual, it’s beautifully written. Read it!

He shares two outlooks: one positive and one negative (arguably the more realistic case). Ultimately, everyone would love to know if we should expect a V-shaped economic recovery or if a long, U-shape is more realistic. He touches on the ability and willingness of the government to write checks to both workers and businesses. But he questions, ‘is it okay, and is it enough?’ While Howard is first to admit nobody can know, his memos are a joy to read because he uses a simple scale: Is outcome A more or less likely than outcome B given what we know? Is it more likely to go down from here or less likely? Is it more likely that one should be positioning their portfolio defensively given the circumstances or more likely that offensive positioning is warranted? I know where I stand, but everyone needs to make this decision for themselves.

NYT published Start-Ups Are Pummeled in the ‘Great Unwinding’ to highlight how high flying companies like ClassPass, Bird, and Airbnb have been thrown into a death spiral overnight. Some will adapt. Some will survive. Many won’t ever be the same. Although valuations may have been stretched for some startups (and public co’s), many were providing valuable services. I love Classpass and credit them for jumpstarting my renewed focus on personal health a few years ago. But they couldn’t plan for this. You can stress test and plan for risky situations, but nobody was preparing for a complete freeze. Workers are losing their jobs and health coverage. While most were probably flying high with dreams about liquidating stock options at sky-high valuations in the future, they’re now worried about finding employment. Things change fast. Not to mention the impact on the supply side of marketplaces like Airbnb due to the overnight disappearance of demand. A lot of people have built income streams that are now gone with the rich valuations.

I sent money to $jackiehlou. She’s raising money through Venmo, PayPal, and CashApp to distribute to people who are having a difficult time making ends meet after losing their job. Send her a few bucks.

Florida Governor DeSantis issued a stay at home order for the entire state.

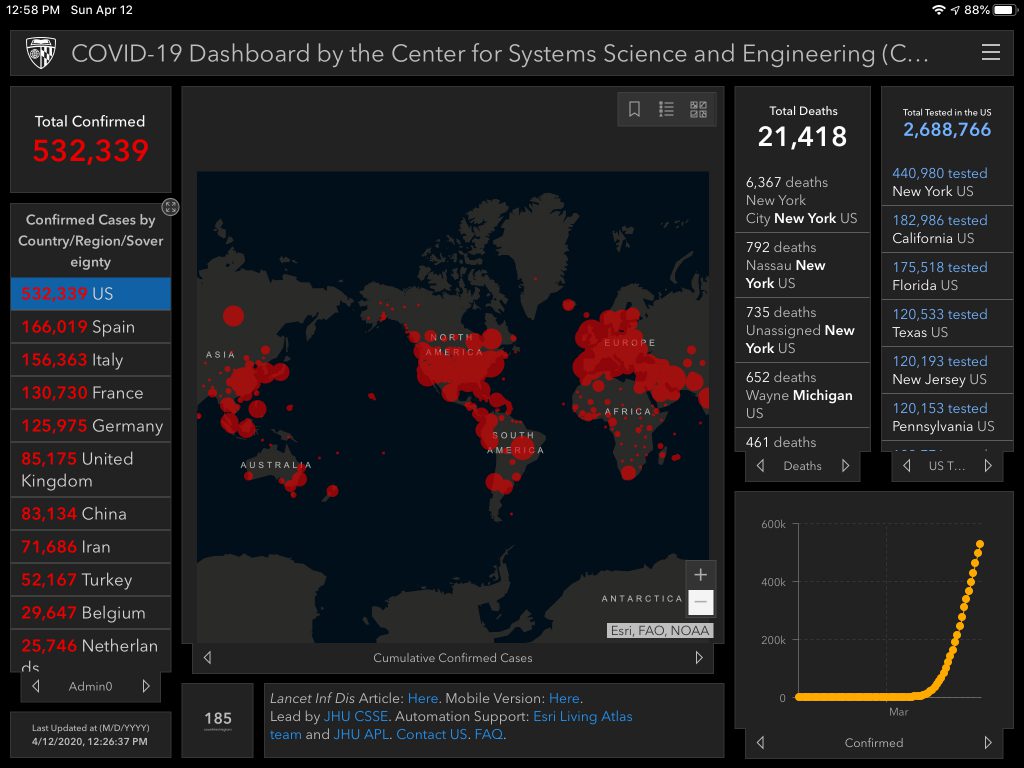

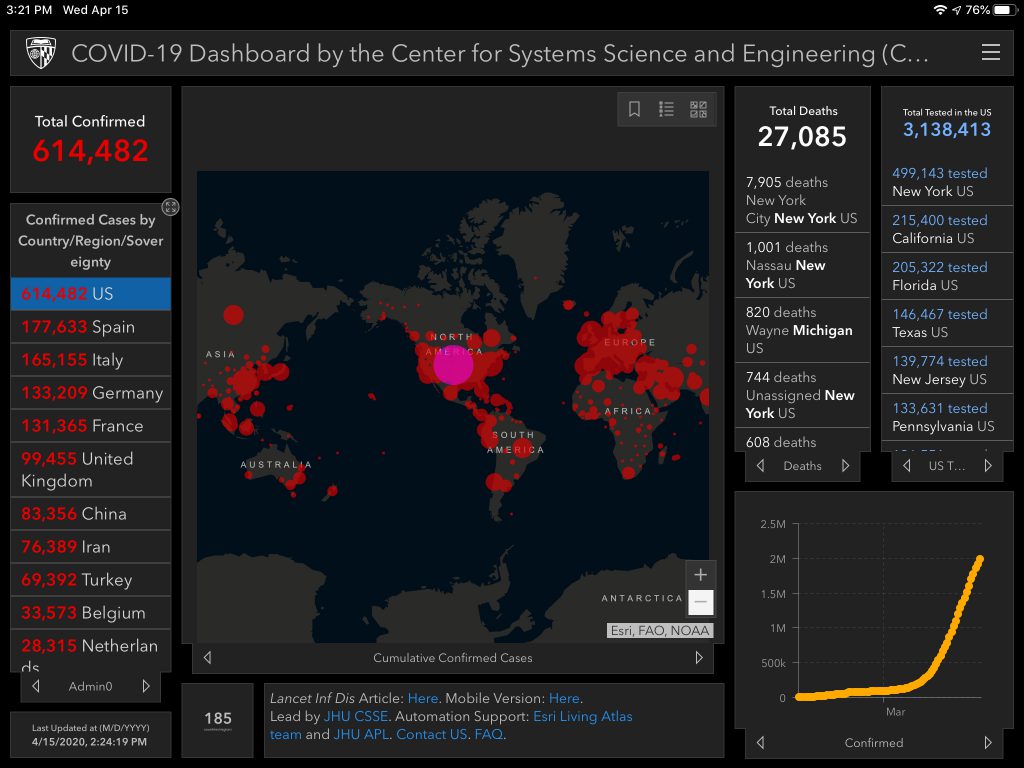

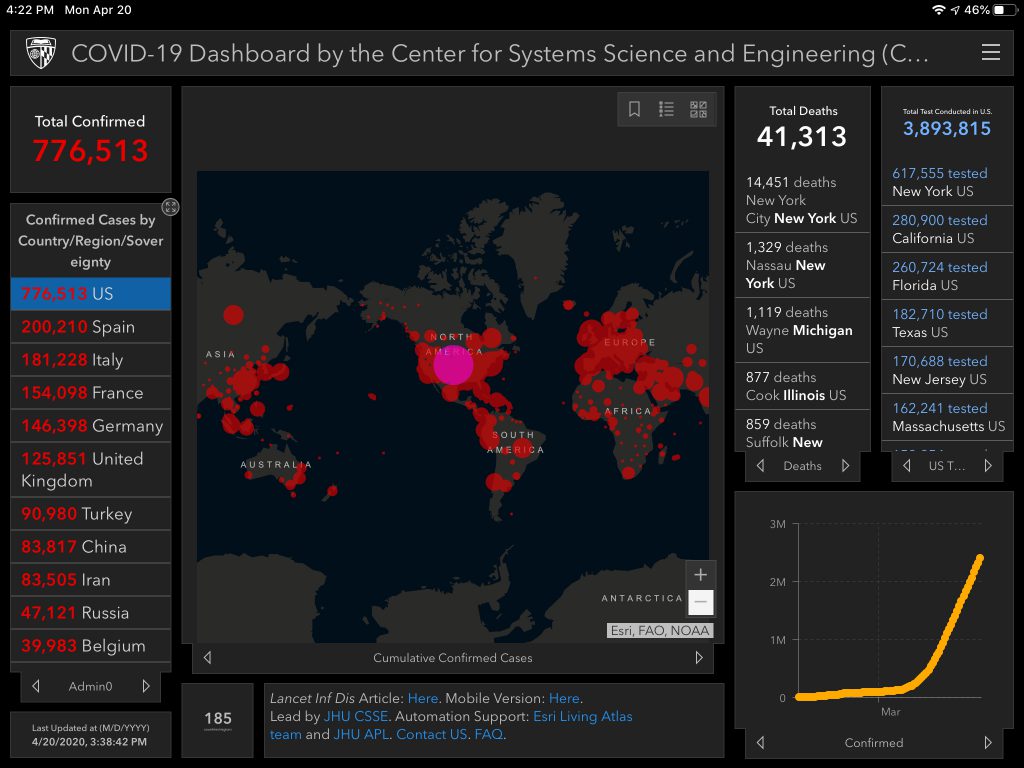

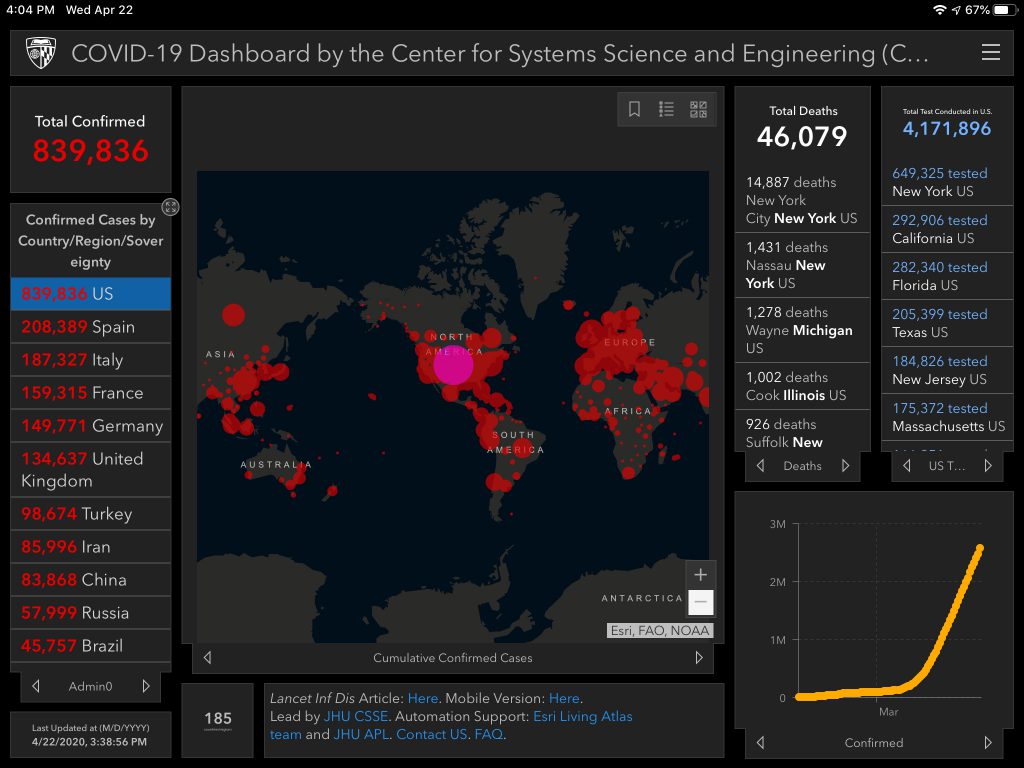

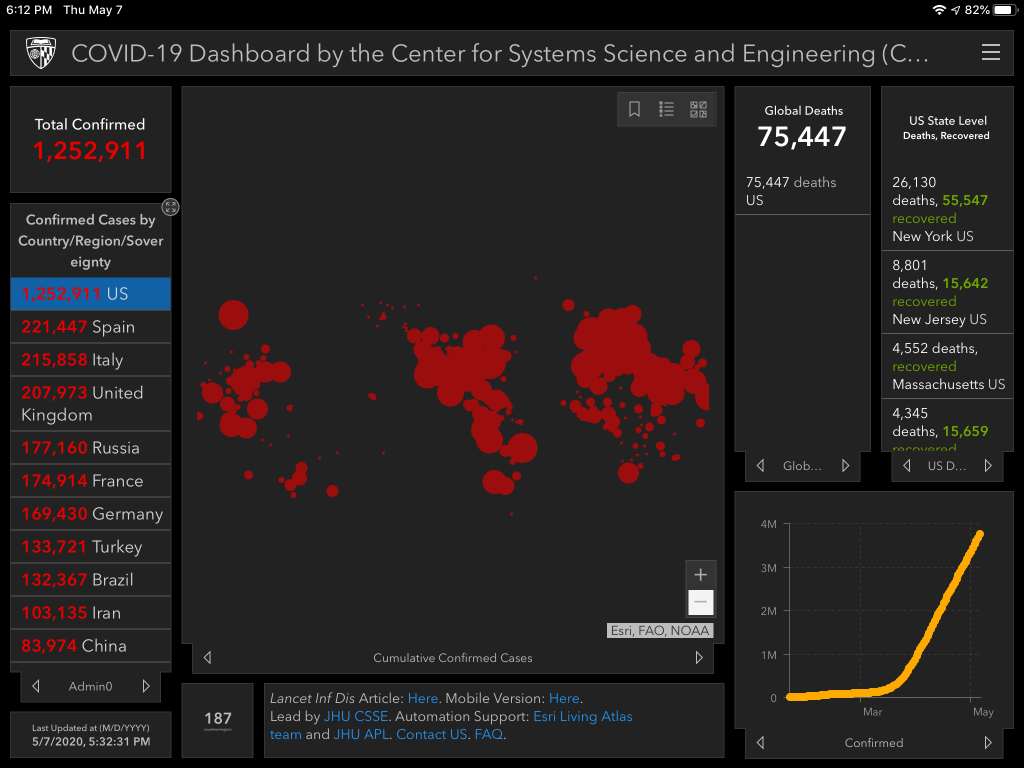

Robert Martin created this time series chart showing COVID-19 growing to the 3rd leading cause of death in the US at the end of March. It’ll inevitably move up very soon.

April 2

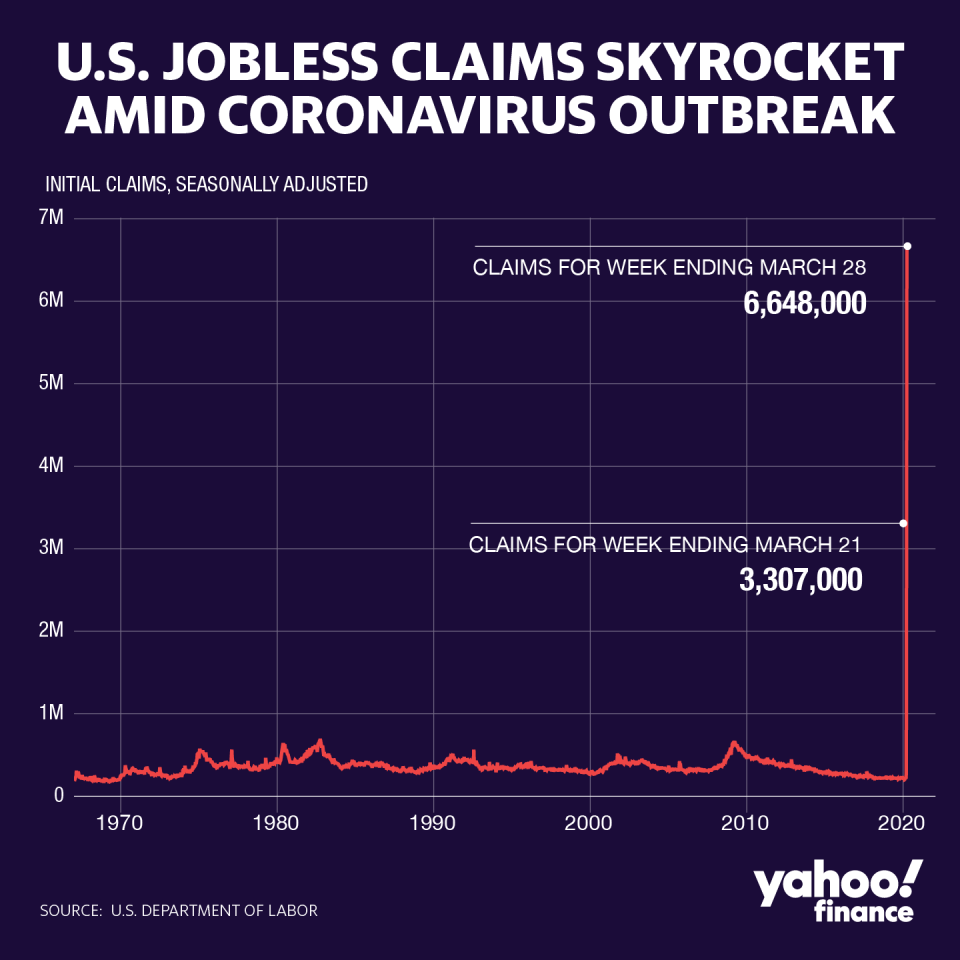

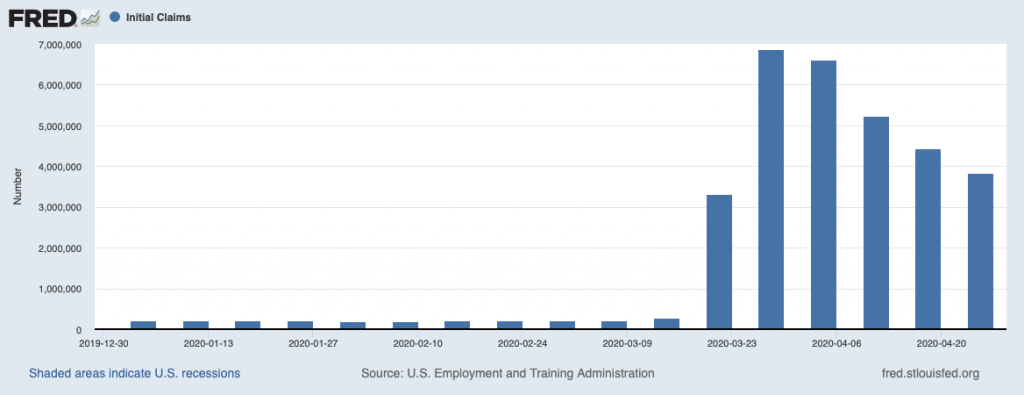

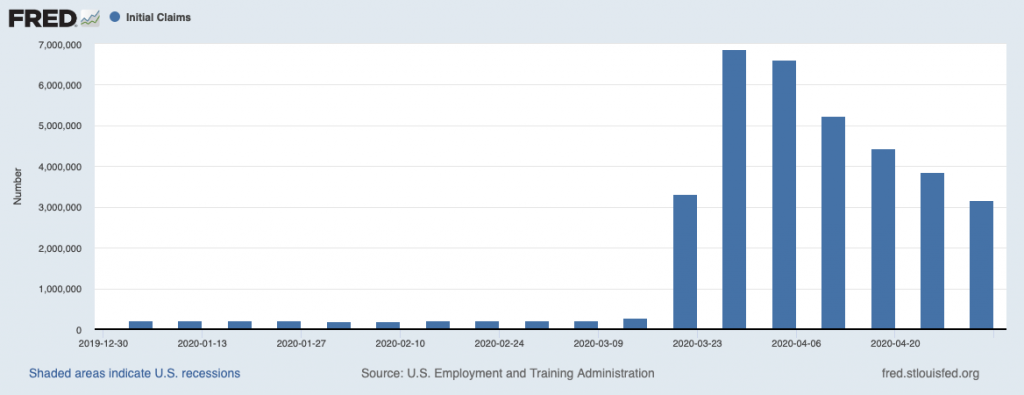

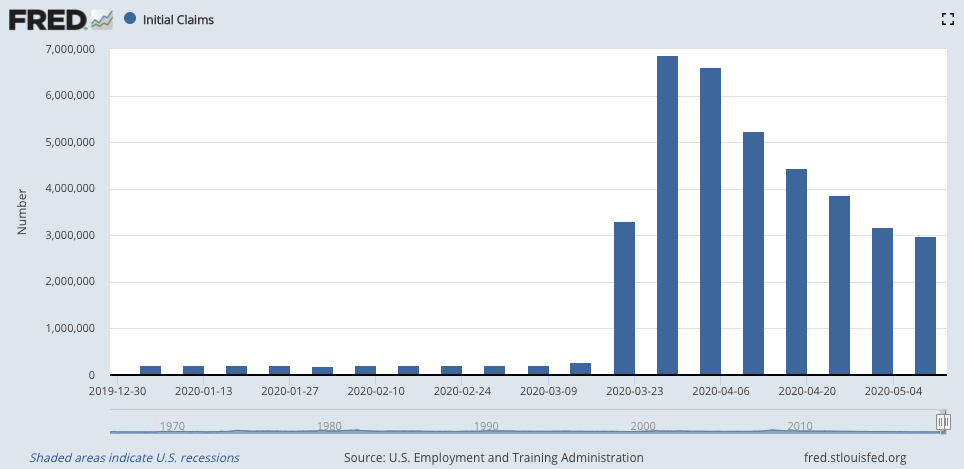

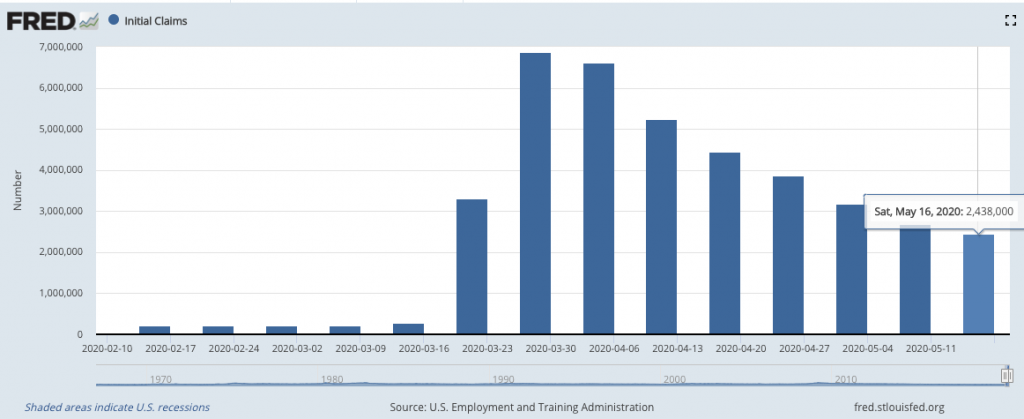

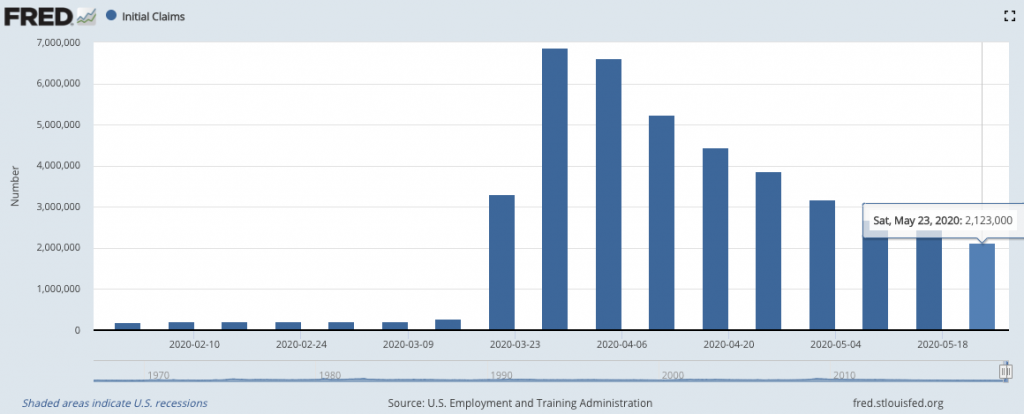

Jobless claims broke another record today at ~6.6 million! This breaks the record from just a week ago of ~3.3 million.

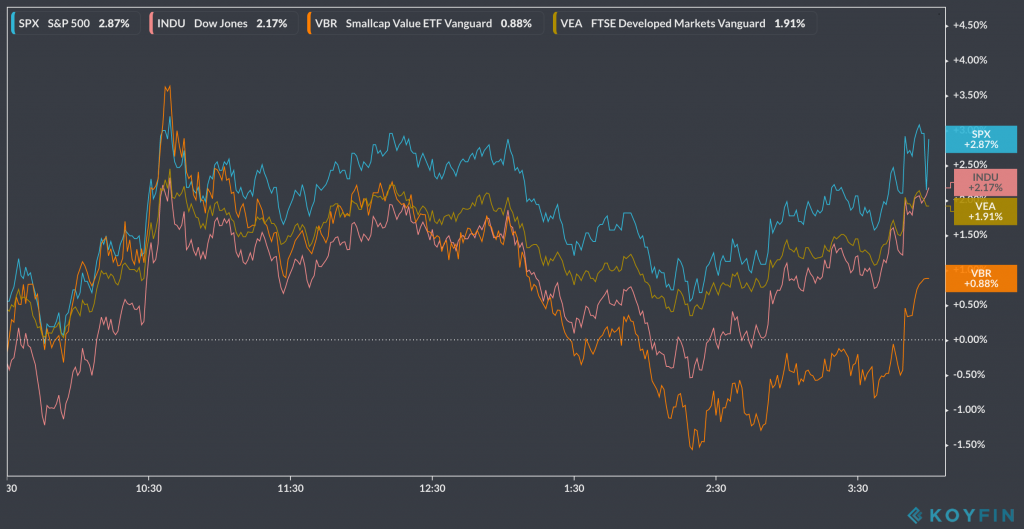

Markets responded similarly today as they did to the record last week. Green. S&P 500 up 2.8%, Dow up 2.1%. Even small-cap value $VBR was up .88%. I don’t get it. Some say it’s because the news is already priced in.

Oil surged over 20%. Supposedly it broke a single-day increase per barrel record. It’s fair to say we should expect some pretty wild swings over the next couple of days. Wilder than the limit up / limit down futures dance that took place a couple of weeks ago with US markets.

Bloomberg published Wall Street Veterans Shun Emerging Markets After Record Rout. “Investors and strategists, from Goldman Sachs Group Inc. to JPMorgan Chase & Co. and Franklin Templeton, are telling clients to hold off on bargain hunting. They’re worried the coronavirus could devastate nations such as India, South Africa, and Brazil, where infections are only now starting to gather pace.” I believe in international diversification, including EM. Perhaps I listen to too much Meb Faber. I can stomach the volatility.

Brent Beshore published Viral Prohibition, Eminent Domain, and the Path Ahead. Well worth the time to read. In it, he proposes that components of Prohibition (“a government-mandated shutdown that forced businesses to hunker down and adapt”) and eminent domain (“a legal doctrine recognizing the right of a government or its agents to expropriate private property for public use while compensating the owners”) are analogous to what we’re facing. Here’s his best guess for what might happen next: “As of March 29th, I believe we’re headed for three phases: Lockdown, Winter, and a New Normal. The more “flattening the curve” that takes place, the less strain on the hospital system, but also the longer a government-mandated and/or self-imposed lockdown will be necessary. Preparing now will be essential for giving your organization the best chance for survival.” You should read his article for more details on those 3 phases. As for the big financial question on everyone’s mind (is this a deep V or U), Brent writes, “…we should expect and plan for a tremendous amount of pain personally and professionally. I believe 20%+ unemployment is inevitable and could rise as high as 30%. GDP seems set to drop 30-50% and I can’t see a recovery being “V-shaped,” at least with the right side of the “V” rising to nearly the same level, without lengthening the time scale.” By the way, if you’re a family-owned business earning $2.5-$15M/yr, visit permanentequity.com. They specialize in partnering, investing, and sometimes outright buying ‘unsexy’ businesses.

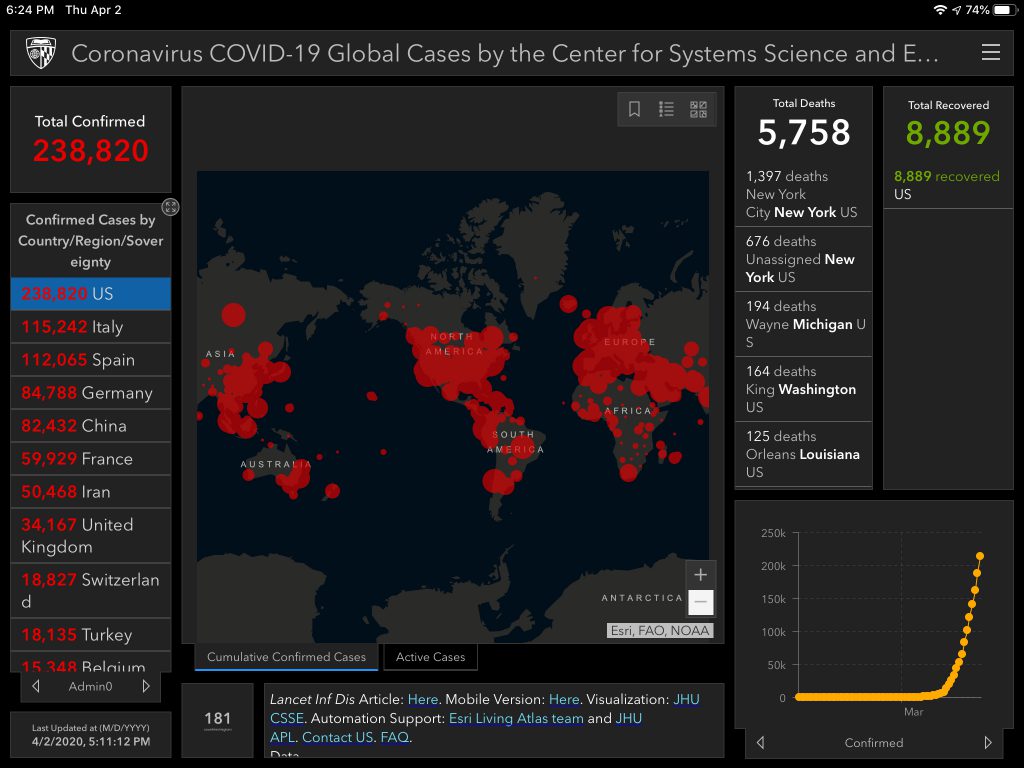

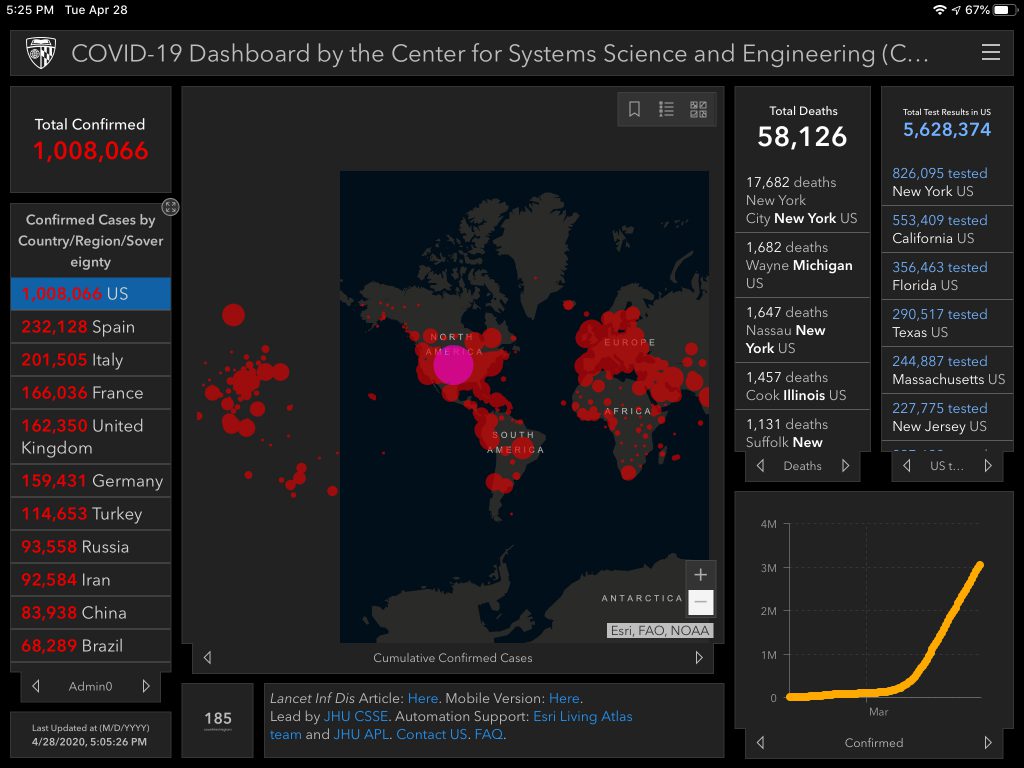

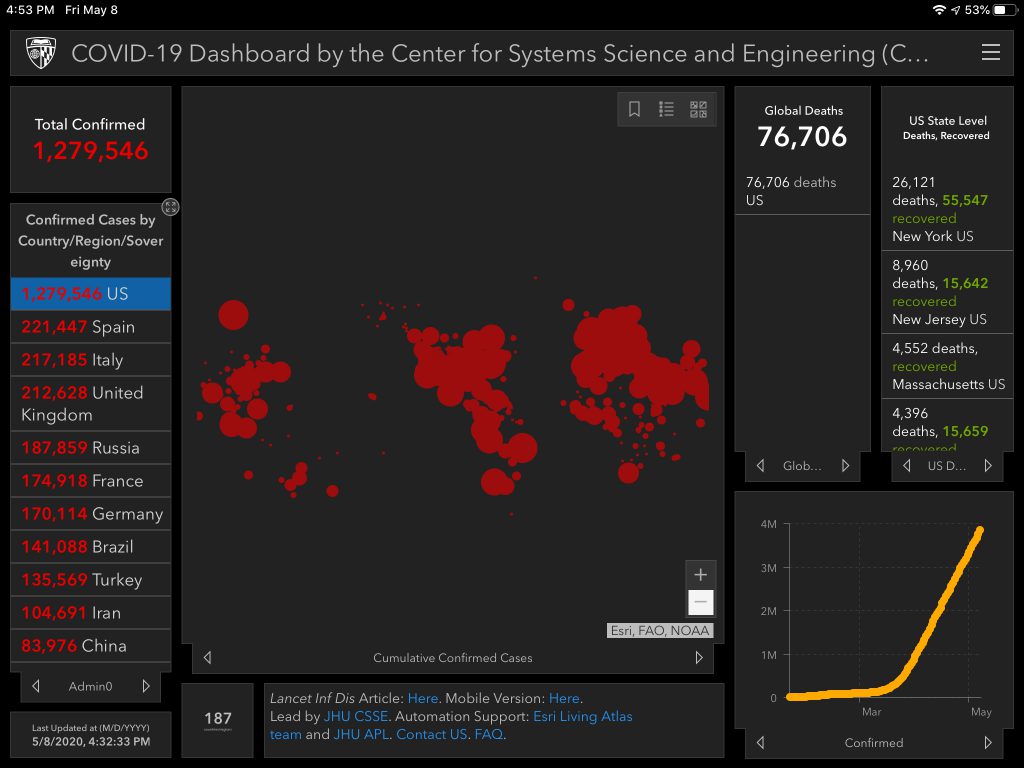

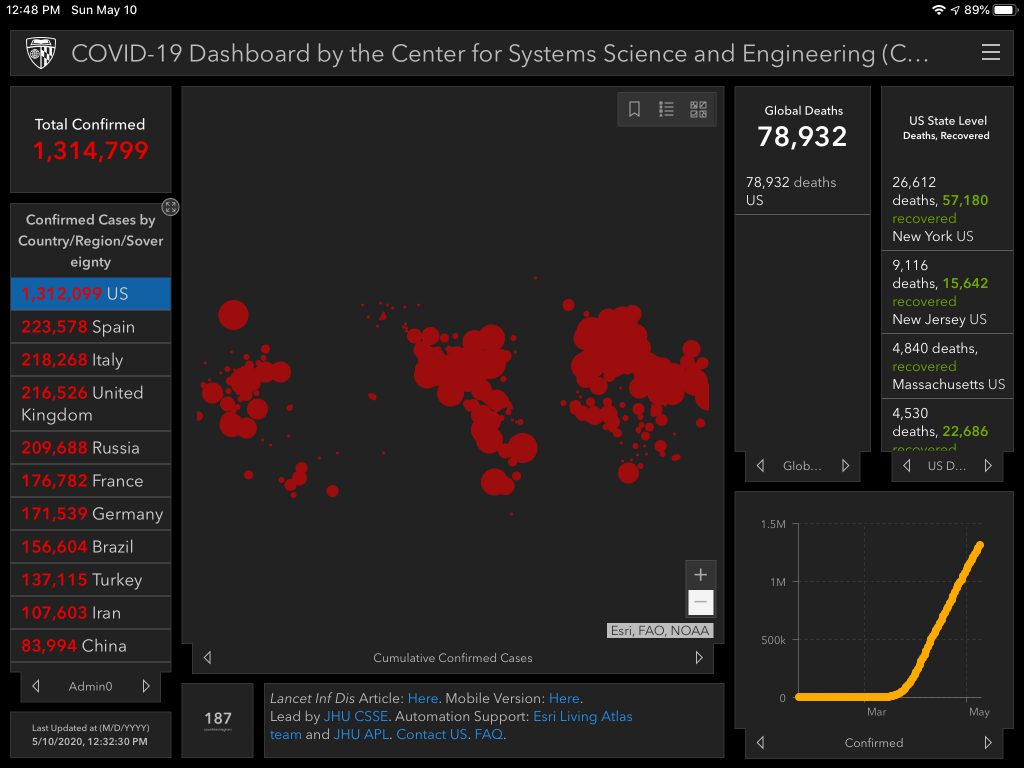

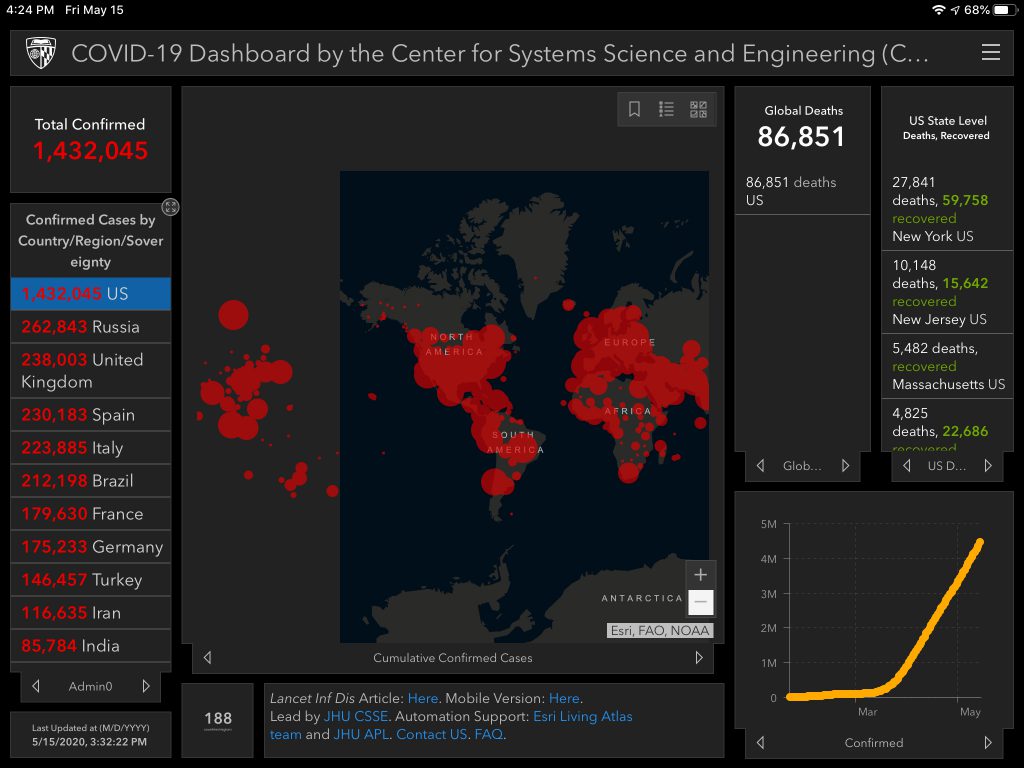

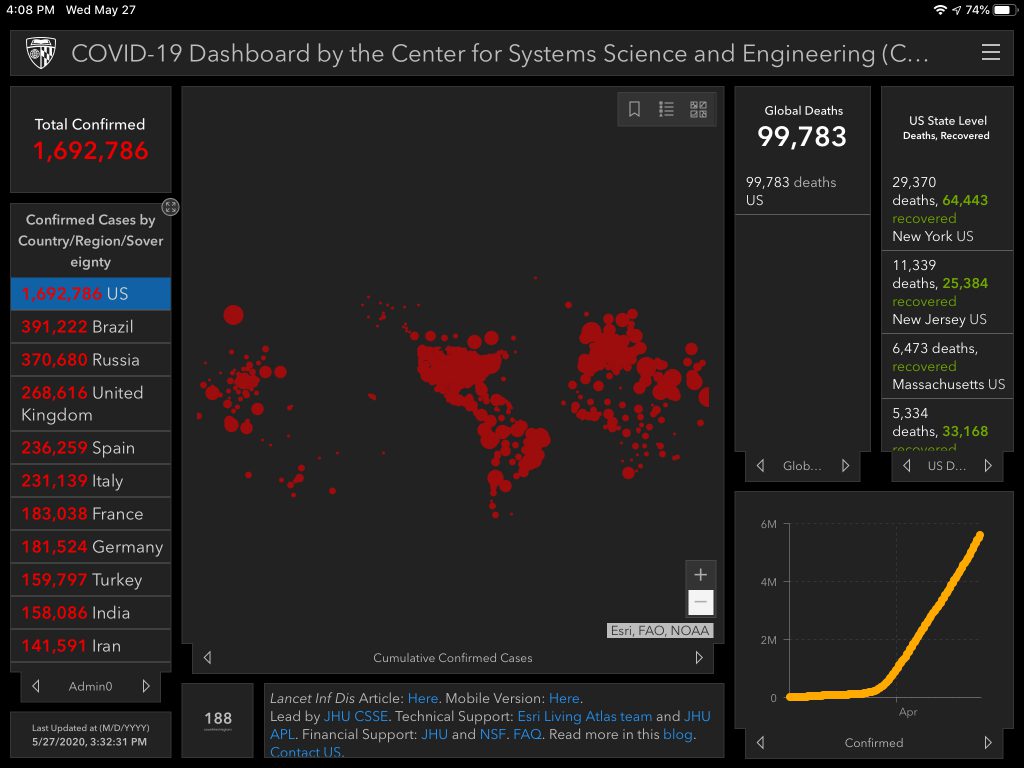

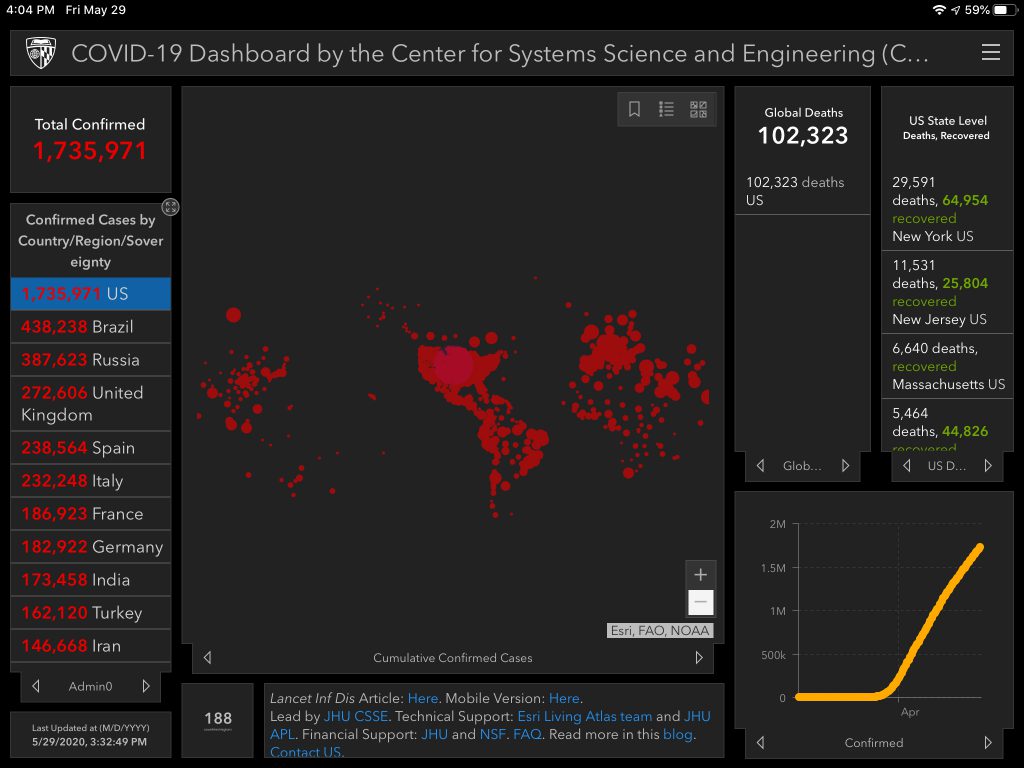

Coronavirus cases have now exceeded 1 million worldwide.

April 3

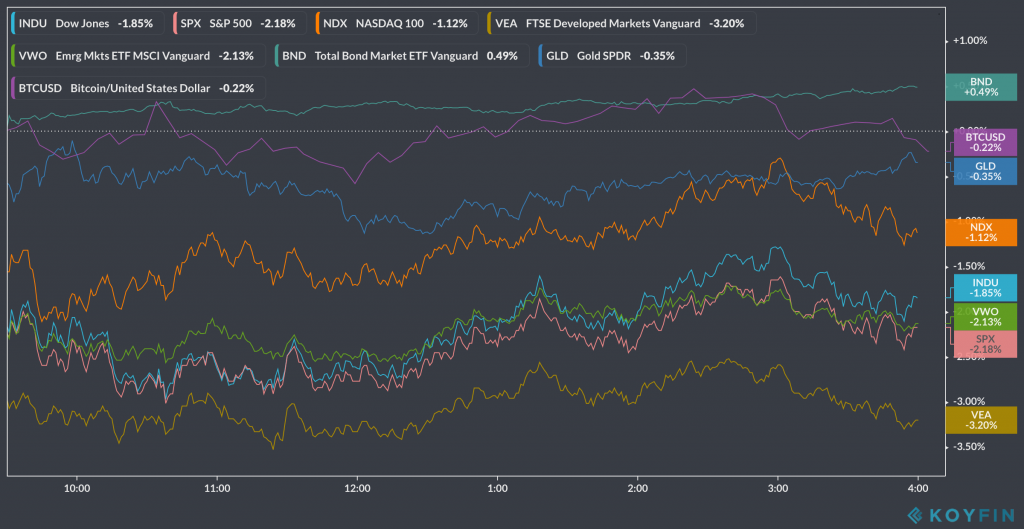

S&P 500, Dow & Nasdaq are all down ~1.5% today. S&P 500 is now down ~23% YTD. Oil surged another 10%+ today. Gold was up .5%.

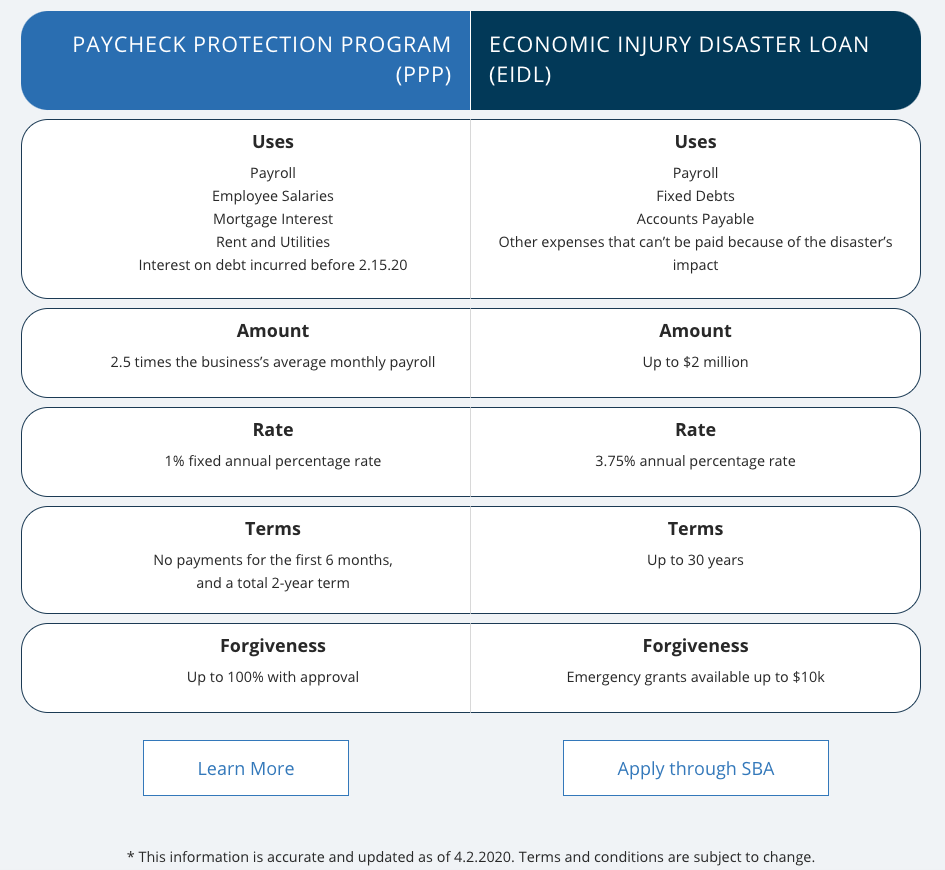

Today’s the first that business owners can apply for loans from the ~$350B allocated to SMBs. Unfortunately, from what I’ve heard, it hasn’t been smooth. There’s a lot of confusion amongst both interested applicants and participating lenders. Heavy.com created Where to Apply for Payroll Protection Program: SBA COVID-19 Links for business owners interested in the Paycheck Protection Program (PPP). The PPP allows companies to obtain up to $10 million in loans that are 100 percent forgivable if they don’t lay any employees off, or if they rehire any that already have been. Another option is this divvy.com page, who teamed up with Silicon Valley Bank. Owners interested in the Economic Injury Disaster Loan Program and Advance (EIDL) can head directly to sba.gov to apply. Check out liveoakbank.com to learn about the differences between the programs.

April 5

Sunday. Feels like the calm before the storm for US equities. Q1 wrapped up and earnings season kicks off soon.

It’s starting to sound like banks can start accepting and processing the PPP loans now, which is good news. Jill Castilla of Citizens Edmond Bank took to Twitter to share the news as did Saira Rahman of Alpine Bank.

Denise Hearn shared a list of organizations worth donating to: COVID-19 — where to give money now. Check it out. Donate to 1 or a few if you can.

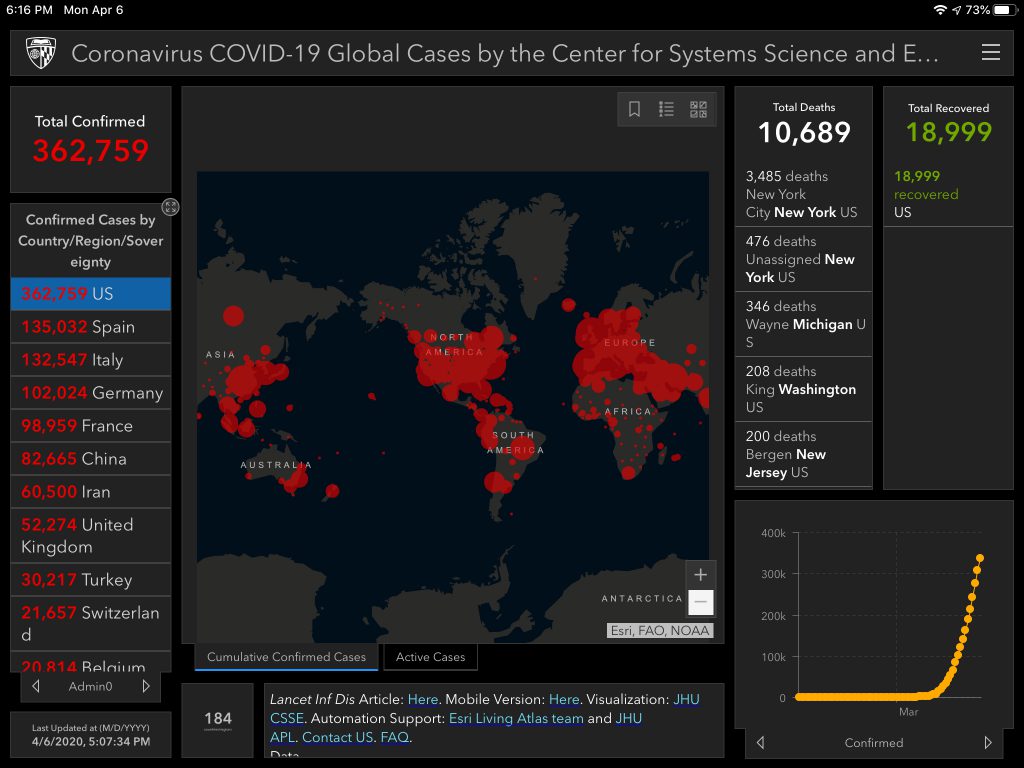

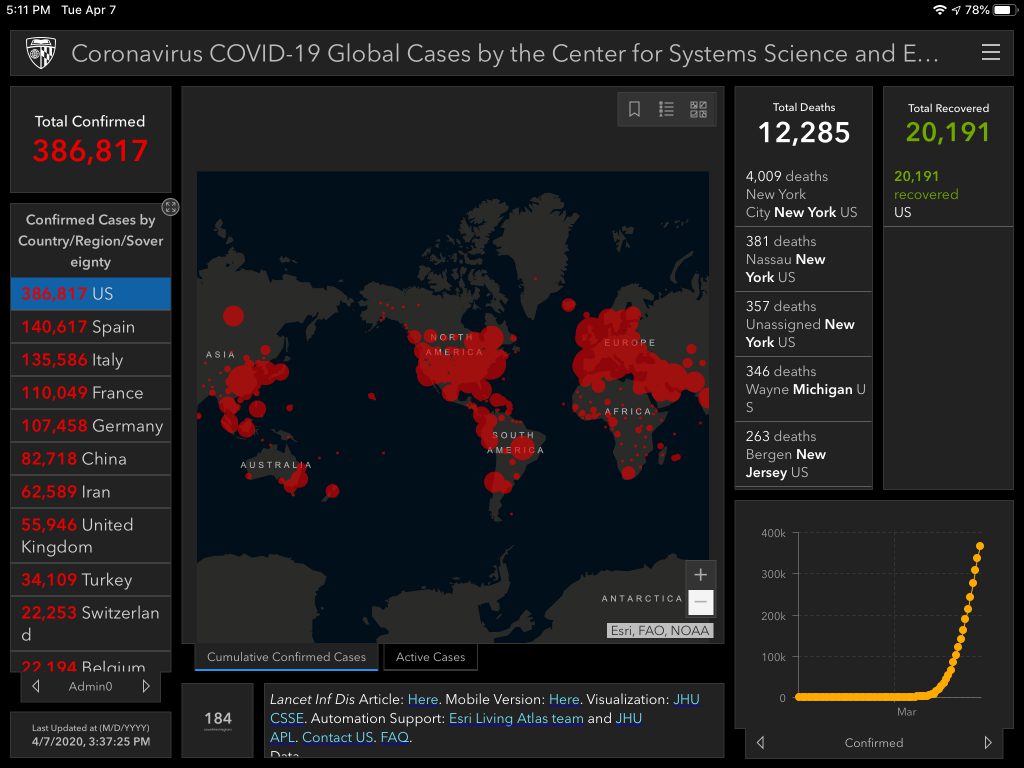

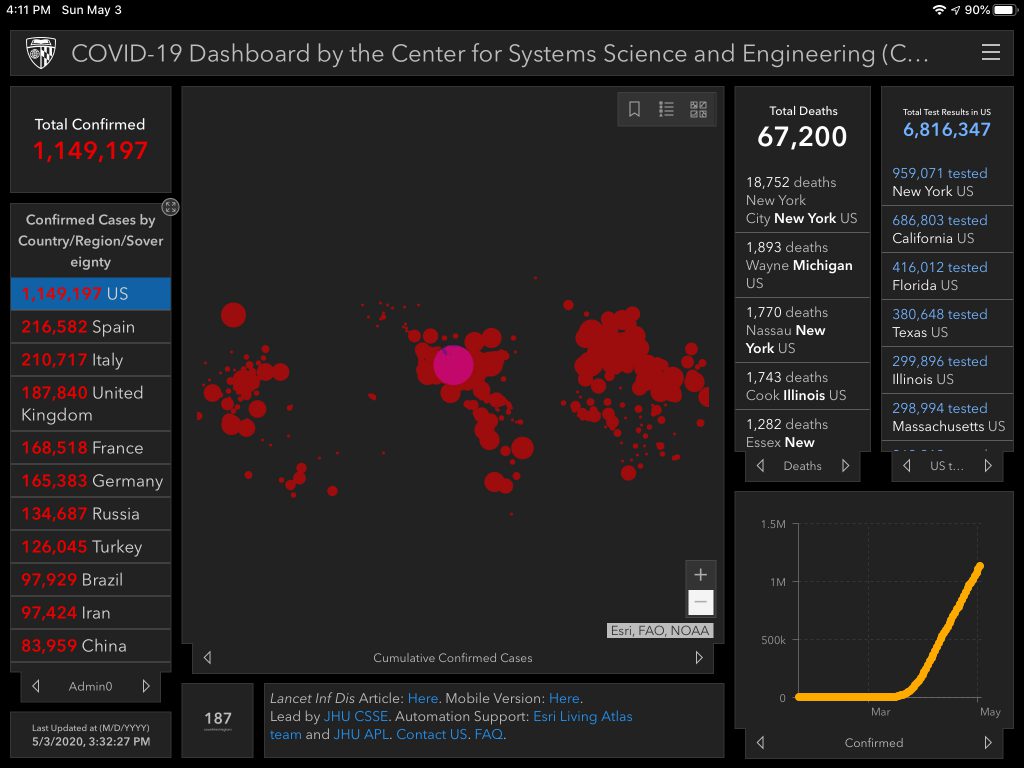

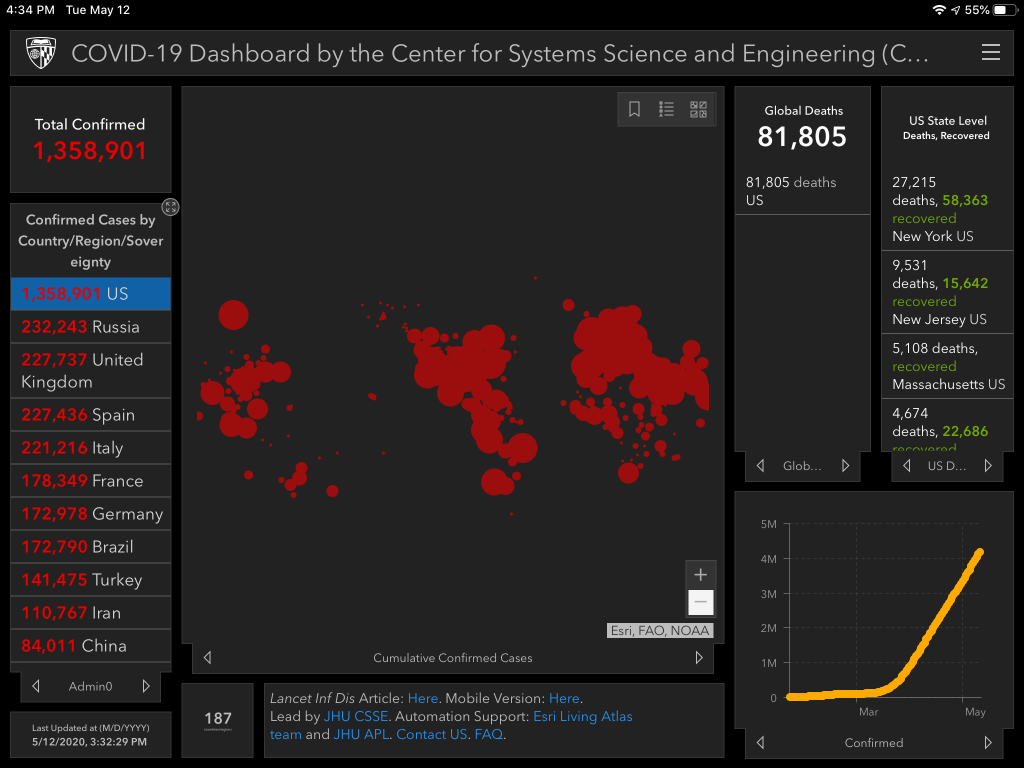

69,000 COVID-19 deaths globally. ~9,500 in the US.

April 6

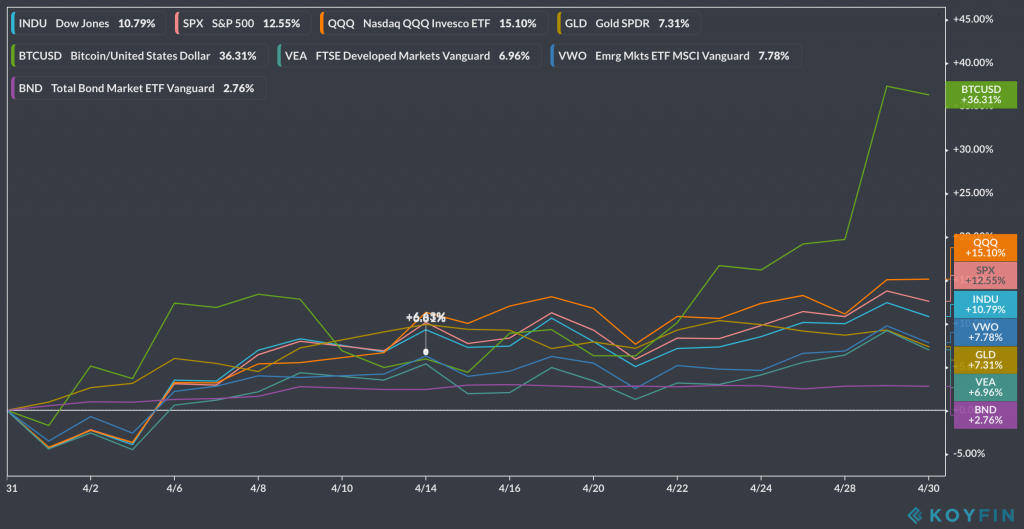

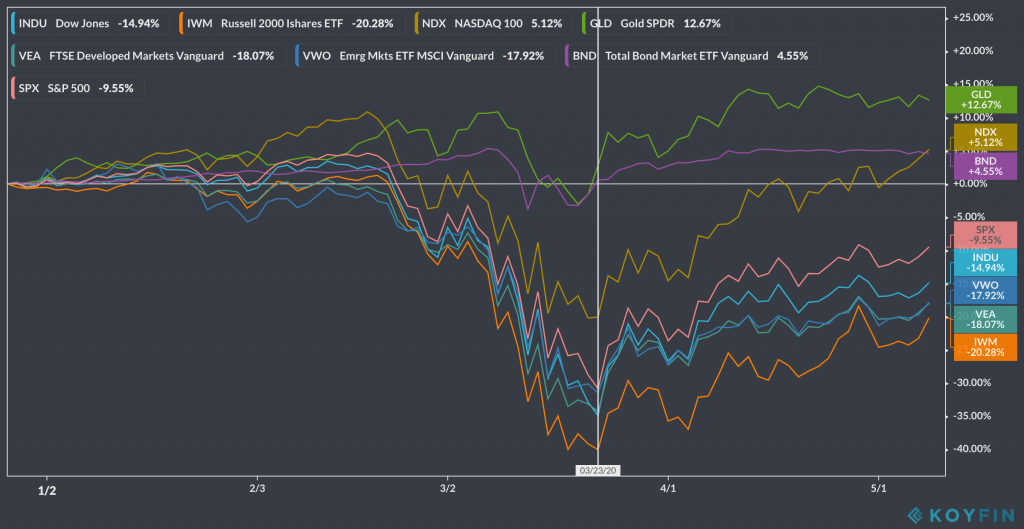

Monday. S&P 500 and Dow both up over 7% today. Mind-boggling. I don’t get it. According to Sean Brown, today is the 9th day in the last 35 where the S&P 500 closed up or down 5%+. Both indexes are up over 3% MTD. Interestingly, $btc is up ~12% over that time frame.

Jamie Dimon & JPMorgan published their annual shareholder’s letter, focusing on how they’re handling the crisis internally. He shared that they’re halting buybacks, they won’t be requesting any regulatory relief from the government, and how they’re taking care of employees (e.g. paying branch employees for their regularly scheduled hours even if they’ve been reduced).

A memo packed with much more theory & market action came from Palm Valley Capital Management as they recap Q1 2020. They were ~92% cash to start the quarter and ended with 52%. As small-cap value investors, they’d been sitting on cash since establishing the fund waiting for buying opportunities. As for why more wasn’t deployed, they said, “One reason we didn’t reduce cash levels in the Fund even further during the market’s downswing was because most higher-quality companies didn’t become cheap, in our opinion. You can’t start from nosebleed valuations, have an average bear market decline, and assume everything must be on sale.”

Regarding the title of this page, Palm Valleys’ stance is, “While the coronavirus was the catalyst to send markets spiraling, we believe the Fed is the culprit for why the financial damage turned so bad, so quickly. Goaded by investors, politicians, and others, central banks suppressed interest rates and printed money for years, leading to a buildup of debt and risk-taking that could not be managed through an economic pothole. For corporations and investors, financial prudence was unnecessary with a Fed backstop (see ‘Risk Management—Why Bother?’). And when the chickens came home to roost, the average Joe took it on the chin. Unemployment claims skyrocketed to 3.3 million for the week ending March 21st, trouncing a previous weekly peak by a factor of more than 4x. Hordes of businesses will be pushed to the brink as revenues disappear, but costs remain. In an attempt to offset the damage that was exacerbated by their prior actions, the Fed has gone all-in on monetary policy.”

Small business owners still looking to apply for a PPP loan can try this Radius Bank application.

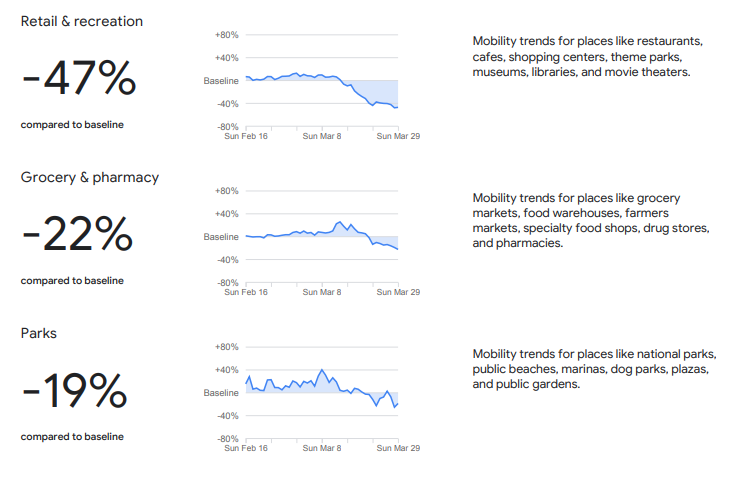

Google released COVID-19 Community Mobility Reports. These interesting reports are supposedly informed by anonymized product usage data (Google Maps, device location history, etc.). Here’s the United States report for March 29, 2020.

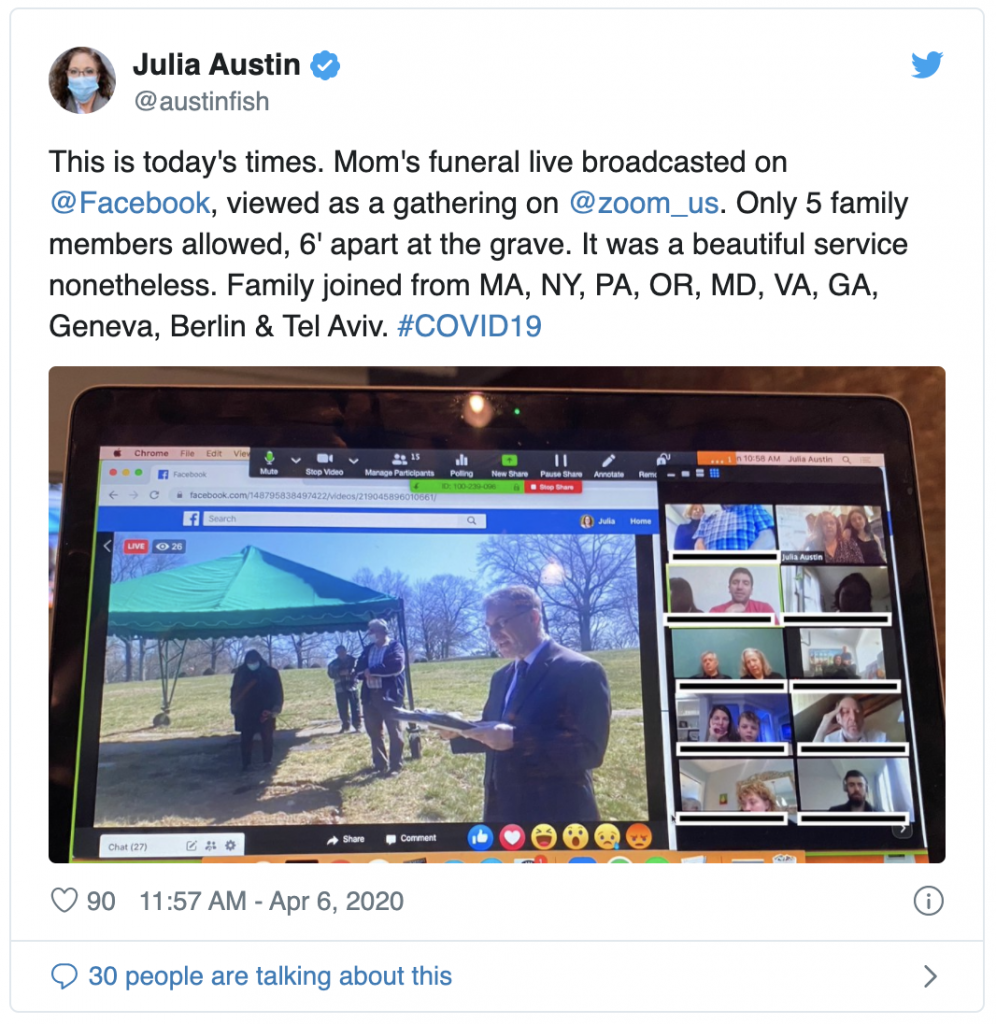

I can’t think of anything that encapsulates how bizarre life is right now then how we’re forced to deal with death:

April 7

Equities pretty much picked up where they left off (S&P 500 & Dow both ended up over 7% yesterday). They were up as high as 5% intraday but took a turn down before the closing bell. $SPX finished down ~.06% and the Dow finished down ~.15%. These rallies are mind-boggling.

I heard about Eric Peters’ wknd notes on this recent Ted Seides podcast episode. I just read wknd notes: The Bullet Factory (published Apr 1). I love his ‘Honestly’ sections. Excerpt: “When Dr. Fauci says this is not the flu, I don’t know what he means. And I don’t know how long the global economy can be stopped without causing catastrophic harm. I don’t know what damage to business and consumer psychology has already occurred. I don’t know what happens if we restart the economy and suffer a renewed outbreak. I don’t know if a V-shaped recovery fueled by a historic monetary/fiscal stimulus is 2-3 months away. Or whether V is the right letter. I don’t know if deflation lies ahead, or inflation, or both. I don’t know how $2trln gets into the right hands without becoming a historical fiasco. I don’t know if this is the once in a generation buying opportunity my broker describes. I don’t know how laws and taxes will change. I don’t know if the Dems will win. I don’t know how the pension system will remain solvent in a world of zero rates. I don’t know how emerging markets can handle this. And I don’t know if we can get through this without an unexpected conflict arising. But I do know no one else knows. And I also know these are some of the right questions to be asking.”

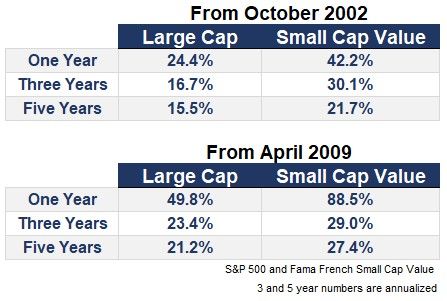

Ben Carlson published What Happened to Small Cap Value? He highlights the pain in small cap value this year but the fact that they often see far higher returns than large cap during recoveries. Obviously no crisis is the same. There’s no guarantee they’ll outperform next time around. Every investor needs to make their own allocation and diversification decisions.

Jack Dorsey announced that he’s “moving $1B of my Square equity (~28% of my wealth) to #startsmall LLC to fund global COVID-19 relief.” If interested, you can track his donation action.

I watched some footage of COVID-19-only hospitals this week, which was upsetting. But it’s reality. The majority of us are lucky to sit in our own homes, healthy, safely, day after day after day. I think some aren’t realizing how real and bad this crisis is for others. Also, everyone working in the healthcare system is incredible (and many are significantly underpaid for the risk they take and the value they provide).

April 8

Yahoo Finance headline:

‘Dow, Nasdaq, and S&P close at 4-week highs, with S&P more than 20% above March low’

In my head:

Enjoy your virtual seders this evening.

I’m loving ‘wknd notes’ from Eric Peters. This weeks is titled Tales of Survival.

Calibrating— yet another memo from Howard Marks after he published a record high of 4 in March. If you’re familiar with his writing, then you know he often thinks in terms of positioning portfolios offensively or defensively. As he says in this memo, ” if you get offense/ defense right, those other things will take care of themselves.” Those other things are referring to capital allocation (large-cap, small, international, etc.). In recent years, he and Oaktree “…felt the uncertain, low-return environment called for defense to be over-weighted relative to offense.” But he expresses a big change in this April 6 memo. “Given these new conditions, I no longer feel defense should be favored… I’m not saying the outlook is positive. I’m saying conditions have changed such that caution is no longer as imperative. With part of the crisis-related losses having already taken place, I’m somewhat less worried about losing money and somewhat more interested in making sure our clients participate in gains. My 2018 book, Mastering the Market Cycle, carries the subtitle Getting the Odds on Your Side. In that vein, I now feel the odds are more in investors’ favor or, at a minimum, somewhat less against them. Portfolios should be calibrated accordingly.” You should read the actual memo to see what he says regarding catching the market bottom.

April 9

Thursday. Last open day of the week for US Stock Markets since Good Friday is tomorrow. New jobless claims were released this morning. Another ~6.6 million Americans filed for unemployment benefits. A record of 16.5 million unemployment claims were filed in the past 3 weeks. To serve as a shock absorber, the Federal Reserve announced another stimulus package of ~$2.3 trillion.

So the markets did what they seem to do upon hearing bad news these days. Rally. Many of us are dumbfounded. Day after day, I write that I can’t make sense of green days. $SPY is down just ~13% YTD and only ~4% in the last year. The Nasdaq is positive this past year. How can this happen with the economy in a significantly weaker state?

Everyone needs to form their own thesis. My current thinking is that the more we rally, the more ridiculous this market is. I can’t give in to the FOMO. When I try to find the uniqueness of this crisis from past crises, I primarily see the unprecedented actions by the Fed. Maybe I’ll look back and say, ‘shit, they showed a willingness to do ANYTHING to keep the markets propped up.’ But I’m having a hard time believing that’ll happen. Maybe it’s just my own internal biases. Valuations are still super high. Many stocks are rallying 7%+ on awful macro news. And that just doesn’t make sense because I value rationality and common sense. While the markets may rally in the short term with help from the Fed, I don’t see it lasting forever. These loans will get disbursed over the next couple of quarters. Maybe it helps some businesses survive. Maybe some even thrive. But many will die. And what happens when some need to pay them back, but can’t? Won’t there be an increase in bankruptcies over the next 18 months? My current thesis is that the markets are actually going to trail real-world sentiment (even though they often lead).

When the health crisis is tamed, and life drifts back towards normalcy, that’s when we may see the markets falter. When the Fed stops and retreats, then the stilts will break. At this rate, it’s hard to believe they’ll ever abandon, but nothing lasts forever. At this point, I’m remaining defensive to opportunistic—anything but bullish. I’m more afraid of a bigger fall in Q4 or 2021 than I am of anything else when it comes to the financial markets. The only thing that would give me comfort would be a tumble back down to 30%+ from the all-time highs. The sooner, the better. I’d love to see this in the coming days, weeks, or a couple of months. And at that point, I’ll buy.

April 10

Global death count passed 100,000 😞

April 12

Easter Sunday.

The Netflix Top 10 in the US right now is led by a series called Tiger King. I wonder if this tidbit will make it in the history books.

April 13

Monday. $GLD hit a 52wk high.

Trump made todays Coronavirus Task Force briefing all about him. He presented a cheesy propaganda video. It wasn’t the right time and place if you ask me. Somewhat comical. But pathetic. Inappropriate.

And he threw a fit.

April 14

Another day of major equity markets rallying. Well, oil tanked. Sentiment is the same for me as on Apr 9. No need to reiterate.

Howard Marks published another memo, Knowledge of the Future. As usual, he highlights that we can’t possibly know how exactly this will play out. He identified the following as truths:

He then lays out reasonable questions that will need to be answered and steps that will need to be followed to get the virus “under control.” This leads to one of the biggest open questions. “One of the thorniest questions remains how society and its leaders will make the trade-off between minimizing deaths from the virus and restarting the economy. A decision to end the stay-at-home orders on May 1 rather than May 31 will be better for the economy in the short run. However, it’ll also send people into society while there are still infected people around, and thus it’s likely to result in a ‘rebound’… How will we make that trade-off?” Howard eventually gets to the likely answer. The reopening will be a gradual process. Like Fauci has said, it won’t be a widespread light switch. Even if it were, Howard points out that individuals will have to make their own decision as to how to live their life. They’ll establish new norms. It’s unlikely many will get right back to their old ways just because someone gives the green light. And this process will have economic impacts. It likely means we won’t see the swift V-shaped recovery the media likes to tout. The rest of the memo covers recent Fed action and potential “moral hazard” that could result (is resulting?). “Markets work best when participants have a healthy fear of loss. It shouldn’t be the role of the Fed or the government to eradicate it… I see no reason why financiers should be bailed out simply because the event they’re being harmed by was unpredictable.”

Eric Cinnamond at Palm Valley Capital Management published a Blog post called The Second Serve. Using tennis as an analogy, he essentially reminds investors not to double fault or put yourself out of the game. Markets are rallying, but it very well could reverse. “Large bounces in asset prices during bear markets are not unusual.” QE and trillion $ stimulus plans are helping fuel this rally. Eric says now is a great time to review your allocation strategies.

Instagram founder Kevin Systrom has been publishing a series of interesting blog posts leveraging “data science, machine learning and product development” at systrom.com (and corresponding GitHub pages).

Apple released Mobility Trends Reports, a data set available in a .csv file that “features daily changes in requests for directions.”

April 15

Major stock indexes retreated a bit. Here’s the 1 day:

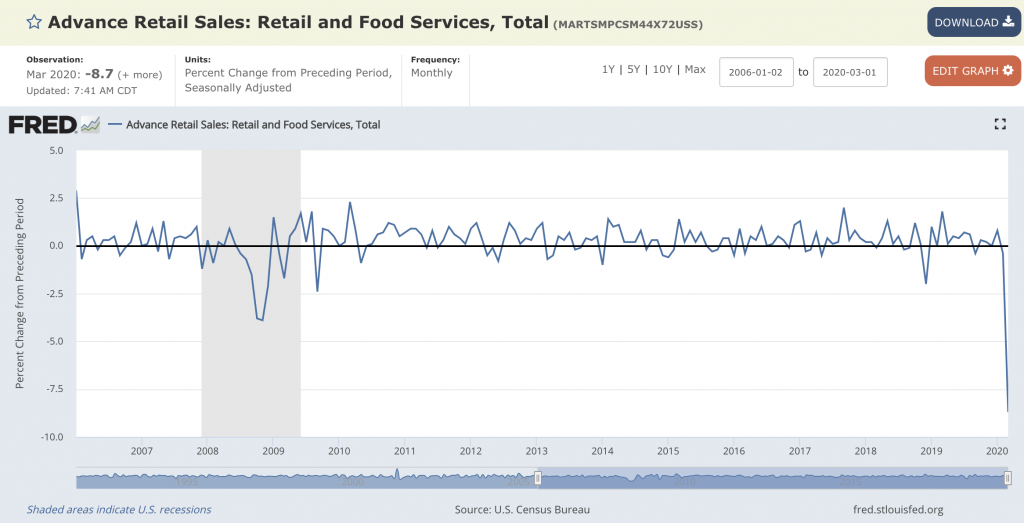

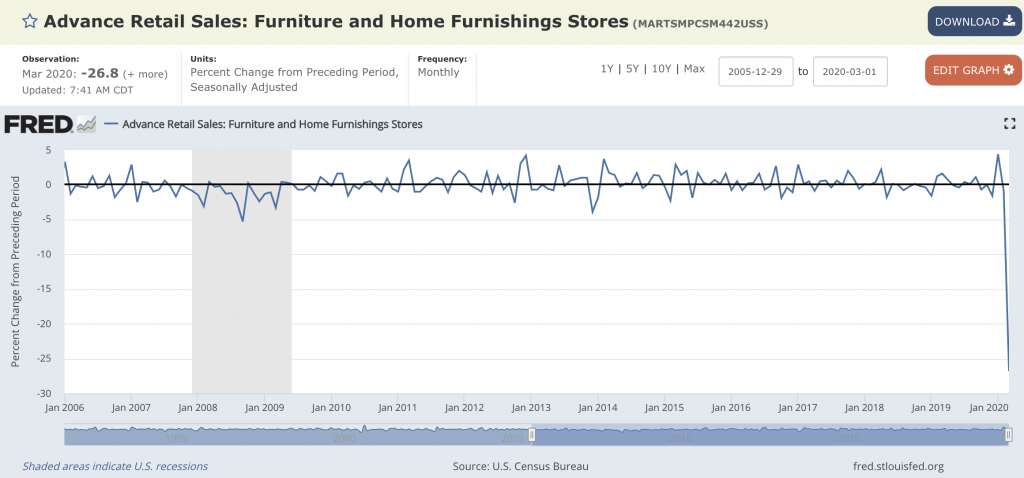

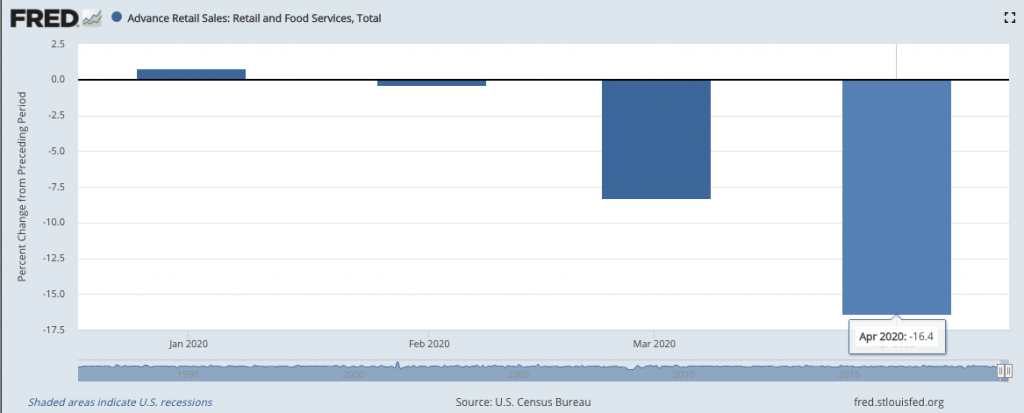

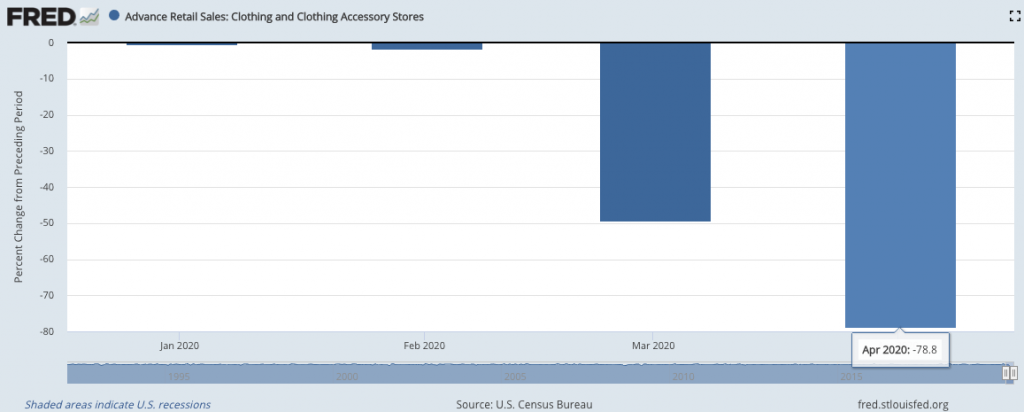

Check out this massive drop in retail sales:

Most businesses are being struck, including higher education. MIT published this Letter regarding MIT’s financial picture and next steps. The MIT President highlights budgetary changes (i.e., pausing hiring except for essential personnel, suspend merit increases, etc.) and provides some answers to significant questions, including “Will the fall semester be online?” We’ll soon know what college looks like for the fall semester. Decisions will have to be made quickly. But we have no clue what it’ll look like in the distant future. Are students going to pay up when they can’t get the historical on-campus experience they desire and value? Norms will change. What else will have to change with them? Some Universities will inevitably thrive, and others will die lust like businesses in most other industries.

Crescat Capital published their Q1 letter to shareholders where they warn, “We strongly believe that investors should be wary of getting sucked into the relief rally. Valuations are still historically high for the US stock market at large. Our macro model does not forecast an economic recovery any time soon. We expect the bear market to fully resume as soon as this week with the Q1 earnings season kicking off with a spate of grim reports… Based on the excessive debt, asset bubbles, and business cycle timing factors all lining up pre-coronavirus, we were already expecting a major global recession, not a quick bear market, and push to new highs. But throw in a global pandemic with almost the entire world population in lockdown, and global GDP could conceivably be poised to plunge at its highest rate ever. We must conclude that it is highly probable that there is much more downside ahead for the global economy and stock market before this recession is over… If anyone is looking for long opportunities in the market, we strongly believe precious metals, and the leading mining stocks in the industry across all capitalizations, are the place to be. They offer incredible upside leverage to the metals’ prices, even as their production is temporarily shut down.”

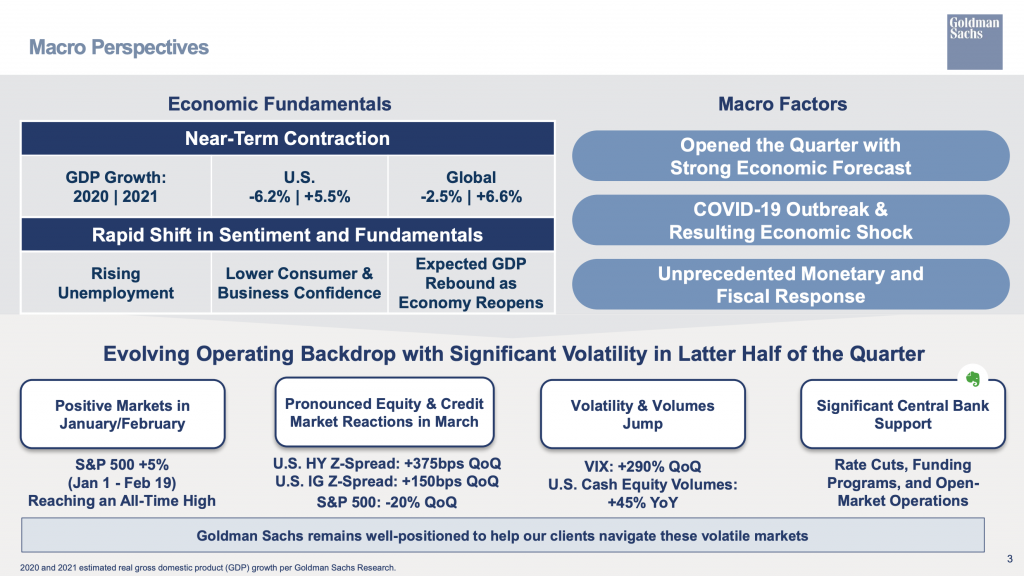

Goldmans 1Q20 earnings call was today. Here’s a slide from their presentation:

David Taggart published A Lesson In Bear Market Rallies, where he highlights what happens once we enter a bear market. “Since 1980, the average bear market rally lasted 108.81 calendar days or 3.63 30-day months. The shortest rally, and as you will see, I had to stretch some definitions for this, was 12 days, and the longest was 285 days… most bear market rallies last a lot longer than people seem to think they do… Maybe we have a second leg down, and maybe we don’t. But do not think that just because we hit a big low and we are definitely in a recession that we have to hit even lower lows anytime soon…or ever for that matter.”

I enjoyed listening to Pomp Podcast #268 w/ Mark Cuban. Sure, Cubans a billionaire. He’ll come out of this thing just fine even with his entertainment businesses getting crushed. Ignore the fact that he’s a billionaire and enjoy his uplifting tone and message. He talks about how much opportunity crises and volatile environments create; America 1.0 vs. the future, 2.0. Minute 29 is an excellent example of his mindset: “We’re not just going to do things the same way. Let’s come up with a vision, and let’s get fired up… I want to see new products and services, those new visions because goddammit if we went through all this shit, I want it to be for something… all those people who died, all those people who suffered, let’s turn this into something that makes this country better.”

Another good recent podcast episode comes from Howard Lindzons’ Panic with Friends series. His episode with Samantha LuDac (a down to earth macro analyst) was both informative and funny.

April 16

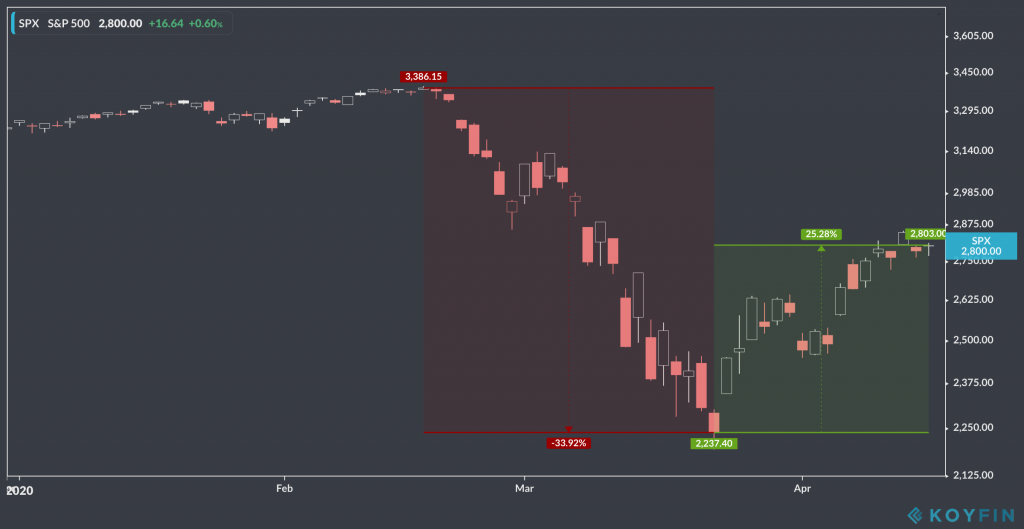

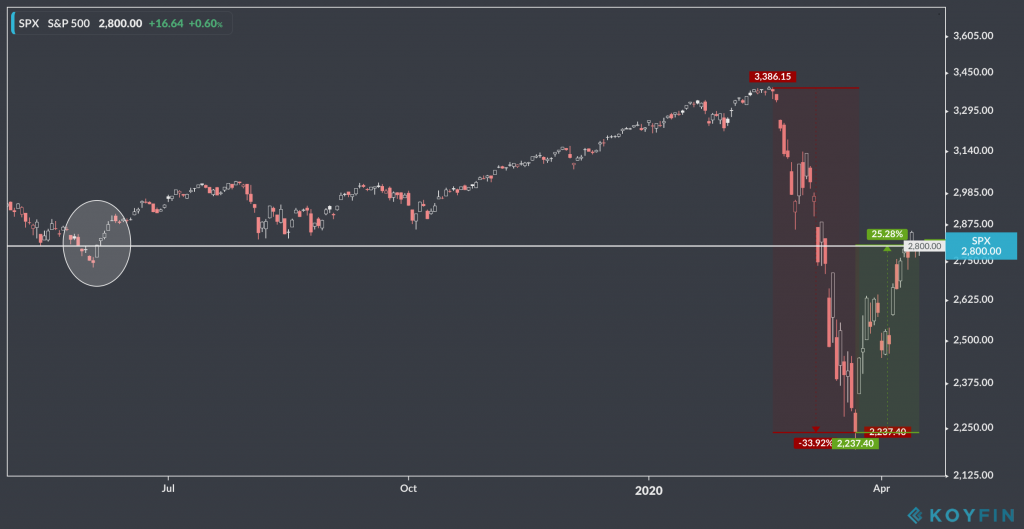

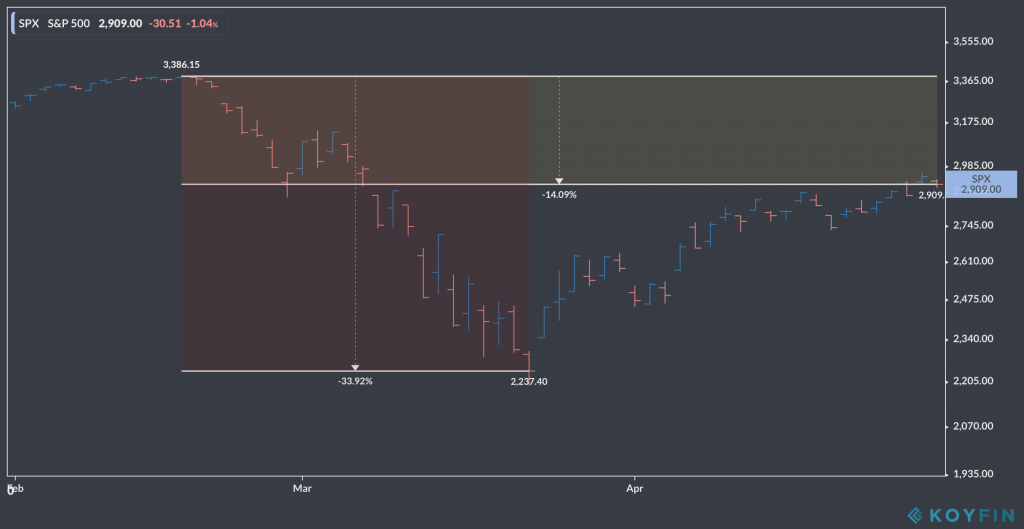

I didn’t catch the exact tops and bottoms, but this $SPX chart is directionally accurate. Greater than 30% drop from Feb 19 to Mar 23, and then a greater than 25% bounce from the low to today.

Drawing a horizontal line at $SPX 2,800 shows its back to June 2019 levels. Things seemed pretty damn good in June 2019. It hasn’t even been 1 year.

Eric Cinnamonds blog post (The Second Serve) that I highlighted on April 14th resonated with me over the past couple of days, given this >25% $SPX bounce.

Ali Hamed published Why is Private Credit So Quiet Right Now? Although focused on credit markets, his advice is applicable everywhere. Credit markets aren’t self-contained. The economy is a system comprised of interconnected markets. Ali succinctly pinpoints how early it is. “For a lot of investors, who have waited ten years for a downturn… there is a temptation to pull the trigger. But it’s better to be too late than too early. Just wait… things will break, but it’ll take time. 3–6 months, maybe. But there isn’t going to be a snapback of the economy. Many small businesses are simply closed forever. The government can stimulate a market, but it cannot mimic the real economy.”

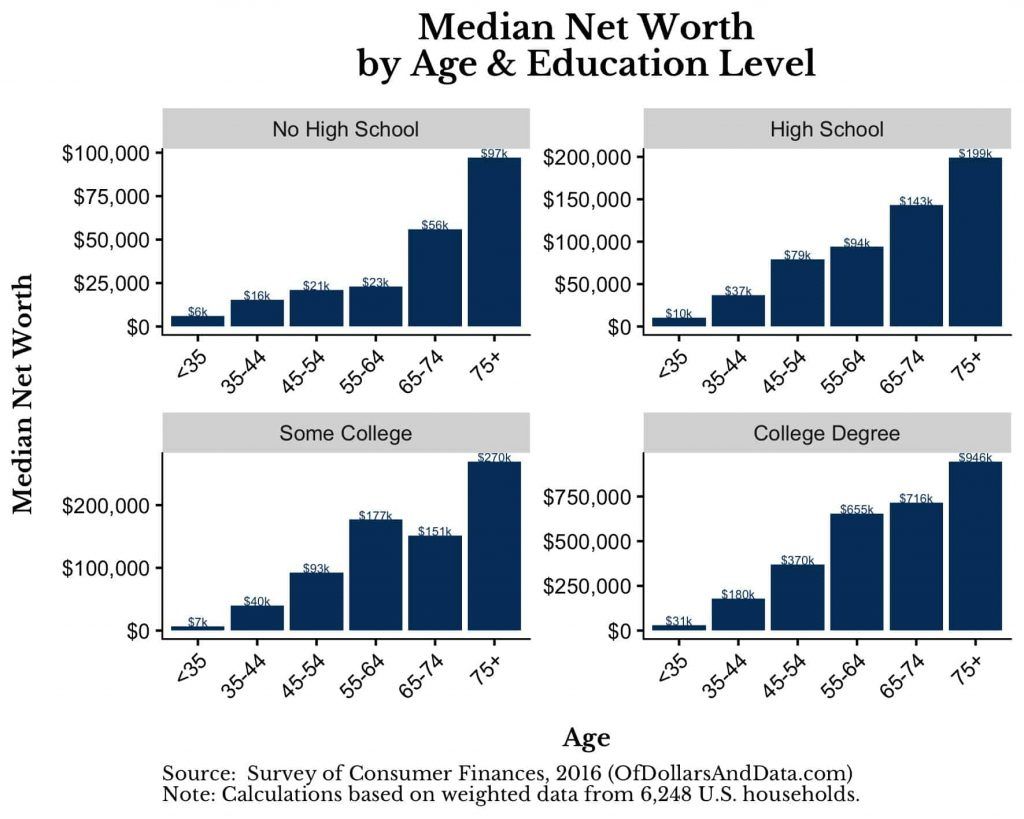

Nick Maggiulli published What is the Average Net Worth by Age and Education Level? Investing has dominated the majority of this page, but personal finance is more important, and Net Worth is the way you measure your household and progress. This is why I love Personal Capital so much (they do a great job focusing on helping you track your Net Worth). Nicks’s post helps readers identify segments to compare their net worth and explains why the segmentation is essential. It’s one of those posts that stirs up a bunch of emotions because it highlights the impacts of inequalities.

April 17

Friday. Stocks rallying some more, for some reason. Crude oil is down to levels not seen in almost 20 years. If being conservative is good enough for Charlie Munger then it’s good enough for me. Jason Zweig interviewed him in The Phone Is Not Ringing Off the Hook.

The Coronavirus Task Force announced Guidelines for Opening Up America Again during yesterdays briefing.

The WSJ published A Second Round of Coronavirus Layoffs Has Begun. Few Are Safe a few days ago. The authors state that the first wave of job losses was comprised of workers from “restaurants, malls, hotels, and other places that closed to contain the coronavirus pandemic. Higher skilled work, which often didn’t require personal contact, seemed more secure.” They say a 2nd wave has come for safer jobs due to falling sales (corporate lawyers, healthcare workers not on the pandemic front line, etc.). It is now extending to state and local governments due to falling tax revenue. High flying startups continue to prep for slower growth as well. Carta CEO Henry Ward shared Carta’s covid-19 layoff after laying off 16% of their team. This is a company that raised $300M at a nearly $2B valuation less than a year ago and is rumored to be actively raising another up-round. Opendoor, most recently valued at almost $4B after raising ~$300M a year ago, parted with 35% of their team. The most recent jobless claims count for the past week came in at 5.2M, for a four week total of >22M. How long it’ll take for jobs to rebound back is dependent on many factors, but it won’t be happening anytime soon.

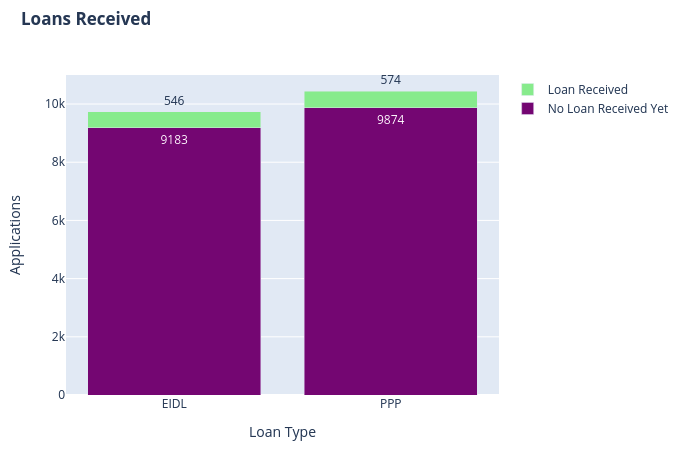

In this bleak environment, yesterday’s announcement that “the $349B loan program for small businesses” ran out shouldn’t be surprising. The demand is high. But I’m left wondering who it helped and how much it helped? To my knowledge, the details regarding applications, application results, and funding status haven’t been made public. To be clear, I’m not knocking the program(s). I’m just curious. The SBA supposedly processed ~14 years’ worth of loans in less than two weeks. The early hiccups and confusion are easily understood. I’m simply curious about the effectiveness. Should another $250B be added, or should they be improved first? (Admittedly, I haven’t looked at the newer Main Street Lending program yet.)

Here’s what I’ve gathered so far (not much and that’s my point):

| Total Applications | ? |

| % of Eligible Payroll who Applied | ? |

| % of Eligible Payroll Approved | ? |

| Approved Applications | 1.66M |

| Declined/Neglected Applications | ? |

| Declined/Neglected Reasons | ? |

| Total $ Amount Applied for | ? |

| Avg $ Amount Applied for | ? |

| Total $ Amount Approved | $349B |

| Avg $ Amount Approved | ? |

| Total $ Amount Distributed so far | ? |

Here are some of the initial questions I think all of us should be asking:

- What’s the big picture look like for the impacts of the program? What’s the return on investment for the broader economy?

- Were applications genuinely representative of the profile of small businesses in America? Who might have been left in the dark, and why?

- Where are the big holes? What type of businesses were either excluded from participation or unintentionally neglected due to unfavorable risk/reward/effort factors?

- Does the current design of the program help ‘save’ small businesses, or better serve as an alternative form of unemployment benefits?

- How would the program be redesigned for various phase 1 & 2 reopening scenarios that could be modeled?

- Should another $250B be earmarked, or should the program be redesigned/improved first?

- Is the percentage of the total $1T+ stimulus package allocated to “small biz” the right amount?

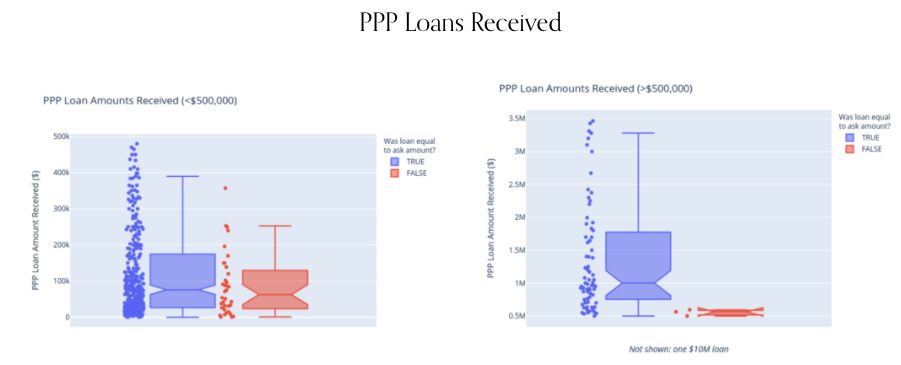

I found CovidLoanTracker.com, but it’s just based on survey results. Permanent Equity is currently conducting a survey as well. Survey results can’t come close to Bank & SBA actuals, but this is the best we have right now. The results make you question the picture being painted during Coronavirus Task Force briefings. Only ~5% of applicants have received a loan, and applicants requesting larger amounts are much more likely to receive a loan equal to their requested loan amount. So, a reasonable question to ask is if the mechanics of the program or application process result in favoring certain types and sizes of businesses over others, thus neglecting a sizable population.

Until official details are released from an authoritative source, we’ll continue to feel confused and disheartened by the overwhelming anecdotal evidence that there’s a disconnect brewing between Wall Street, Main Street, and the CARES Act.

April 18

Saturday.

It seems like a good time to recognize where the health crisis stands compared to March 15 when I said, “It’s all about doing your part to decrease stress on the healthcare system ultimately.” Social distancing is working. There have been almost 40,000 COVID deaths in the US. Had social distancing measures been laxer, projections had us seeing more like 100,000+ deaths around this time. While 40,000 deaths are tragic (and there will still be many, many more), it’s worth acknowledging that it could have been worse. It appears like we may be safe saying that we successfully avoided the major catastrophic vision of having overrun medical facilitates that have to turn away high risk, vulnerable patients at their front door. According to recent white house claims, nobody who has needed a ventilator in the US has been denied access to one. That’s a win. It could have been worse. And it most certainly would have reached that point if not for social distancing. This post isn’t to claim victory or to celebrate. Many people have died, and many more will. Many healthcare workers continue to exhaust themselves physically and mentally while risking their lives each day, taking care of the ill. That won’t stop anytime soon. But at least most of the people who need care have been able to receive it. That’s one for the win column.

Hopefully it wasn’t all for nothing. Hopefully some states won’t make it even harder for other states. Look at this recent shot from Jacksonville shortly after opening their beach back up.

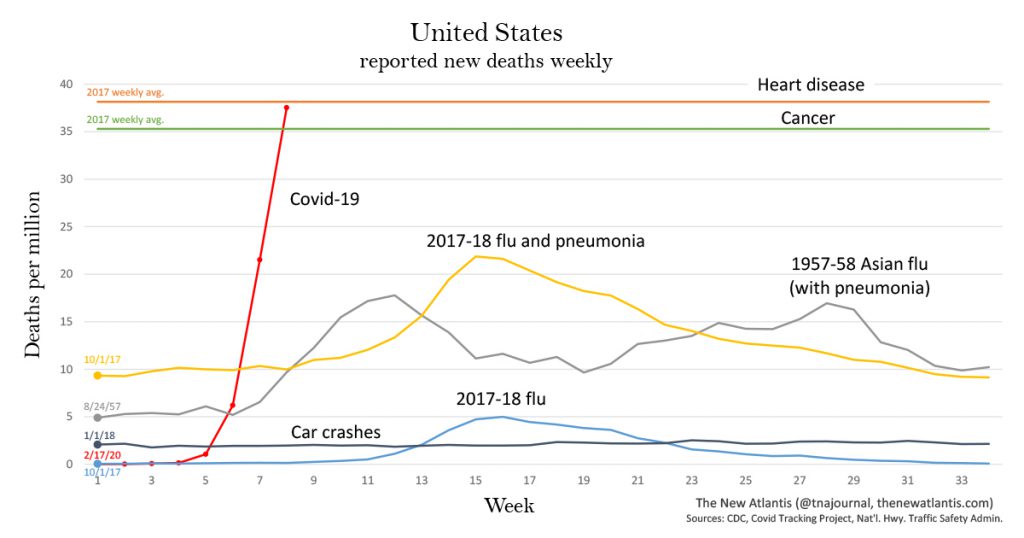

And to all of those people who enjoy touting that COVID-19 shouldn’t be getting special attention compared to more common killers, check out this chart from The New Atlantis in Not Like the Flu, Not Like Car Crashes, Not Like… (“But last week, reported U.S. Covid-19 deaths were just shy of the normal rate from heart disease, usually the leading cause of death.”).

Listening to podcasts with successful entrepreneurs this week has shed a positive light on the fact that this time period can be viewed as an epidemiologist’s dream. A lot of goodwill come from all of this. Hopefully, many new norms that get established will last. We’ll undoubtedly be more prepared for future health crises. That would be another one for the win column.

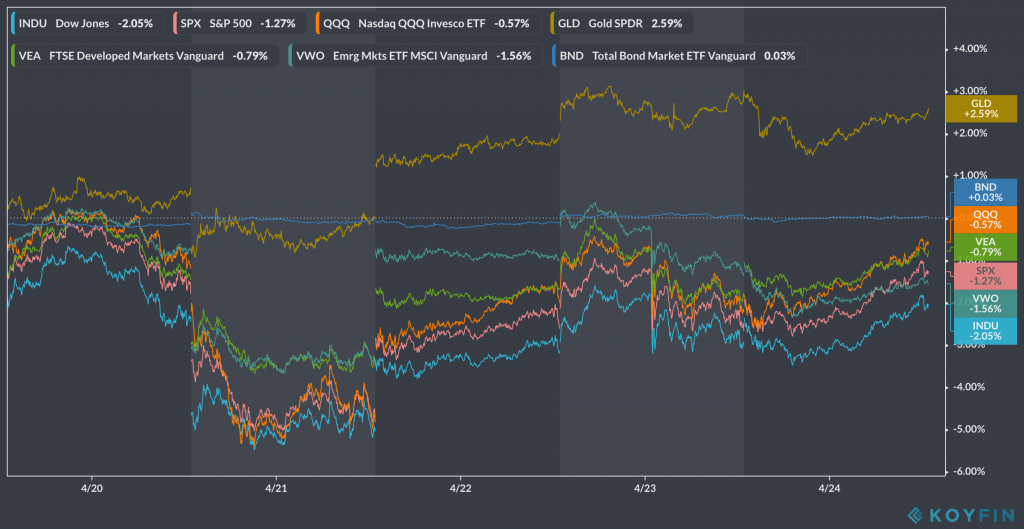

April 20

Monday. US Oil dominated market chatter today. The May Futures contract settled at -$37.63/ barrel. I don’t know much about the oil market, but I understand that demand decreased, supply was flooded, and there’s diminishing storage capacity. I’m sure there are many other factors at play too. I’m assuming this unprecedented drop will impact equities sooner than later. Major indexes were slightly down on the day.

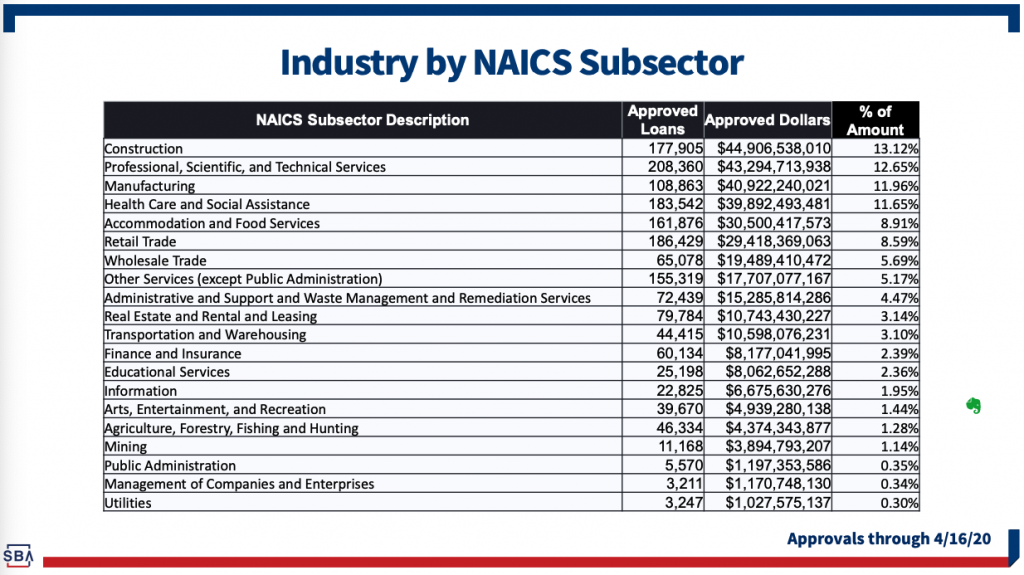

The SBA published a PPP Approval Report (through 4/16/20). Assuming an estimated 30.7M small businesses in the US, ~5.4% received loans from the PPP so far (obviously not all 30.7M need a loan). The report revealed:

- Average Loan size = $206k

- Approved Loans =<$350k made up ~31% of Approved Dollars

- Approved Loans > $1M made up ~44% of Approved Dollars

- Approved Loans > $2M made up ~29% of Approved Dollars

Here’s a shot of the breakdown by NAICS Subsectors:

Recent headlines scream about Harvard (~$8.6M), Ruth’s Chris (~$20M), and other non-stereotypical small businesses receiving CARES Act dollars. Shake Shack is in the news for taking $10M. And then returning the $10M. The National Restaurant Association CEO told Newsweek, “There are more than 1 million restaurants in the U.S., employing 15.6 million people…” Many of them include larger, well-known brands like Ruth’s Chris and Shake Shack. All of the employees of these businesses are important. But it’s worth questioning how the PPP can be improved to focus more on need-based lending. This isn’t to say that Harvard and Ruth’s Chris aren’t in need. Maybe they are, but maybe they aren’t compared to other loan applicants. Shake Shacks CEO was able to find an alternative source relatively easily. Size tends to provide optionality, which is precisely why it’s worth redesigning the PPP before funding it with another $300B, and then another, and then another. It’s also worth questioning if non-essential and essential businesses should really be treated the same? Don’t non-essential businesses need a loan (on average) more than those who are still able to operate to some degree? In Shake Shack is returning its PPP Loan. Here’s why, the CEO explained the confusion around the program, why they applied to begin with, how they’ve been able to access capital alternative to the PPP loan, and how the program could be improved for restaurants across the country. I think their 3rd suggestion is obvious and interesting. “Eliminate the arbitrary June forgiveness date for PPP loans. This virus has moved in waves with a different timeline in different parts of our country. Instead, make all PPP loans forgivable if a minimum of 6 months rehires an adequate number of employees following the date that a restaurant’s state (or city) has permitted a full reopening to the public.” This dovetails into a reality check from Dr. Craig Smith.

In COVID-19 UPDATES FROM DR. SMITH, he makes a good point about the future. He urges us to rid “COVID-free” from our vocabulary. In America 2.0 (as Mark Cuban calls it), our new normal needs to be “COVID-safe.” COVID is here to stay. We won’t be 100% free of it. Going forward, we should only think in terms of relative safety. This helps prove the point the Shake Shack CEO is trying to make. Communities will rebound on unique timelines. It doesn’t make sense for PPP loan dates to be generic across the country. And we all need to think and act with a bias towards encouraging a COVID-safe world going forward.

April 21

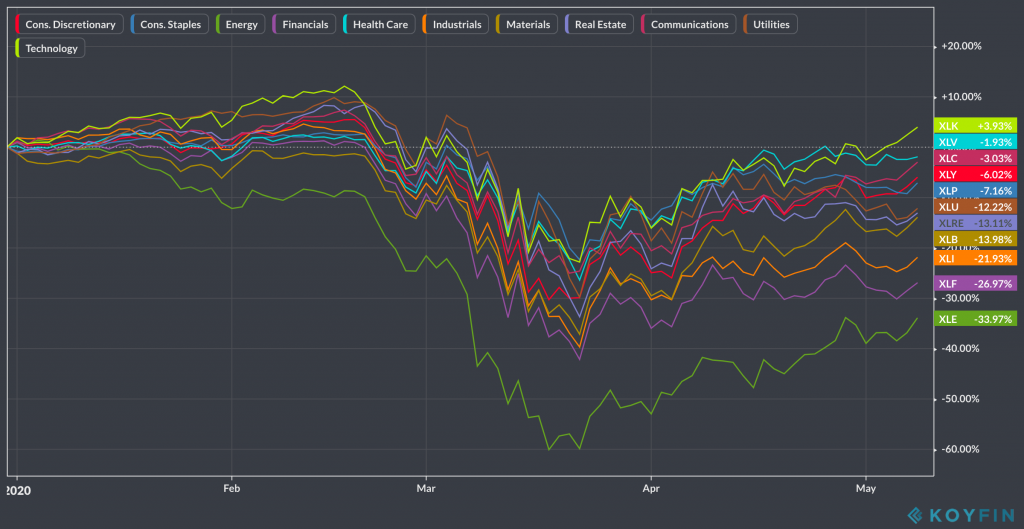

Major indexes went down 2-3% today. Tech was one of the leading down sectors (for a change), despite dominating recently.

Mnuchin announced that the Senate Passed another stimulus package, totaling ~$480 Billion during todays task force briefing. According to this Bloomberg article on the package, it includes:

- $320B more for PPP

- $60B for EIDL

- $75B for hospitals “with a significant portion aimed at those in rural areas”

- $25B for COVID-19 testing

Trump tweeted: “In light of the attack from the Invisible Enemy, as well as the need to protect the jobs of our GREAT American Citizens, I will be signing an Executive Order to temporarily suspend immigration into the United States!” Details are unknown.

Georgia announced plans on opening gyms, nail salons, bowling alleys, restaurants and movie theaters over the next week. Apparently the Guidelines for Opening Up America Again presented to the country last week were just that; guidelines. Governors don’t have to follow them.

A new ESPN documentary series called The Last Dance about MJ and the Bulls appears to be giving quarantine fav, Tiger King, a run for it’s money. I’m not a basketball or sports fan myself, but I’m enjoying it so far. Season 3 of Fauda and Ozarks are also popular shows these days.

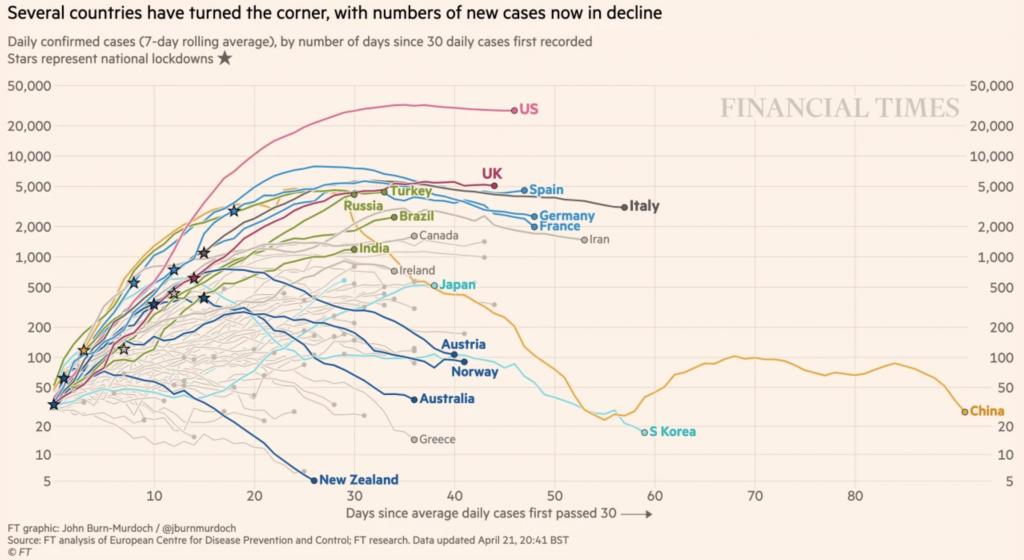

Here are some positive signals from FT.com. But still a long way to go, especially for frontline workers.

April 22

Another green day 🤯. Oil bounced. Gold up 2%. Gold miners up over 6%. $SPX up 2.3% with tech leading the charge up 3.8%.

KKR published Keep Calm and Carry On on Apr 15. Interesting excerpts:

- “No doubt, we are impressed with the speed and size of the fiscal and monetary response around the world, but we think that Covid-19 is hitting the system at a time of unique vulnerability. Corporate margins and financial leverage are both at historic peaks, and geopolitical tensions were already running hot. So, while not ever losing sight of the human tragedy, there are important market considerations that all investment professionals must consider in this new environment in which we find ourselves.”

- “In terms of economic growth, we are looking for a sharp downturn during the second quarter, followed by more of a U-shaped recovery than a V-shaped one.”

- “Using several different big data sources, we estimate that hours worked in the United States have fallen 62% in just the past few weeks. Europe is not that dissimilar, we believe. The enhanced unemployment benefits of the government will likely help… Unfortunately, as we detail below, we are concerned that there will be an employment ‘hangover’ effect associated with this pandemic, as the global economy is likely to be reshaped quickly towards a more digitally-oriented society that favors national champions. Looking at the big picture, we think that the road ahead will be a bumpy one for the global economy and its constituents.”

- “All told, we now forecast peak-to-trough decline in U.S. GDP to reach 12%, which is substantially worse than the four percent drop during the Global Financial Crisis (GFC).”

- “So, we would think about the aftermath as somewhere between what happened following the ‘shock’ of September 2001 and the market crash of 1987. If we are right, then we are likely to have more rolling recessions globally following the huge downward shock we just experienced with the onset of Covid-19.”

- “we think that risk assets are close to appropriately valued for the current outlook. Credit appeals to us more than what Equities seemingly offer…”

- “Expect continued massive stimulus from central banks and government authorities to offset this downturn… it still has a lot of firepower left if financial conditions do not begin to improve.”

- “From a bigger picture, long-term perspective, the onset of the new coronavirus will, in our opinion, further throw sand in the gears of globalization ― interconnected, lowest cost supply chains in particular ― and likely fuel a re-examination of over reliance on any one nation… We envision a more regionalized model, with the Americas coalescing around the United States and Asia around China.”

Richard Branson published An open letter to Virgin employees. I found it to be incredibly heartfelt and enlightening. I don’t know much about the many different Virgin business lines, but this letter highlighted how wide-reaching Virgin is. Regarding the crisis, we should value observations from proven entrepreneurs like Richard Branson. He wrote, “Over the five decades I have been in business, this is the most challenging time we have ever faced. It is hard to find the words to convey what a devastating impact this pandemic continues to have on so many communities, businesses, and people around the world. From a business perspective, the damage to many is unprecedented, and the length of the disruption remains worryingly unknown.”

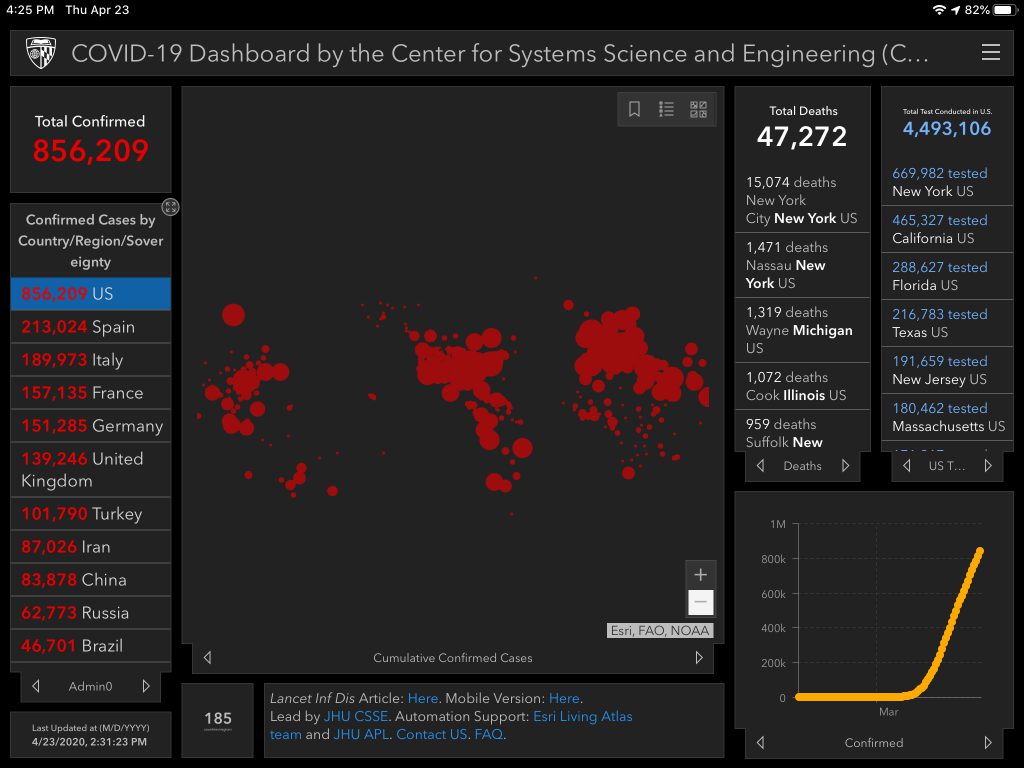

April 23

Major indexes closed relatively flat. $SPX closed down .06%. $GLD up .9%. $BTC is up almost 6% on the day so far (~+16% mtd).

Jobless claims rose another ~4.4M. The total for the last 5 weeks is ~26M. For context, the entire GFC of 08-09 saw just over 37M.

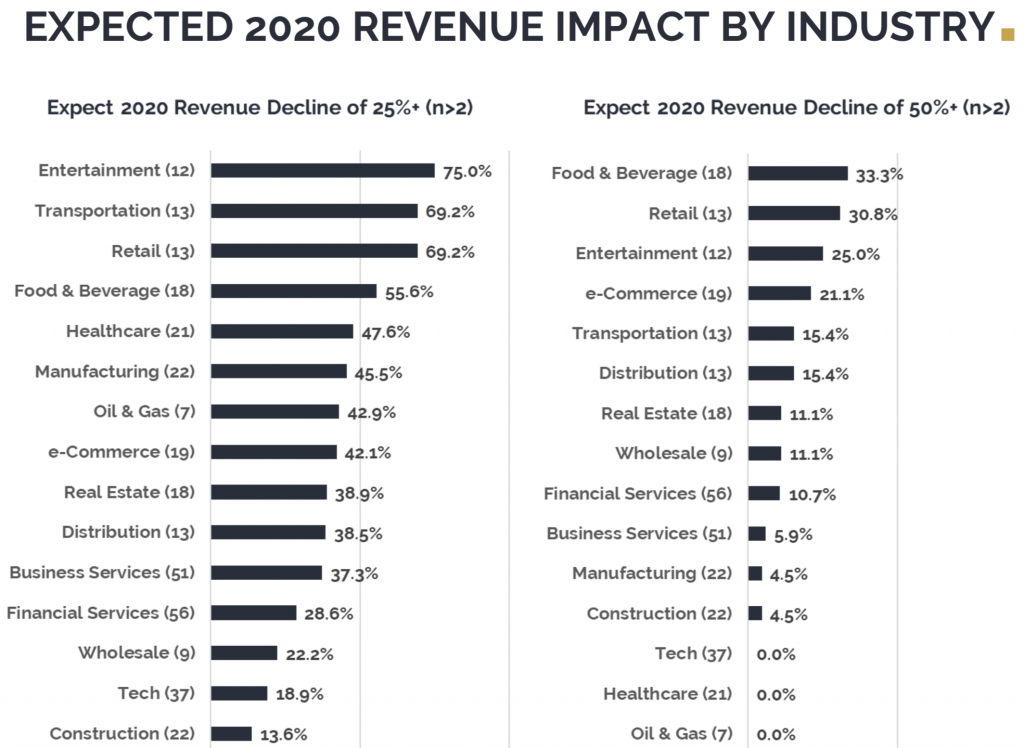

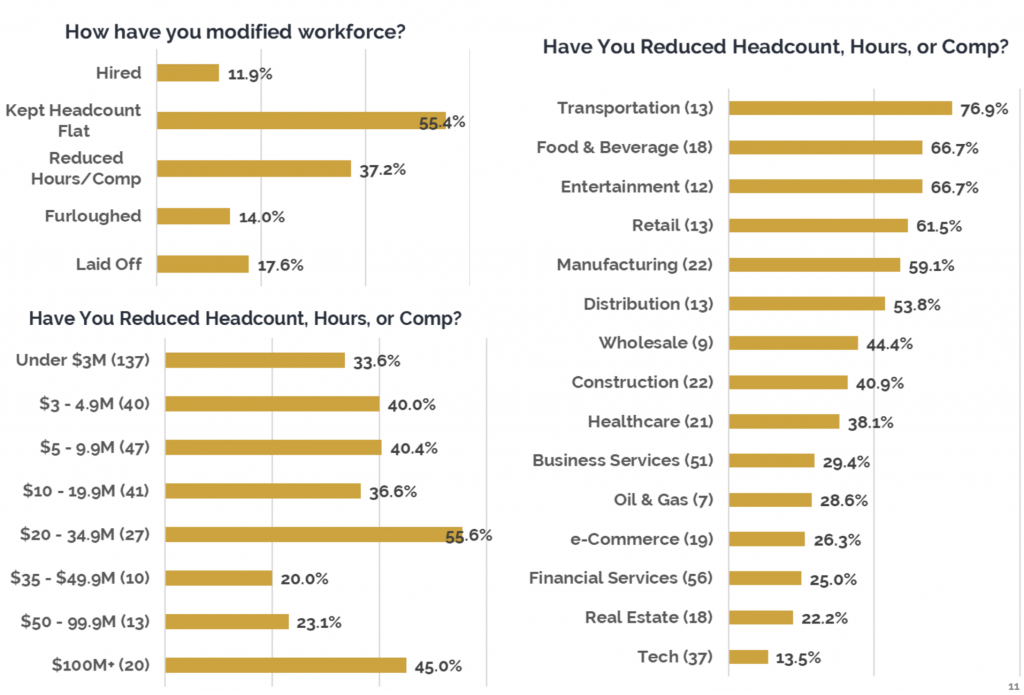

Permanent Equity published Owner / Operator COVID-19 Impact Survey with input from 336 owner/operators in 43 states. ~41% of respondents have company annual revenue under $3M. An optimistic takeaway is that 57.4% said their business can survive while sheltering through 2020 or longer. 79.2% applied for government aid, including 100% of those in Entertainment and 94.4% in Food & Beverage. However, only 35.7% who applied have received it so far.

It’s estimated that roughly 2.7B people (~1/3 of the worlds population) are now under some sort of movement restriction due to coronavirus. That’s crazy!

CNN published Preliminary antibody testing in New York suggests much wider spread of coronavirus. The results could (well, are) being interpreted many different ways. I think it’s too small and uncontrolled of a study to draw too many conclusions from. While I’m sure it’s helpful to scientists, I don’t think it’s helpful to the media or most of the public.

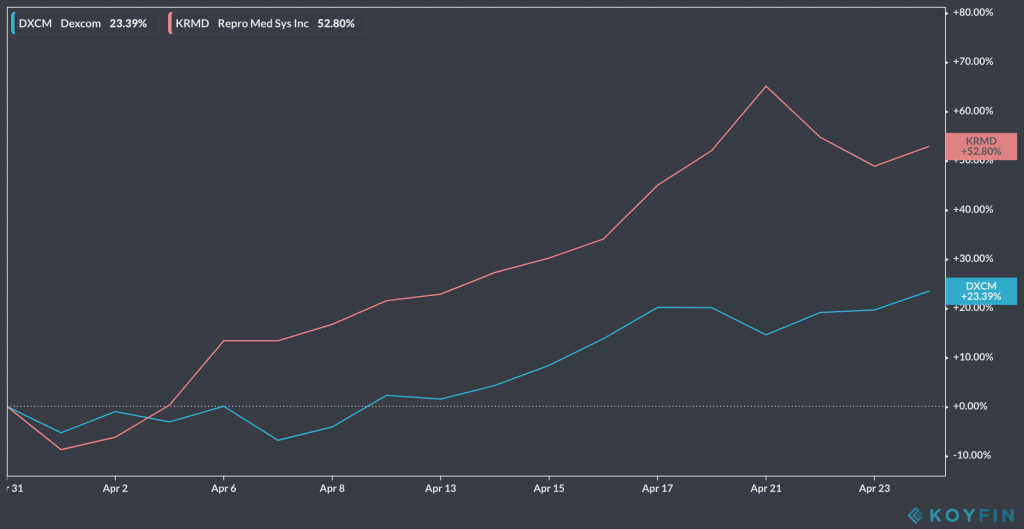

April 24

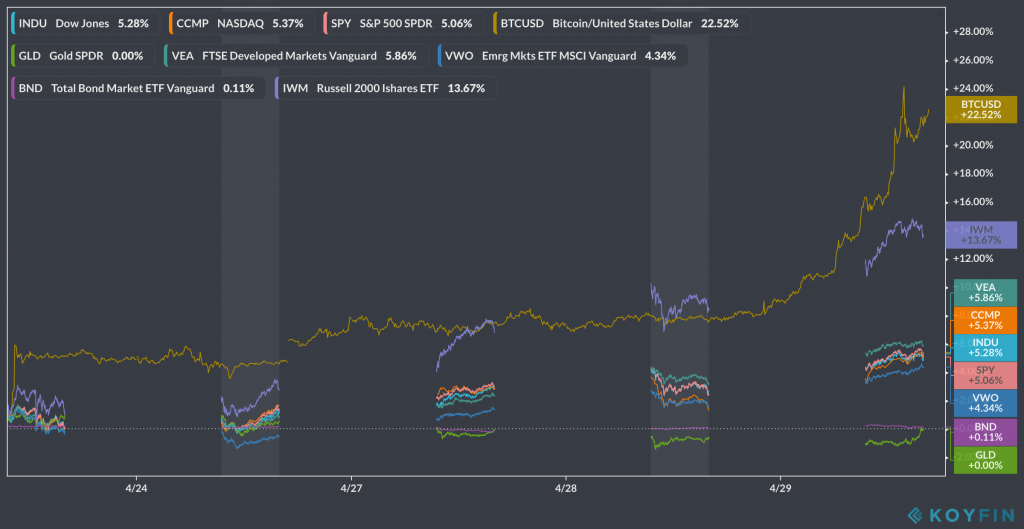

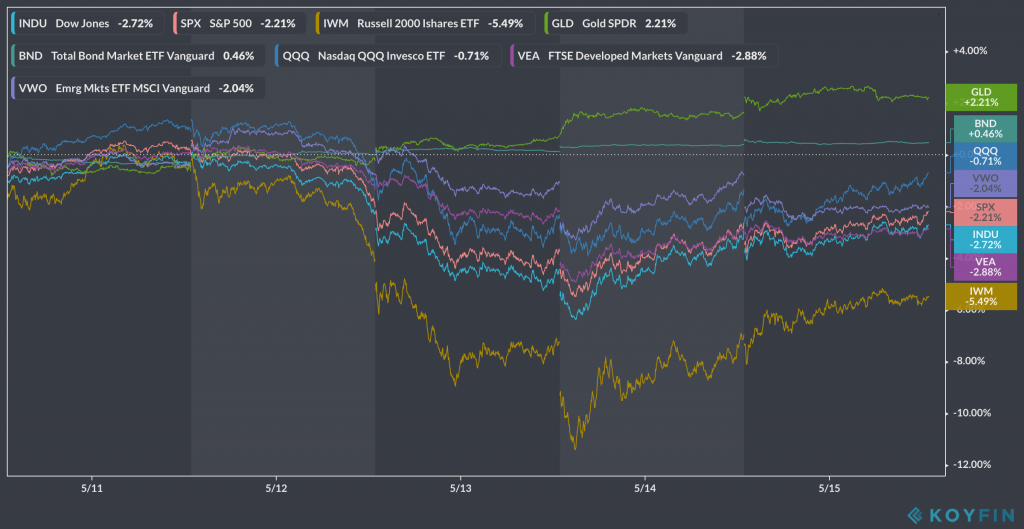

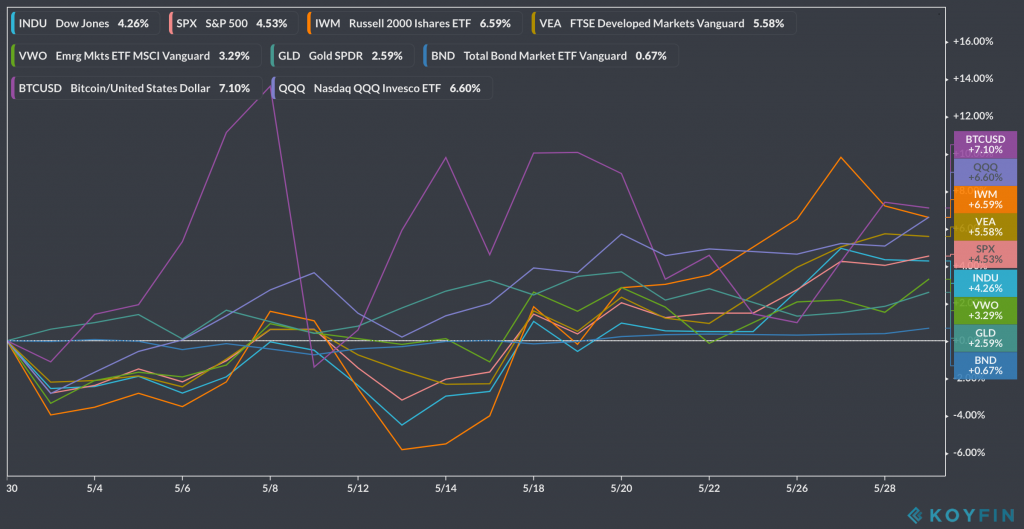

Friday. Here’s what the charts say for the last 5 days:

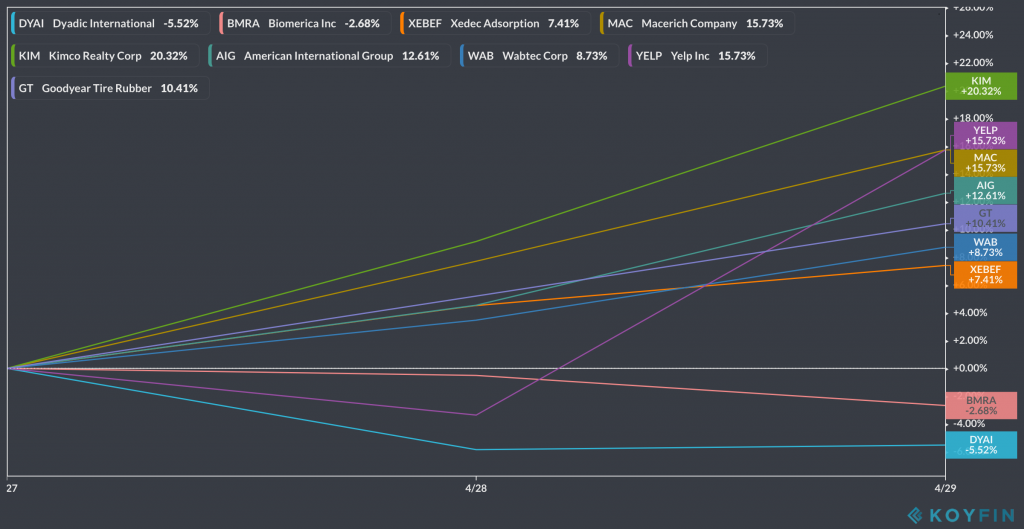

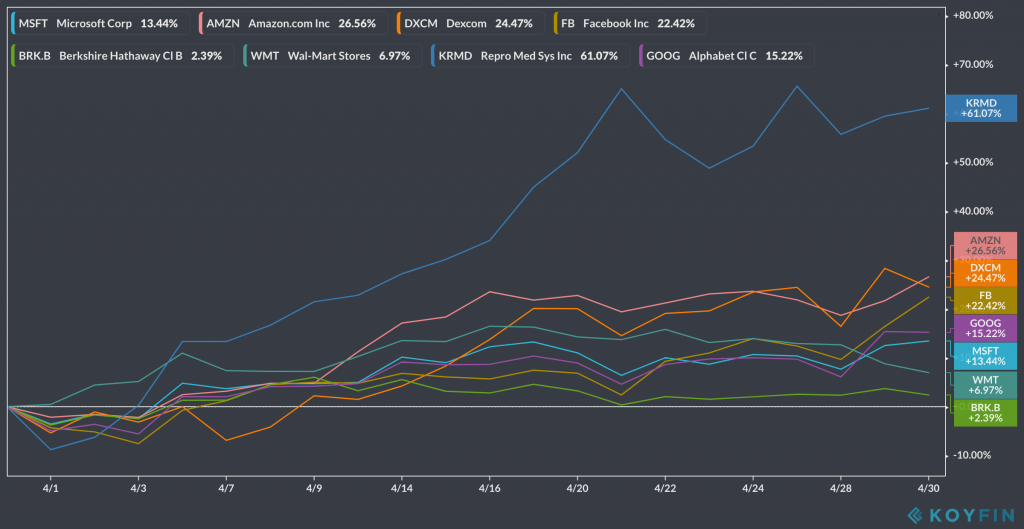

2 of my favorite single stock holdings had big days today and have been crushing mtd.

Both my dog and I turned another year older this week. I’m thankful that she, my wife, and I are all healthy and that both of us are still employed.

For those of you who care about “fintech,” FT Partners published Understanding the Impact of COVID-19 on FinTech. They cover an overview of the stimulus package, PE & VC impacts, public market impacts, macro indicators, and the impact on financial services.

I came across this cool COVID-19 HubSpot page which is “based on aggregated data from over 70,000 HubSpot customers globally.”

Turn the sound on and get a glimpse of yesterdays task force briefing:

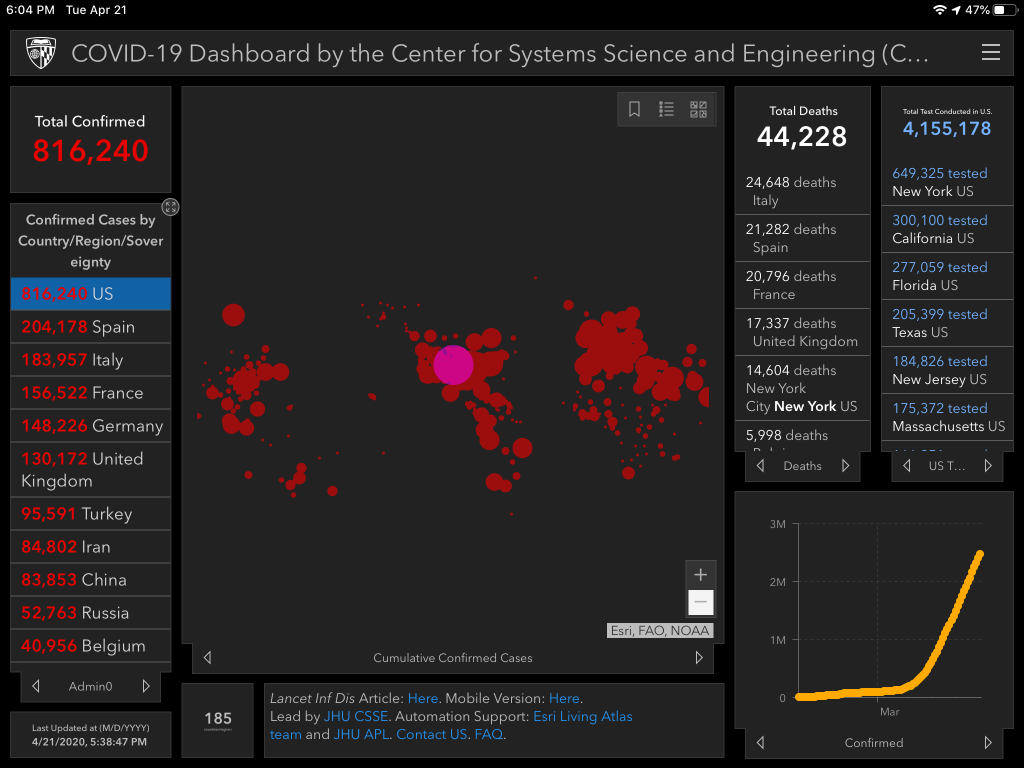

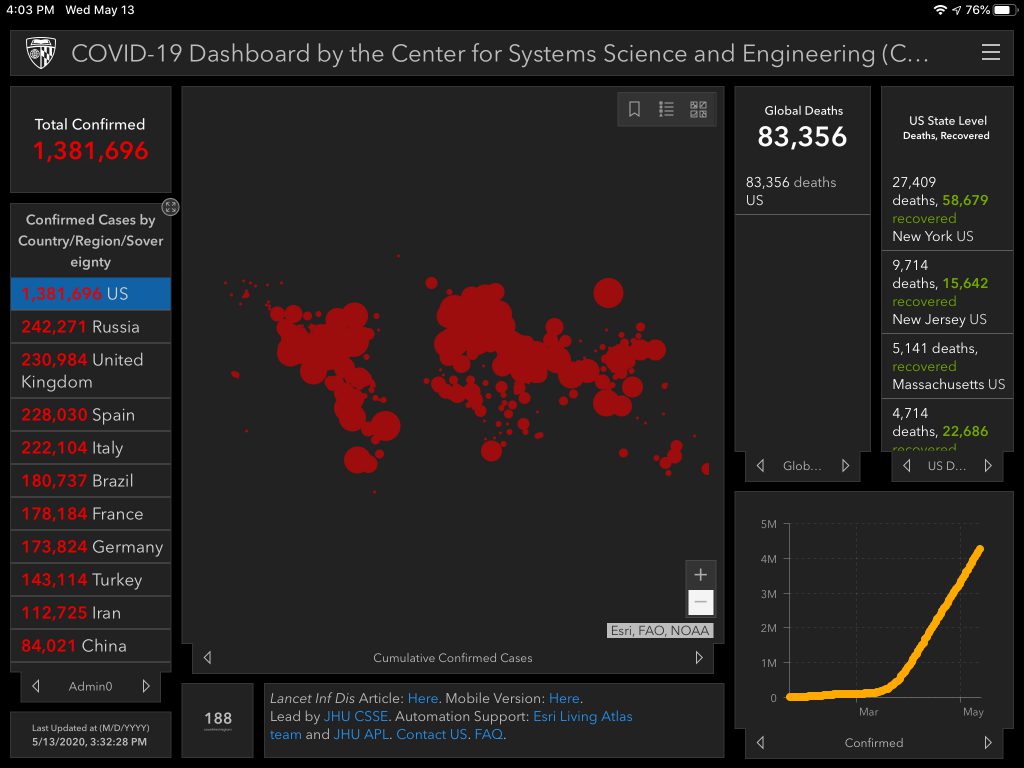

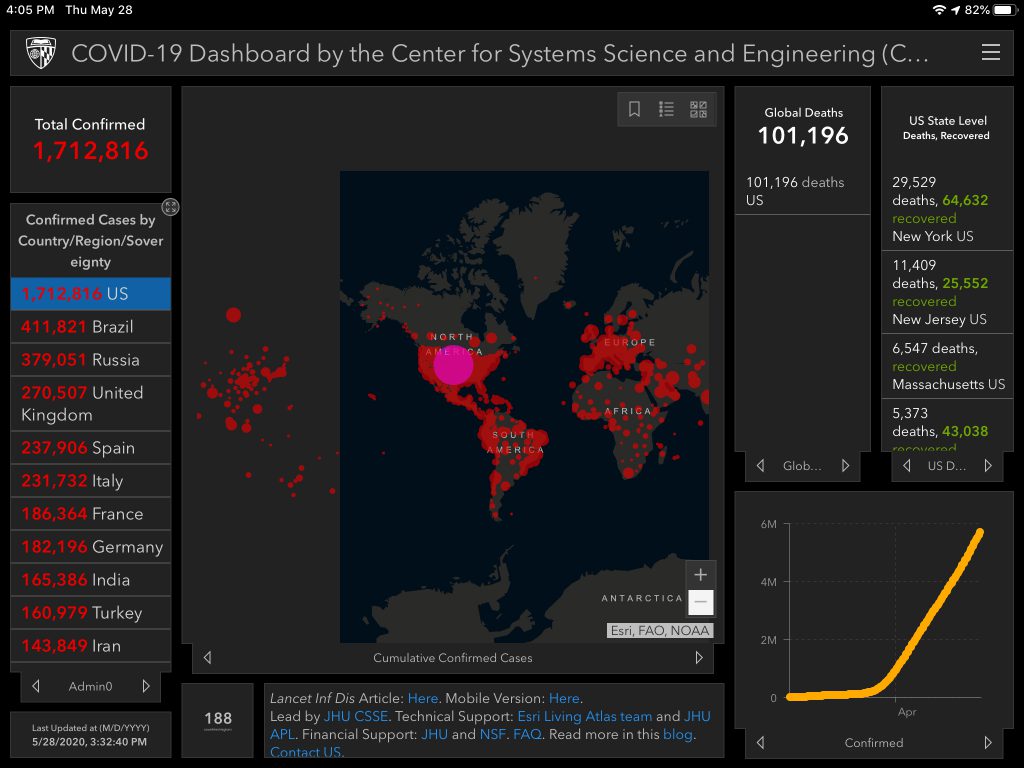

We sadly crossed 50,000 deaths in the US and are close to 200,000 worldwide.

April 26

Sunday. Major markets are still sleeping.

As someone who tends to shy away from large crowds, I’m really enjoying the virtual music performances. Both the Foo Fighters ‘Times Like These’ cover and Post Malone/Travis Barker Nirvana Tribute Concert and are raising awareness for the COVID-19 Solidarity Response Fund for WHO. Turns out Posty is actually really talented. Who knew?

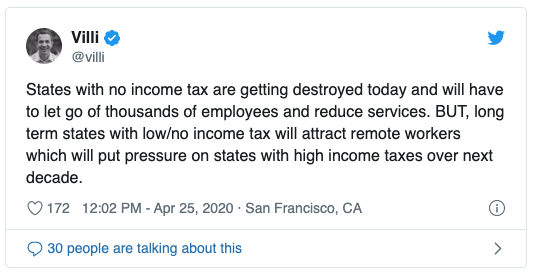

Villi wrote a thought provoking tweet yesterday:

Bill Gates published The first modern pandemic, The scientific advances we need to stop COVID-19. It’s the most succinct single artifact I’ve read on the state of our current COVID-19 world. It covers the Gates Foundations role, vaccines, contact tracing, testing, reopening, and more. It’s worth noting that Bill says, “I see global innovation as the key to limiting the damage. This includes innovations in testing, treatments, vaccines, and policies to limit the spread while minimizing the damage to economies and well-being.” It’s noteworthy because many are suggesting that globalization progress should reverse the trend because of current events since every country has been forced to rethink their supply chain and reliance on others. In KKRs report Keep Calm and Carry On, they wrote, “We envision a more regionalized model, with the Americas coalescing around the United States and Asia around China.” Personally, I can’t help but think that free-trade and international collaboration is better than not, for similar reasons, Bill thinks global innovation is the key to limiting damage. I’m reminded of reading ‘The World is Flat’ by Thomas Friedman as a college student in 2005. I guess it had a lasting impact on me. It’s time to start formulating my theory for how the world may change. KKR’s prediction sounds reasonable. Will it play out that way, or are other changes to international trade more likely? What would that timeline look like? What portfolio asset allocation makes sense in that case? What risk is there to the portfolio if those trade predictions don’t play out? These are the types of questions non-TDF investors need to think about.

April 27

Monday. Lots of green. Dow and S&P 500 both up ~1.4%. Russell 2,000 up ~4%. Financials & Real Estate were the leading sectors today. Gold was down .6%.

I still believe the stock market is wildly disconnected from the economy right now. I’m not materially changing my portfolio allocation. But I’m salivating over the March lows.

The SBA began accepting PPP applications again. There are a few changes since the first round. For instance, no single lender is allowed to lend more than 10% of the total PPP funds. And E-Tran is rate limiting each lender at 350 submissions per hour. So, how many days will it take for all available funds to be allocated? Likely just a few. The first round took 13 days but this round is starting off with a backlog of applications left hanging from the previous one.

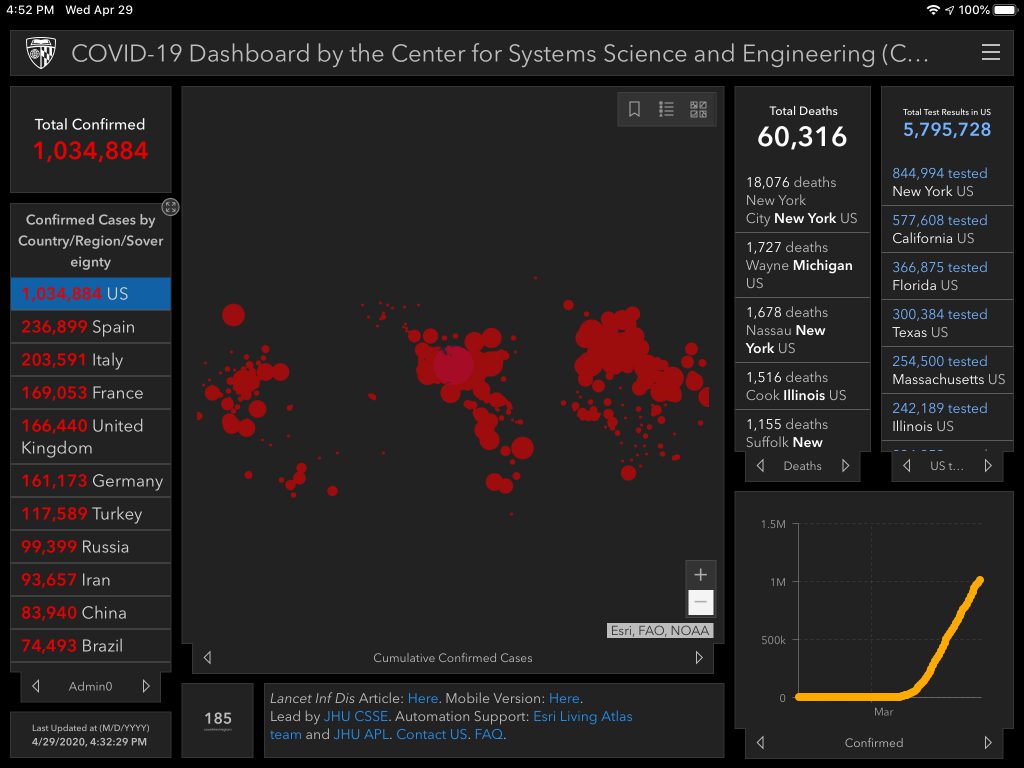

The world now has over 3 million confirmed cases and 210,000 deaths.

April 28

The Russell 2000 was todays leader again, up 1.5%. Other major indexes were down slightly. $IWM has separated from the pack over the last few days, up over 9%.

The Fed announced expansion of the Municipal Liquidity Facility (MLF). The program originally had them buying bonds up to 2yrs in duration but now they’ll buy bonds up to 3yrs. They’ll also buy debt from cities with 250k+ residents and counties with 500k+. One can’t help but wonder if actions like this will lead to moral hazard, as Howard Marks initially questioned a few weeks ago in his memo Knowledge of the Future.

My county is beginning to “reopen” starting with golf courses, tennis courts, basketball courts, pools, marinas, parks, etc. But no beach yet. It’ll be very interesting to see if case rates change course in a few weeks. One of the flyers stated that county park bathrooms will remain closed for now. I guess it’s a great time to discourage hand washing…

April 29

More green. Energy led the US sectors, up 7.4%. For the 3rd day in a row, the Russell 2,000 was an index leader, up about 5% today. But most major indexes were also up more than 2%, including international. $GLD is up .55% and $BTC is up over 13% so far today. Pretty crazy previous 5 days:

If this is a bear market rally instead of an actual bull run, then it’s the first of its kind in history (re: duration & bounce) as Ryan Detrick highlighted today.

This market is confusing as hell right now. Need to stay disciplined.

US GDP (a broad measure of goods and services produced in the economy) dropped in Q1 -4.8%. Which included a strong Jan/Feb so the decline basically came from part of March which means Q2 should look significantly worse. This is the first drop since 2014 and the worst quarterly drop since 2008.

I listened to Eric Peters on the Hidden Forces podcast today. I first referenced him on this page back on April 7. I really enjoy listening to his calm, collected, insightful thoughts on not only the markets but society. Some paraphrased excerpts:

- ‘…We’re overly confident in our ability to prevent an outcome like that and as a result we get blindsided by a complex mass hysteria that it appears we’re entering into. It appears we’re entering into our first, let’s call it mania that is a pessimistic one. We’re accustomed to these bullish ones like dot-com but we haven’t in our lifetime seen a bearish mania. But it appears to me that we’re tipping into that right now… it’s super important for us to realize how dangerous of a place we are right now. We are 100% in a global depression that’s worse than the Great Depression. The only question is how quickly we emerge from it. And I think there’s a level of confidence that has almost tipped into arrogance that through some aggressive policies out of the central bank and the treasury that we can just bridge this gap and get to the other side and largely be fine. I think a number of financial asset classes are priced for that scenario. That may be what happens and wouldn’t that be wonderful if it does? But I think the real risks are tilted in the other direction and certainly the risk in terms of market pricing is tilted very extremely in the other direction given that asset prices are quite high right now.’

- ‘I think this pandemic and the aftermath of it is going to be devastating for globalization. This has clearly been a catalyst that is going to sever any goodwill between the US and China at this point and economies will have to adjust to that in a very serious way.’

- ‘It seems Americans have gotten conditioned after 9/11 to expect the government to solve problems more and more. And the government has proven itself increasingly inept at solving those problems. And I just worry that in this crisis as everyone is looking towards the government to do something that we’re going to get more of the same… much, much more of it. More government, more authoritarianism, more surveillance, and less solution…”

CNBC published this article about an antiviral drug called Remdesivir that has proven to improve the recovery time for patients as well as mortality rate. Dr. Fauci announced that it will be the “standard of care” for coronavirus treatment.

We crossed 60,000 deaths in the US, 226,000 worldwide.

April 30

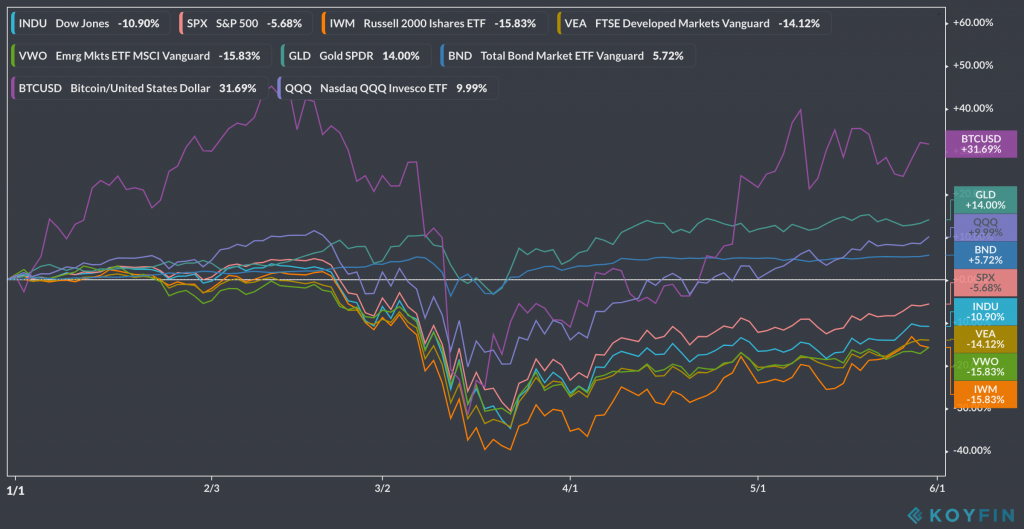

Thursday. Last day of the month. Russell 2,000 cooling off after the run it had this week, down 3.8% today. S&P 500 down 1%, Dow down 1.4%. Here’s a month-end snapshot:

The bounce was huge for some of the big names, plus a few others I care about.

So $SPX is down just ~14% as April ends from the February high, compared to being down over 33% at the March low. It’s such a confusing time because things don’t seem OK. They’re not OK. The economy isn’t OK. And I know, “the stock market isn’t the economy, blah blah blah” but performance still seems irrational and nonsensical. Q1 earnings calls have shown how much the pandemic impacted businesses for just the last two weeks of the quarter, and everyone knows Q2 is going to be awful. Q3 and Q4 are unknown. So why the rally? Was March the low? Was March a panic and the April rebound largely a rebalancing exercise from America 1.0 losers into America 2.0 winners? Or just a flight to quality? How much should the US and international valuations matter? These questions help to express the uncertainty in financial markets right now. Shit is as uncertain as it gets.

Jobless claims rose another 3.84M. The total for the last 6 weeks is 30.3M. For context, the entire GFC of 08-09 saw just over 37M.

It seems like I’m referencing material from Eric Peters (CEO/CIO of One River Asset Management) daily here. I read his latest ‘wknd notes’ titled Mass Hysteria. As always, he’s concise, eloquent, and thought provoking. I highly recommend following him to get his updates on LinkedIn. In this week’s edition, he ends his opening with, “Will the real world rebound to meet the paper asset prices artificially set by the Fed and Treasury? Or has the relationship between paper assets and reality been permanently severed? And if that is so, then what will be the price we pay?” He later expands on manias and mass hysteria (optimistic & negative) that he spoke about on the Hidden Forces podcast episode that I wrote about yesterday.

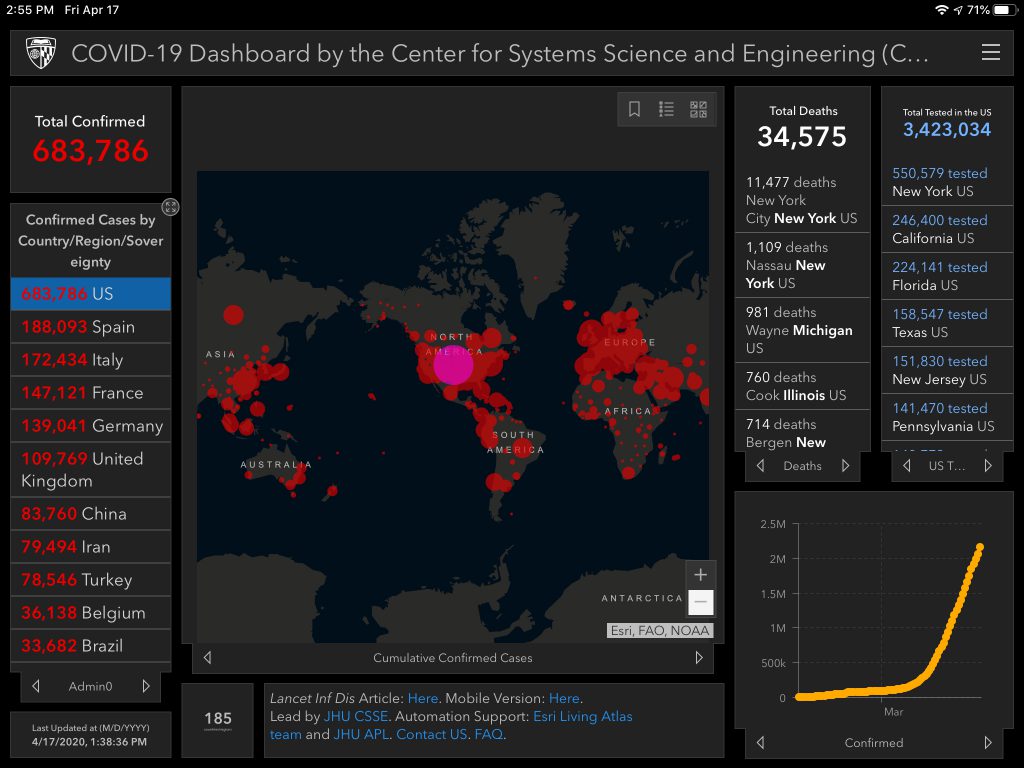

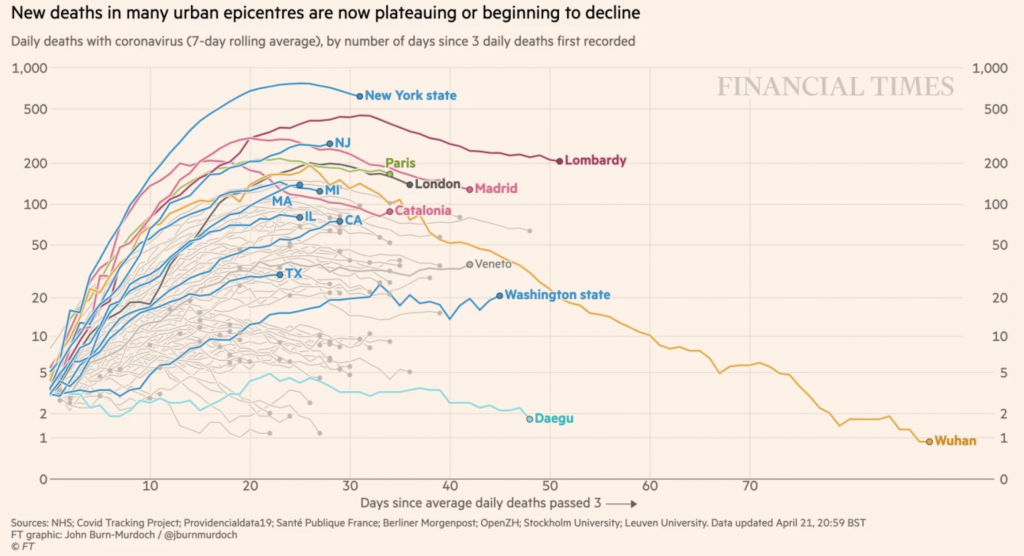

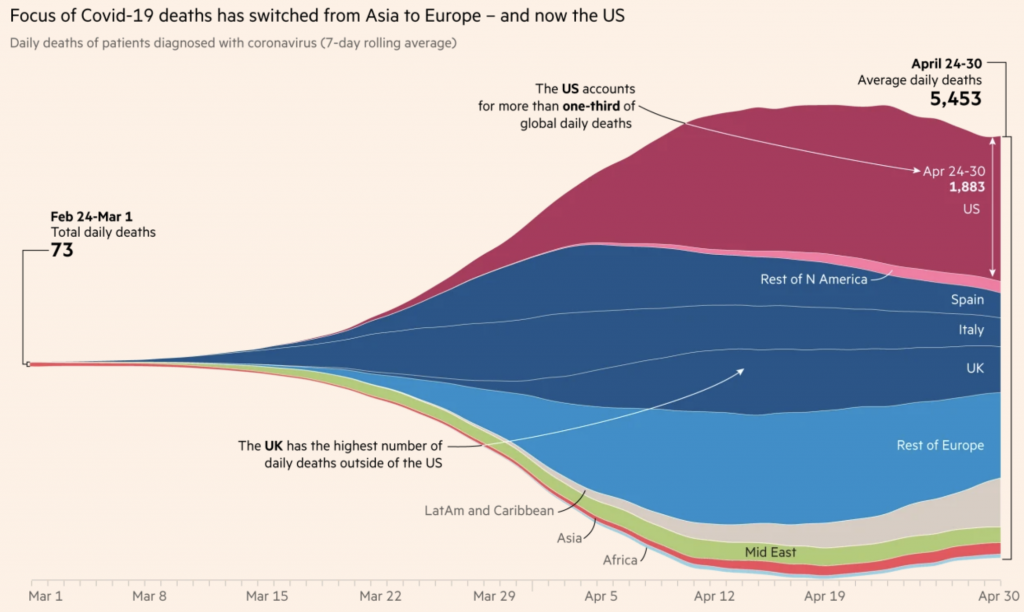

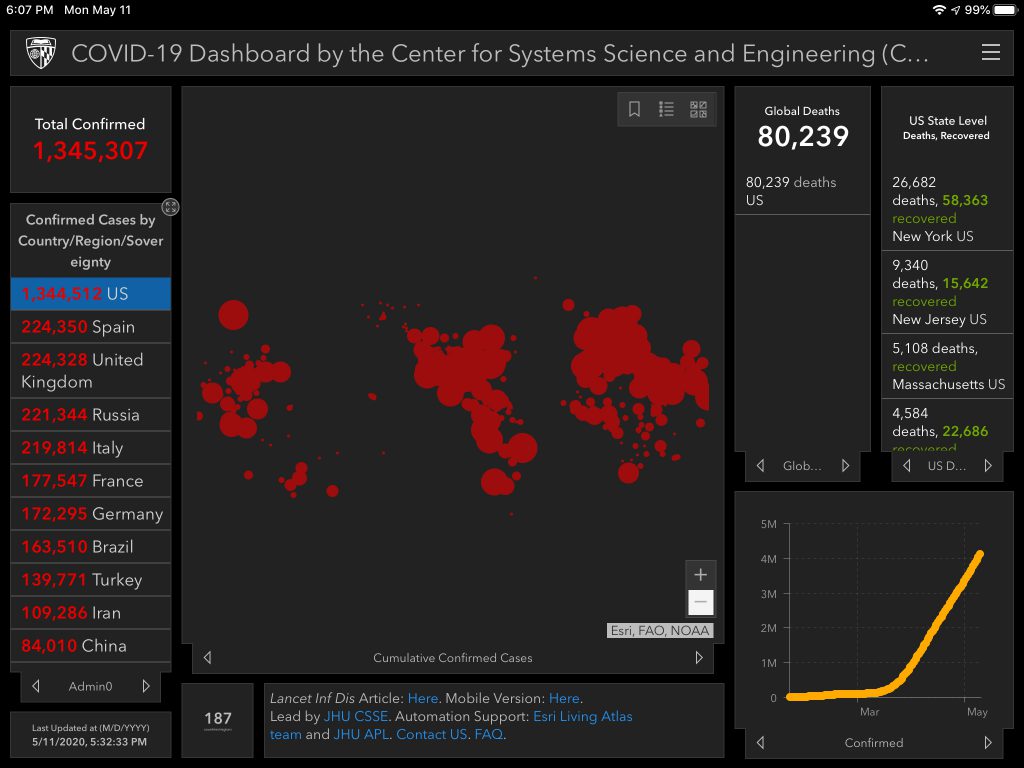

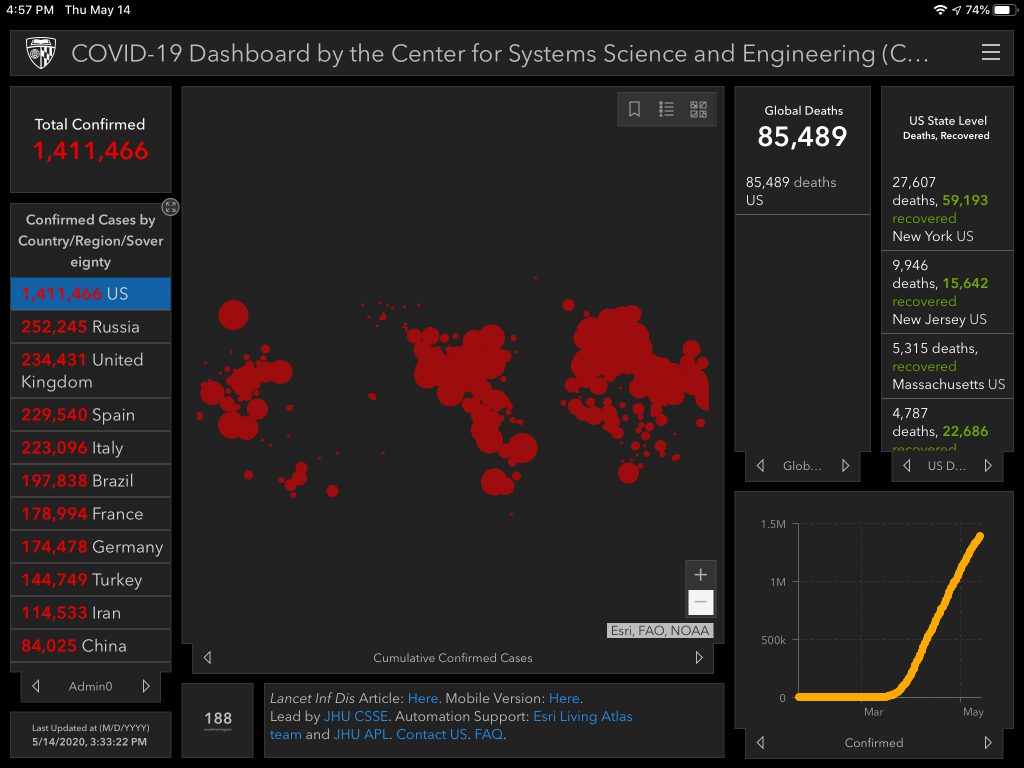

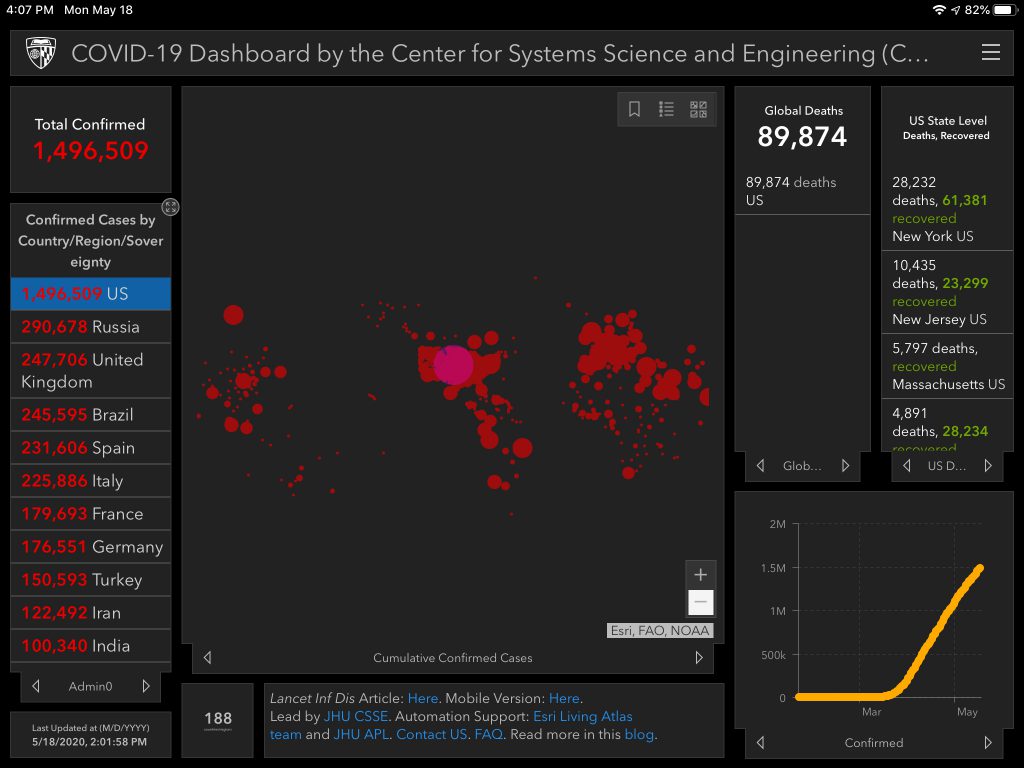

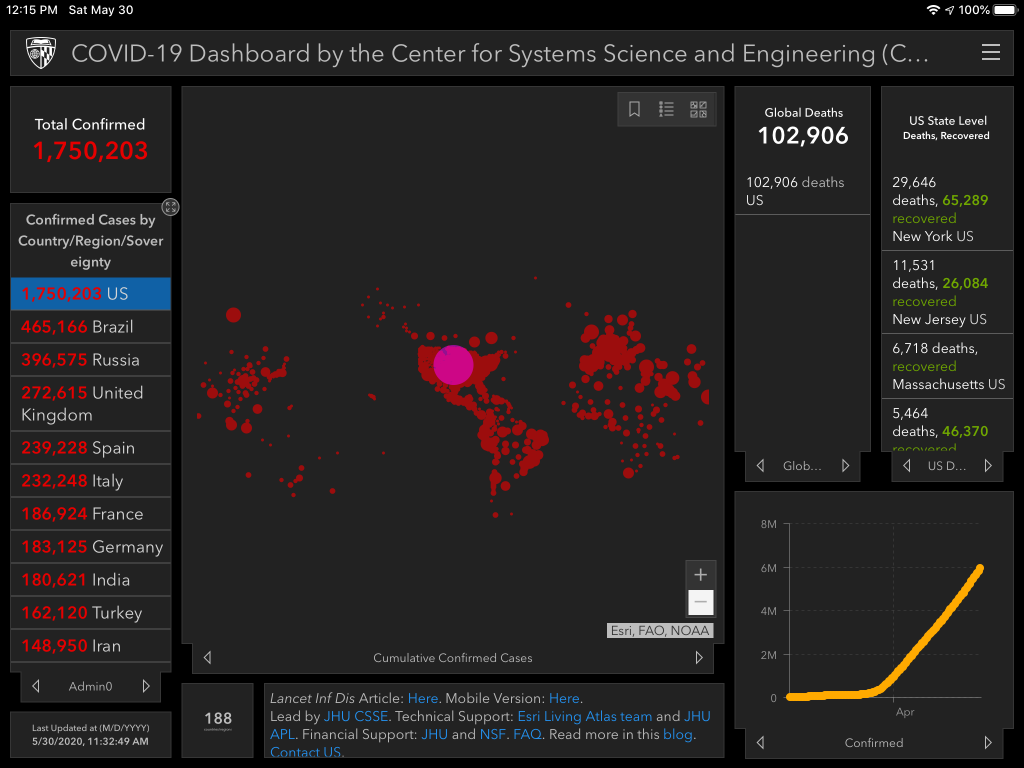

The graphic below from FT.com shows the average daily death count across major regions. I scrolled up on this page to see the first US Dashboard image that I posted. It was on March 19. Just 6 weeks ago. And the total COVID-19 US death count was just 200. Now the daily average is over 27x that. It’s mind-boggling how many lives have been lost or changed dramatically over that short time period.

May

May 1

Friday. Markets finished the first trading day of the month as a rational person would expect, unlike most of April. Russel 2,000 down 3.8%, S&P 500 and Dow both down 2.8%. $GLD up .6%.

Wells Fargo joined Chase by announcing they’ll no longer offer home equity lines of credit (HELOCs). They’re clearly bracing for rough times to come in the form of foreclosure increases, in which they’re 2nd in line behind the primary mortgage lender to be repaid.

Yahoo Finance published The month stocks broke from reality. It’s a great title and Myles Udland recapped April succinctly. “And while whether the stock market is a good representation of the broader economy is an eternal debate in the business world, April’s judgment was clear: stocks did not reflect April’s lived experience.”

I read Connor Haley’s (Alta Fox Capital) Q12020 letter. He’s a small/micro-cap investor who I came across online about a year ago. I tend to enjoy his writing and think he does great research within his niche of “buying high-quality and under-followed businesses at low prices.” The letter shows his prudent risk management technique and why discipline is so important. He reminds us, long term investors, “When you ‘zoom out’ and put the risk in its proper context, you realize that for many high-quality businesses, this slowdown will be largely irrelevant three to five years from now.” But that doesn’t mean secular shifts should be ignored. For example, he touches on their past investments in traditional casinos and increased bullishness on online operators, a thesis they believed in before the pandemic, but that has accelerated. Some industries and consumer behavior will change forever. Take that seriously if investing in individual companies.

The NFL announced plans to play the full season starting in September. “The schedule will come out as normal, but we’re doing reasonable and responsible planning as we always do, inside of game operations… Empty stadiums, neutral sites and no bye weeks are among several alternatives being discussed.”

I published my April 2020 Health Review. Gotta stay healthy!

My wife and I were thinking about ‘the new normal’ on the horizon… the ‘reopening’ period… the current pre-COVID-19 vaccine period vs. its wide availability. As a pediatric health provider, she encounters parents all the time who oppose vaccination (which blows my mind). Will these parents feel the same towards the COVID-19 vaccine as they feel towards others on the immunization schedule (flu, measles, hep a/b, etc.)? Will schools or businesses require vaccination to return? If they can require it for this virus, can or will they require it for others? Maybe a silver lining from this horrific time period will be stricter vaccination enforcement.

May 3

Sunday. The 2020 annual Berkshire Hathaway shareholders meeting was yesterday, with the only attendance option being virtually through Yahoo Finance. Only Warren Buffett and Greg Abel were present to talk and take questions (socially distanced by what looked like ~10sh feet). We were assured that Charlie Munger is healthy but not participating, despite his proficiency with Zoom.

Warren said a lot. Literally. He talked from about 4:45 pm ET until about 9 pm. 89 years old. I don’t think he took a bathroom break, even though he was sipping down his Cherry Coke. You can read the full 2020 Annual Berkshire shareholder meeting transcript here, or the plethora of articles that have already been published like Warren Buffett still cites See’s Candies as an acquisition he loves, 48 years after buying it. I don’t care to recap the meeting or try to interpret how Warren and Berkshire feel about the future short term market prospects. I’ve read plenty from others who are taking it upon themselves to speak for WB by saying they interpreted his tone, stories, and Q1 + April action as ultra bearish in the short term. We know how he feels about equities long term, so that’s not in question (“never bet against America”). Maybe he’s bearish… perhaps terrified but couldn’t say it because he knows he has the power to move the markets Monday morning. But maybe he’s not. I have no reason to believe these interpretations or to try to guess myself. I prefer to focus on the facts, the things he didn’t say he didn’t know about. When he says, “I don’t know,” I believe him. I know it probably means he has an idea, but an idea isn’t the same as knowing. Who can? It’s uncharted territory. So, below are the things he was more certain of that I’ll be thinking about this week.

- They completely sold out of their airline positions. WB said, “But I think that there are certain industries, and unfortunately I think the airline industry among others, that are hurt by a forced and shut down by events that are far beyond their control.” If he thought travel would resume again in the next 1-2 years, than he would have likely held them. But he doesn’t. He doesn’t know for sure but thinks pretty strongly that the industry may be changed forever.

- They haven’t done any deals. The prices haven’t been right. They want to but only for the right price. “We’re not doing anything big, obviously. We’re willing to do something very big. I mean, you could come to me on Monday morning with something that involved 30 or 40 billion or $50 billion, and if we liked what we were seeing, we would do it, and that will happen someday.” This is a clear signal that valuations are still very high.

- He explained what happened around March 23rd, the current crisis low. “But right around in the day or two leading up to March 23rd, we came very close but fortunately we had a Federal Reserve that knew what to do, but money was… investment-grade companies were essentially going to be frozen out of the market. CFOs all over the country had been taught to sort of maximize returns on equity capital, so they financed themselves to some extent through commercial paper because that was very cheap and it was backed up by bank lines and all of that. And they let the debt creep up quite a bit in many companies. And then of course, they had the hell scared out of them by what was happening in markets, particularly the equity markets. And so they rushed to draw down lines of credit. And that surprised the people who had extended those lines of credit; they got very nervous. And the capacity of Wall Street to absorb a rush to liquidity that was taking place in mid-March was strained to the limit to the point where the Federal Reserve, observing these markets, decided they had to move in a very big way. We got to the point where the U.S. Treasury market, the deepest of all markets, got somewhat disorganized. And when that happens, believe me, every bank and CFO in the country knows is, and they react with fear. And fear is the most contagious disease you can imagine; it makes the virus look like a piker. And we came very close to having a total freeze of credit to the largest companies in the world who were depending on it. And to the great credit of Jay Powell… but Jay Powell, in my view, in the Fed board belong up there on that pedestal with him [Paul Volcker] because they acted in the middle of March, probably somewhat instructed by what they’d seen in 2008 and ’09. They reacted in a huge way and essentially allowed what’s happened since that time to play out the way it has. And then March, when the market had essentially frozen, closed a little after mid-month, ended up, because the Fed took these actions on March 23rd, it ended up being the largest month for corporate debt issuance I believe in history. And then April followed through with even a larger month. And you saw all kinds of companies grabbing everything, coming to market and spreads actually narrow then. And every one of those people that issued bonds in late March and April, I sent a thank you letter to the Fed because it would not have happened if they hadn’t operated with really unprecedented speed and determination… And like I say, we don’t know what the consequences of that [swelling Fed balance sheet], and nobody does exactly. And we don’t know what the consequences of what they undoubtedly will have to do. But we do know the consequences of doing nothing. And that would’ve been the tendency of the Fed in many years past, not doing nothing, but doing something inadequate. But more brought the whatever it takes to Europe and the Fed, then with March, sort of did whatever it takes, squared, and we owe them a huge thank you. But we’re prepared at Berkshire. We always prepare on the, on the basis that maybe the Fed will not have a chairman that acts like that. And we really want to be prepared for anything. So that explains some of the $124 billion in cash and bills.” On one hand, there’s a lot here to digest. On the other, maybe not so much. The Fed acted swiftly. It would have been awful if they didn’t. Time will tell what the consequences may be in the future and if they outweigh those which would have taken place with inaction. I think the main I (and others) are thinking so much about this is because we were taught to manage risk responsibly in the case of a catastrophic event without a Fed or other party stepping in. First world problems. As Warren said, we don’t yet know the long term consequences. Likely some degree of moral hazard as others like Howard Marks have been writing. But I like acting like Berkshire to a degree: “We’ll never get ourselves in a position where we have a lot of money that can come due tomorrow. And people that were financing heavily with commercial paper and then found their business stopped. Well you’ve seen what’s happened to the airlines. I mean they need money. Cruise lines need money. There’s some businesses that, it’s just the nature of what they’re in. Berkshire will never get it in a position where it needs money. And we factor in, like I said, we factor in some things that are not ridiculously unlikely. And I’m not going to spell out scenarios because I, to some extent, you start spelling out scenarios, you may increase the chance of them happening. So it’s not something that we really want to talk about a lot, but our position will be to be to stay a Fort Knox.”

Walking through nearby gated communities has become a favorite quarantine weekend activity for wifey and I. We moved to the area not too long ago so it’s a fun, safe way for us to enjoy a change of scenery. On this morning’s walk, she asked, “What do we have to do to get one of these?” Funny enough, the first thing that came to my mind was, “To get one of these, we need not to buy another in the short term.” I say this because we’ve been trying to act like Berkshire by being conservative and saving cash for years. And we’ve saved for a down payment. But who knows what will happen in the markets. While I don’t know for sure, I think pretty strongly that there’s a lot more pain to come, which is our opportunity.

I want us to A. be disciplined and conservative by maintaining a cushion for the unexpected (health or financial) and B. invest in the highest return assets at reasonable prices. And as of today, buying a home won’t accomplish either of those, so the final answer to her was, “we do more of the same. We keep working hard, saving, and capitalize on investment opportunities when they come.” We also touched on some other topics like rates and the potential departure of residents from NYC. Where will they go? Could they come here in large enough quantities that it lifts S. FL real estate prices? Anyway, as usual, we’re ultimately just thankful that we’re still healthy and employed. That’s what matters most during pandemics and economic crises.

May 4

Monday. Major indexes appeared to trade down for most the day but turned green just before close. S&P 500 and Russel 2,000 finished up about .42%. Energy was the leading US sector, up 3.5%.

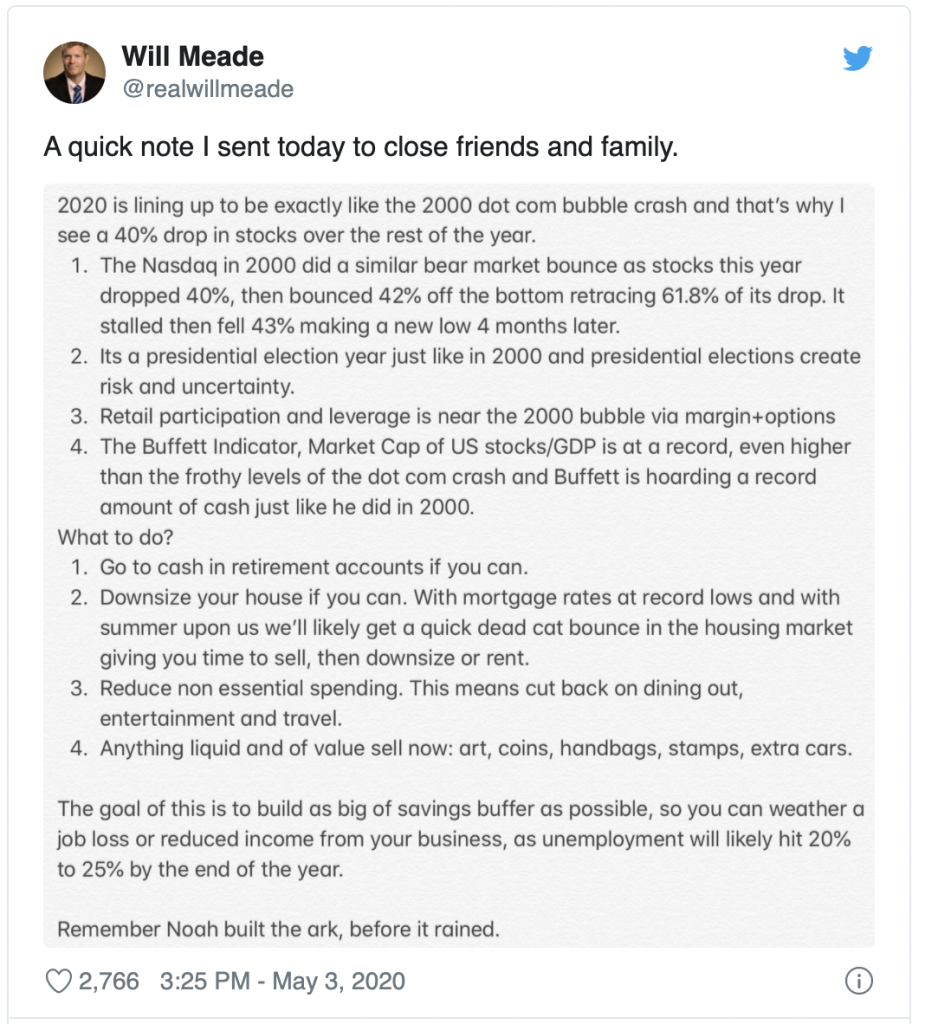

Will Meade shared the note below. Some will view this as fear mongering. Others will view is as a near life saving, money saving fire alarm. But we’ll truly only know what his message (and others like it) are in hindsight. To be clear, I’m not endorsing every piece of content I share on this page; I’m just capturing the current sentiment.

The Washington Post published The iconic brands that could disappear because of coronavirus because “A number of the nation’s most iconic brands are at risk of disappearing, as weeks-long lockdowns and deep economic unrest disrupts consumer spending. More than 100,000 stores could disappear by the end of 2025, according to UBS.” J. Crew already bankruptcy protection. Others like Gap, Nordstrom, Koh’s, Macy’s, J.C. Penney and Neiman Marcus are all in less than desirable positions too. “Now analysts say the coronavirus pandemic that has killed more than 55,000 Americans could change the face of the retail industry, which employs 29 million and supports 1 in 4 U.S. jobs, according to the National Retail Federation. It could be years, analysts say, before consumers feel comfortable walking into a shopping mall again.”

One the rare positives from the pandemic (although it’ll be short lived) includes decreased air pollution. WSJ published, Coronavirus Offers a Clear View of What Causes Air Pollution. “The result has been drops in air pollutants to levels not seen in at least 70 years, easier breathing for people with respiratory ailments and consistently clear views of landmarks often obscured by smog, such as the Hollywood sign in Los Angeles and the Manhattan skyline.”

Business Insider published, The Trump administration is privately predicting the daily coronavirus death toll will almost double over the next month, with new infections increasing from 25,000 per day to 200,000. Scary headline. “That estimate was a large increase from the numbers the president mentioned just a few weeks ago, but doesn’t predict nearly as many deaths as Lessler did in his draft models. On April 20, Trump told reporters that about 60,000 people would die. As of Monday, the US death toll stood at over 68,000 people with 1.16 million infected. There is widespread belief among experts that both the infection total and the death toll are much higher than the confirmed numbers show.”

May 5

Just another ‘new-normal’ day where major indexes were green and I ask myself, “why the hell is the stock market climbing higher?” Most major indexes were up between .4% and 1.1%. Health Care was the leading US sector, up 2.1%.

The latest wknd notes from Eric Peters is out: Descending into the Fog. It’s a stunner.

Here’s another stunner, this time from The Atlantic. The Small-Business Die-Off Is Here, claiming “…it will change the landscape of American commerce, auguring slower growth and less innovation in the future…. The great small-business die-off will fuel industry consolidation, which will both depress wages for workers and increase prices for consumers. More inequality, more sclerosis, and a smaller GDP: These are some of the legacies the coronavirus pandemic is leaving.”

CNN published White House coronavirus task force to be wound down around Memorial Day. I’m not really sure what it means exactly. Surely there will continue to be a group, like the task force, responsible for monitoring, planning, and providing key input to authorities… right? I know I appreciate[d] the daily briefings, especially when they focused on COVID-19 and featured Dr. Birx and Dr. Fauci. I felt somewhat informed and comforted by seeing them on a daily basis.

It’s nurses week so my wife published Love your Job: Why I went into Nursing. I don’t think I have respect and appreciation for anyone more than the selfless, persevering, and underpaid nurses who work tirelessly to take care of others. They’re true heroes during this pandemic (well, outside of pandemics too). They’re a different breed of human being than the rest of us.

May 6

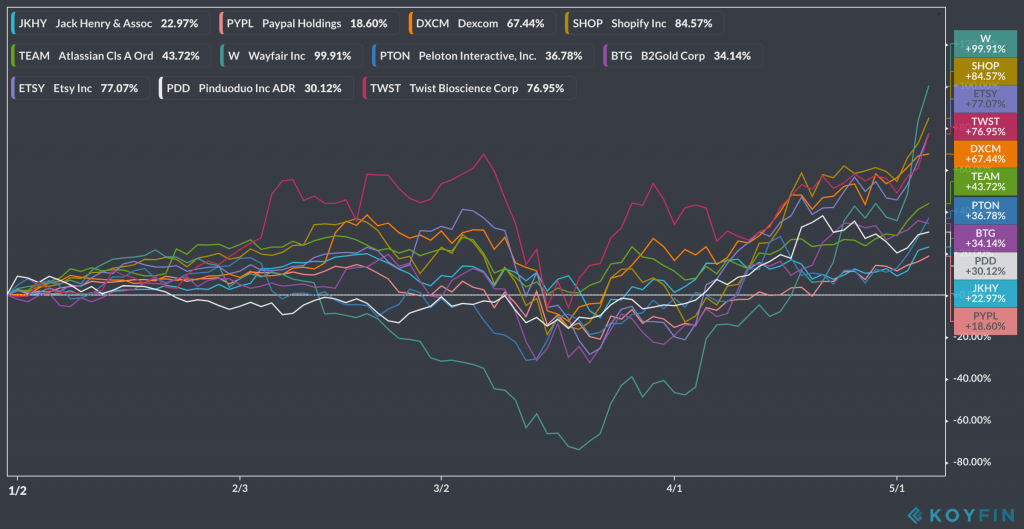

Wednesday. Relatively tame day for the major indexes which were all +- 1% but I got a bunch of alerts for new ATHs of companies I follow (not that I necessarily own). Here’s the ytd performance of some some of them ($dxcm, $pypl, $pton, $shop…):

Layoffs from the well-funded tech darlings continue this week including 1,900 from Airbnb and 3,700 from Uber. Fortunately for those impacted, the packages are extremely generous touting several months base pay, sometimes up to a year in health coverage, etc.. United Airlines announced that they’ll require many US employees to take 20 unpaid days off between May and September, as well as expectations to lay off 30% of administrative jobs.

I came across COVID-19 Consumer Impact Tracker from Glimpse. It might be the simplest visual representation of quarantine life that I’ve come across.

May 7

Thursday. Major indexes tend to rise on jobless claim Thursdays for some reason, no matter how bad. Most closed up 1-1.5% with Energy leading the sectors, up 2.6%. $GLD is up 1.6% on the day and $BTC has been making a run at $10k, reaching $9,970 so far meaning it’s up ~6% in the last 24 hours.

Jobless claims rose another 3.169M. The total for the last 7 weeks is ~33M. For context, the entire GFC of 08-09 saw just over 37M.

I got a few more ATH alerts for stocks on my watch list again today. Peloton was one of them, encouraging me to write about my experience trying to catch the bottom of $pton.

NYT published Small Businesses Counting on Loan Forgiveness Could Be Stuck With Debt. Paul Merski, a lobbyist for the Independent Community Bankers of America said, “Now that over $500 billion of these loans have been approved, we’re really focused on the forgiveness phase, and the forgiveness phase could be 10 times more complex than the initial program.”

May 8

Friday. The rally continued with all major indexes up over 1% today. Russell 2,000 up 3.9%, Dow up 1.8%, S&P 500 up 1.6% and once again, Energy was the leading sector up 4.6%.

Here are a few ytd charts:

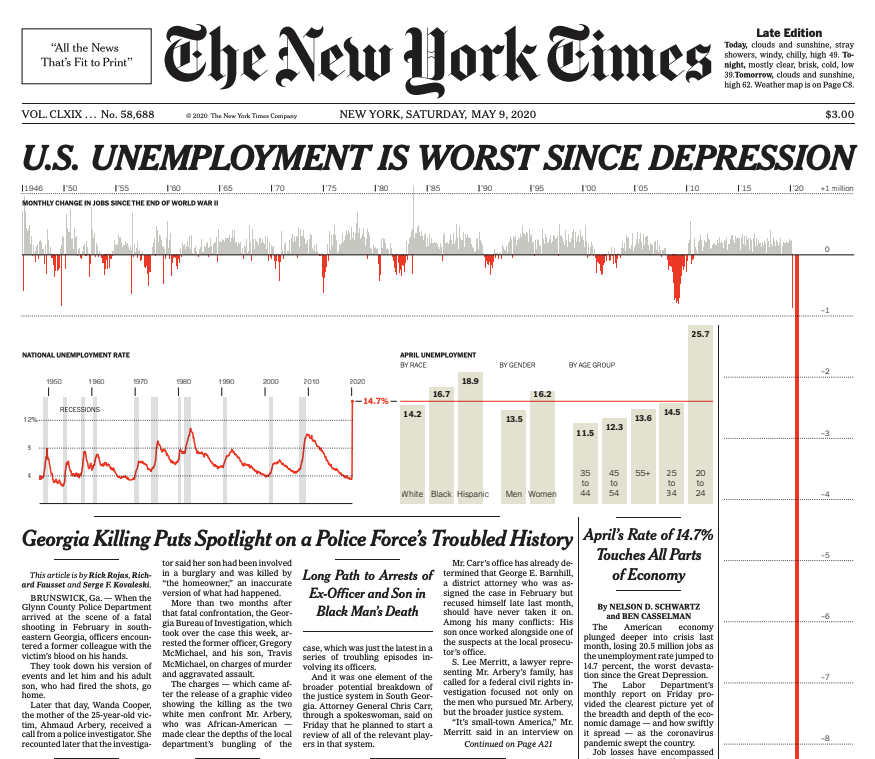

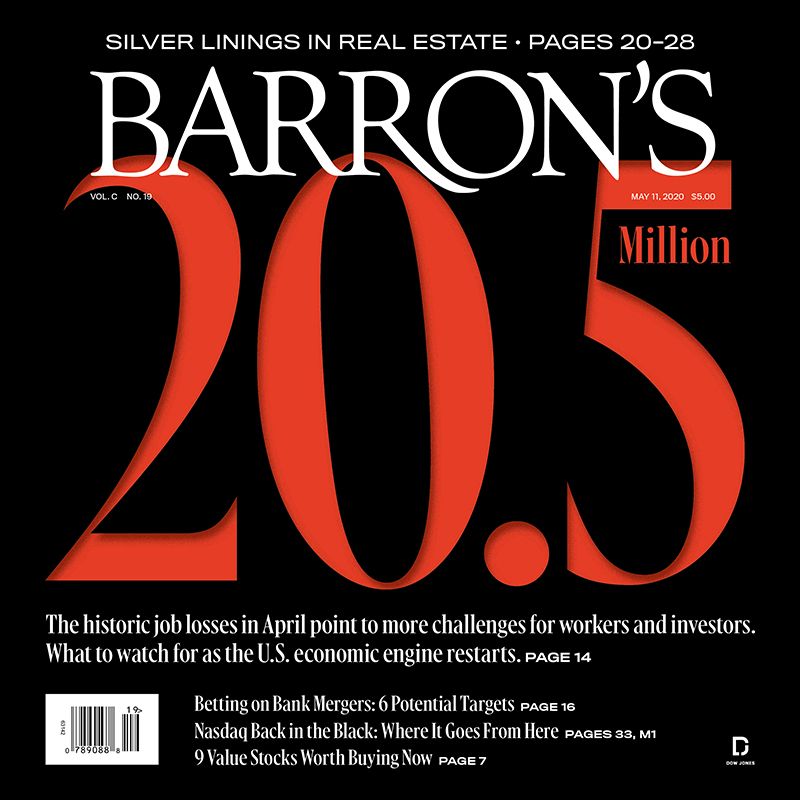

The April Employment Report from the Department of Labor shows an unprecedented loss of 20.5M jobs, catapulting the unemployment rate to 14.7%.

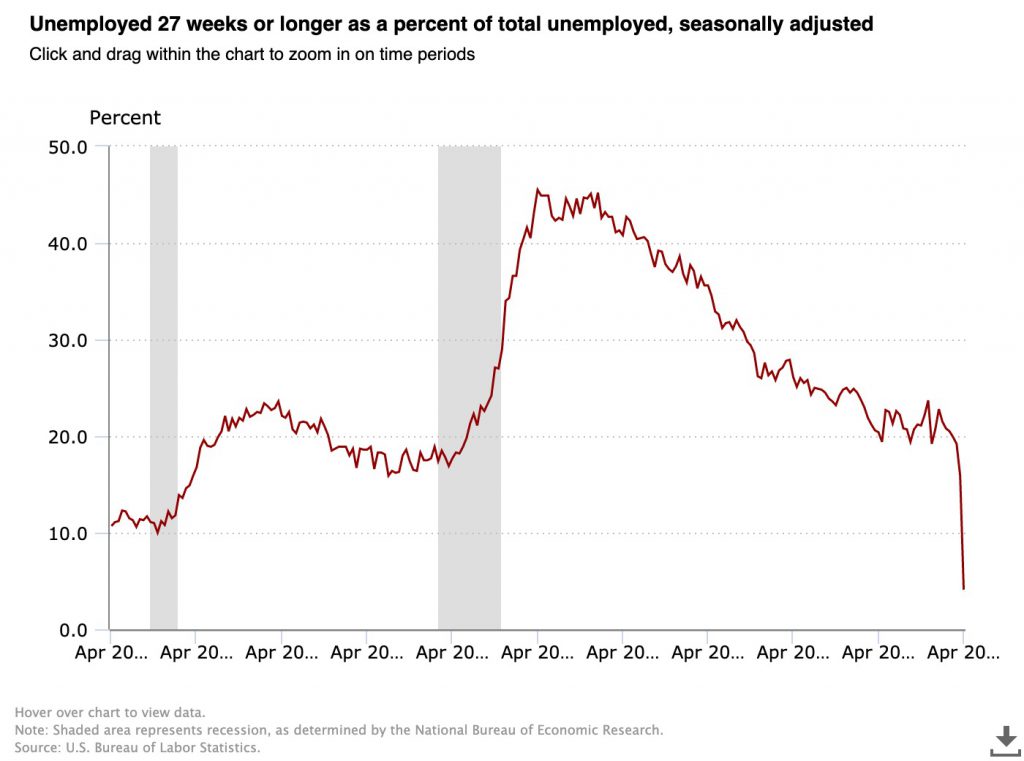

bls.gov makes their charts and data available to visitors. Below is their chart of Unemployed 27 weeks or longer as a percent of total unemployed:

According to Lakshman Achuthan, the three D’s are a method for measuring a recession’s severity.

- Depth – “this recession is extraordinarily deep.”

- Diffusion – “this recession is certainly severe, affecting a wide range of industries.”

- Duration – “this recession could be among the shortest on record.”

We know about #1 and #2, so #3 is the wildcard. This thing just started. IF it somehow ends up being short in duration, then it’s possible we’re already in a new bull market. I personally just can’t fathom that being the case though.

Today would have been the late, great Jack Bogles birthday. Pay tribute by doing yourself a favor by reading his last book, Stay the Course. WB once said, “Jack did more for American investors as a whole than any individual I’ve known.”

I updated my about me page with a bunch of reading and listening recommendations.

The reopening has begun across the country. In most of Florida (where I live), restaurants and retailers are allowed to reopen at 25% capacity. Unfortunately for restaurant workers, my wife and I won’t be dining out anytime soon. We’re just not attracted to dining with masks on while judging and worrying about everyone around us. We’ll probably start getting take-out more often going forward, though. The FL Governor also announced that barber shops, hair and nail salons can operate if precautions are followed, such as wearing masks and gloves. Starting May 18, residents of my county will be allowed to go to our beaches.

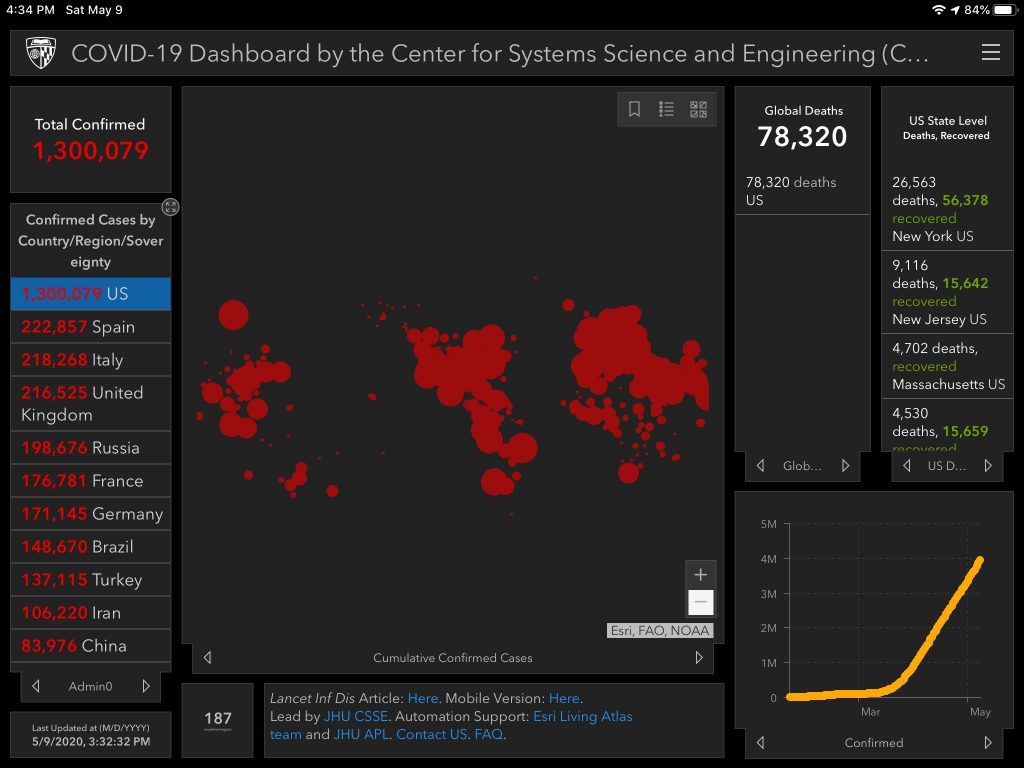

May 9

Saturday. Figured it’s worth capturing some imagery for the future.

Vanity Fair published If 80% of Americans Wore Masks, COVID-19 Infections Would Plummet, New Study Says. It’s extremely frustrating seeing people out in public (picking up food, gas station, USPS, food shopping, etc.) without one.

According to the NYT, “One-third of all people who have died from the coronavirus in the U.S. are nursing home residents or workers. In at least 13 states, deaths in nursing homes account for more than half of all Covid-19 deaths.” Business Insider published this article the NYT article the without a paywall.

May 10

Sunday.

I got around to reading Is (Systematic) Value Investing Dead? From Cliff Asness, which was published following a longer white paper being published by AQR with the same title. He wrote this in summary: “Value is super cheap today, and this is not coming from only the potentially “broken” price-to-book measure (it isn’t even very dependent on it), nor is it due to a group of winner-take-all monopolistic companies. It is not coming exclusively from the tech industries, it is not coming from mega-caps, and it is not coming from the most expensive stocks. Instead it is a pervasive phenomenon. Investors are simply paying way more than usual for the stocks they love versus the ones they hate (and measured using our most realistic implementation this is the clear maximum they’ve ever paid) and doing it in a highly diversified way up and down the cross-section of stocks… We think the medium-term odds are now, rather dramatically, on the side of value, with no “this time is different” explanation we can find…”

Tesla released their ‘Return to Work Playbook‘, something every company is now working on.

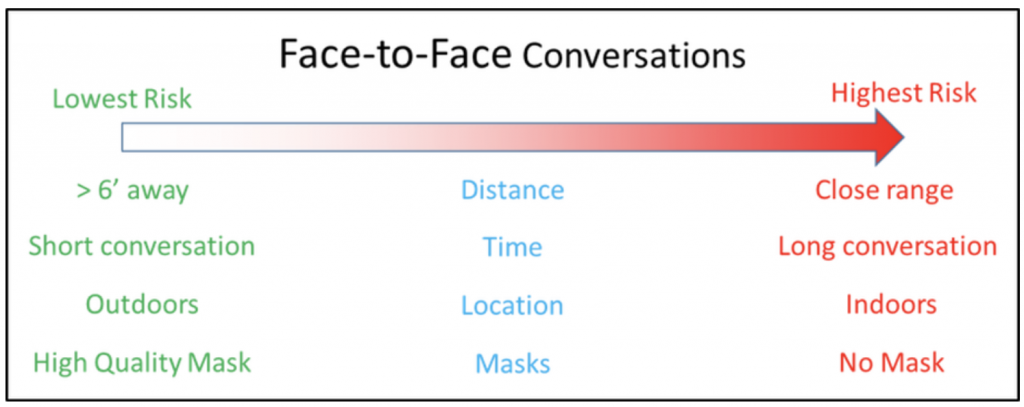

I came across erinbromage.com, the blog of an Associate Professor of Biology at the University of Massachusetts Dartmouth with a Ph.D. in Microbiology and Immunology. His posts are concise and informational. His most recent post titled The Risks – Know Them – Avoid Them starts with, “It seems many people are breathing some relief, and I’m not sure why.” He then does an excellent job articulating that reopening will “add fuel to the viral fire” but acknowledges that reopening is happening whether he likes it or not. Here are some excerpts from his guide to help people understand the risks. Nothing too new, but timely given that it seems like people are taking the act of reopening also to mean that the virus is no longer as threatening or dangerous as it was a month ago.

- “All you have to do is enter that room within a few minutes of the cough/sneeze and take a few breaths and you have potentially received enough virus to establish an infection… This is also why it is critical for people who are symptomatic to stay home. Your sneezes and your coughs expel so much virus that you can infect a whole room of people.”

- “We know that at least 44% of all infections–and the majority of community-acquired transmissions–occur from people without any symptoms (asymptomatic or pre-symptomatic people). You can be shedding the virus into the environment for up to 5 days before symptoms begin.”

- “Any environment that is enclosed, with poor air circulation and high density of people, spells trouble… The main sources for infection are home, workplace, public transport, social gatherings, and restaurants. This accounts for 90% of all transmission events.”

His parting note: “As we are allowed to move around our communities more freely and be in contact with more people in more places more regularly, the risks to ourselves and our family are significant. Even if you are gung-ho for reopening and resuming business as usual, do your part and wear a mask to reduce what you release into the environment.”

May 11

Monday. Up pre-market, down early in the day, then ended relatively flat. S&P 500 closed up .1% while the Dow Jones and Russell 2,000 both closed down .5%. Health Care was the leading sector, up 1.7%, with Financials being the biggest loser, down 1.9%.

I read May 2020 BVI Letter – Macro Outlook, The Great Monetary Inflation by Paul Tudor Jones and Lorenzo Giorganni. Paul is a legendary hedge fund billionaire. Lorenzo, who I hadn’t heard of prior to this, is the Head of Global Research at the Tudor investment firm. More interestingly, he served as the Deputy Director at the International Monetary Fund (IMF) for over 17 years. The letter has been making headlines because in it, Bitcoin is identified an asset with a growing role in the world we’ve found ourselves in and potentially heading towards— a world with inflation due to “a tipping point when a breakdown in global supply chains spills overs to goods prices, undoing two decades of disinflation attributable to globalization” and “high debt accommodated by money printing.”

Page 5 contains a list of assets that can or have worked well during reflationary (stimulating the economy by lowering taxes or increasing money supply) periods:

- Gold – A 2,500 year store of value

- The Yield Curve – Historically a great defense against stagflation or a central bank intent on inflating. For our purposes we use long 2-year notes and short 30-year bonds

- NASDAQ 100 – The events of the last decade have shown that quantitative easing can rapidly leak into equity markets

- Bitcoin – There is a lengthy discussion of this below

- US cyclicals (long)/US defensive (short) – A pure goods’ inflation play historically

- AUDJPY – Long commodity exporter and short commodity importer

- TIPS (Treasury Inflation-Protected Securities) – Indexed to CPI to protect against inflation

- GSCI (Goldman Sachs Commodity Index) – A basket of 24 commodities that reflects underlying global economic growth

- JPM Emerging Market Currency Index – Historically when global growth is high and inflationary pressures are building, emerging market currencies have done quite well